On Friday, December 14th, Credit Suisse announced a 10:1 reverse split of TVIX, effective the 21st. I had pretty much given up on TVIX because its price had slid way past the logical reverse split point and has traded below $1 for the last 16 trading days. However instead of fading to black TVIX is now back into a reasonable trading range.

In February 2012 Credit Suisse got nervous about the rapid growth and size of TVIX, and temporarily pulled the plug on new share creation. Market makers need the share creation process to keep the price of Exchange Traded Products (ETPs) from rising too far above their Net Asset Value (NAV). Typically if the ETP’s price floats too high they short the security with the knowledge that the ETP issuer is usually happy to issue new shares at the NAV price they can buy to cover the short—guaranteeing the market maker a risk-free profit. The selling naturally drives the price of the security down.

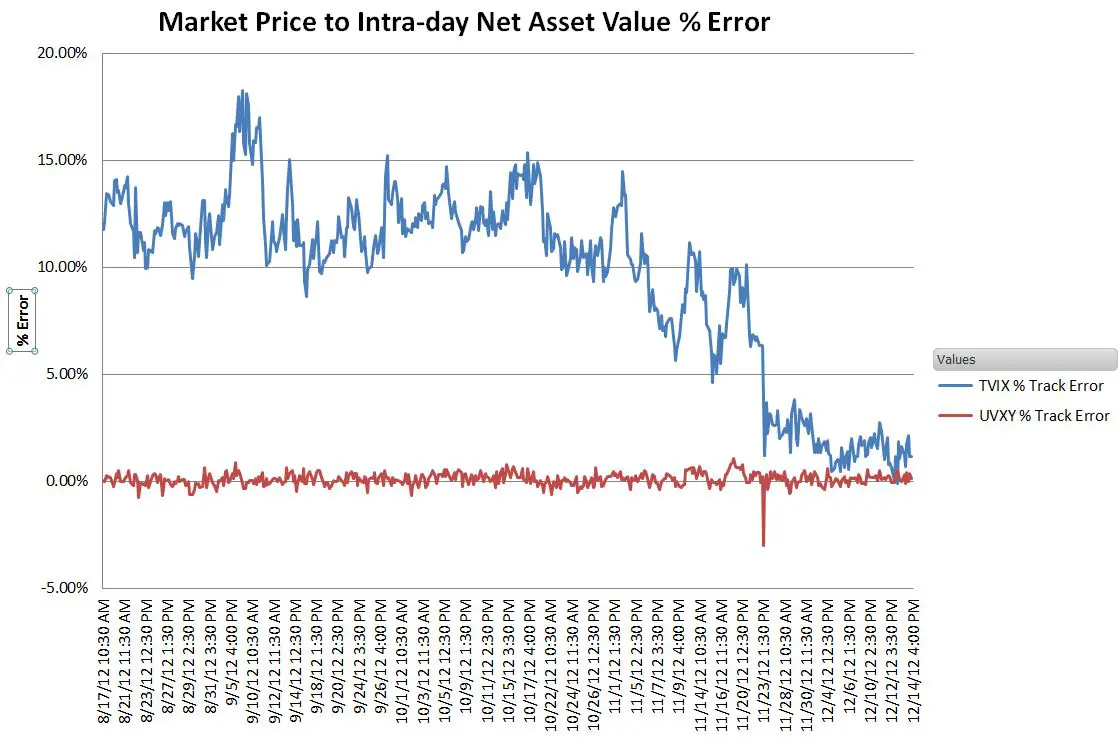

Credit Suisse restarted partial share creations a month later, but in the interim the NAV of TVIX had plummeted 56%—while the market price of TVIX only drifted down 15%. The resultant correction vaporized $277 million of TVIX value in a day. Subsequent tracking still wasn’t great—Credit Suisse’s partial solution was expensive for the market makers and only profitable for them to short the ETP if it was 5% to 15% above the NAV price—better but still a horrible tracking percentage.

Apparently Credit Suisse had been working on the share creation problem. The TVIX prospectus was revised in early November and starting November 23rd, TVIX’s tracking improved considerably. The chart below shows its tracking error alongside of ProShares’ UVXY— its closest competitor.

When TVIX’s tracking error dropped suddenly on November 23rd it appears that it spooked some investors into dumping their UVXY—messing up its tracking for an hour or so until its market makers pulled it back into line.

Unfortunately this improved tracking was a short term thing. A week or two after the split TVIX’s tracking error returned to the 5% to 7% range. While not a killer, I’m hard pressed to see any advantages of TVIX over ProShares’ UVXY, its well behaved ETF based equivalent.

Year to date in 2012 TVIX is down an astonishing 97%, but it was even a worse year than normal for 2X leveraged volatility funds. Next year I project a 90% loss, so TVIX might not require reverse splitting again until around December 2013.

Still, $117m AuM seem to be eager to lose 90%+ per annum.