VXX hasn’t hit a new low in 6 weeks, and it’s not because the market is crashing. What has changed is the shape of the VIX futures term structure—the underlying futures that the various volatility Exchange Traded Products (ETP) like VXX, XIV, TVIX, and ZIV are based on (see volatility tickers for the entire list).

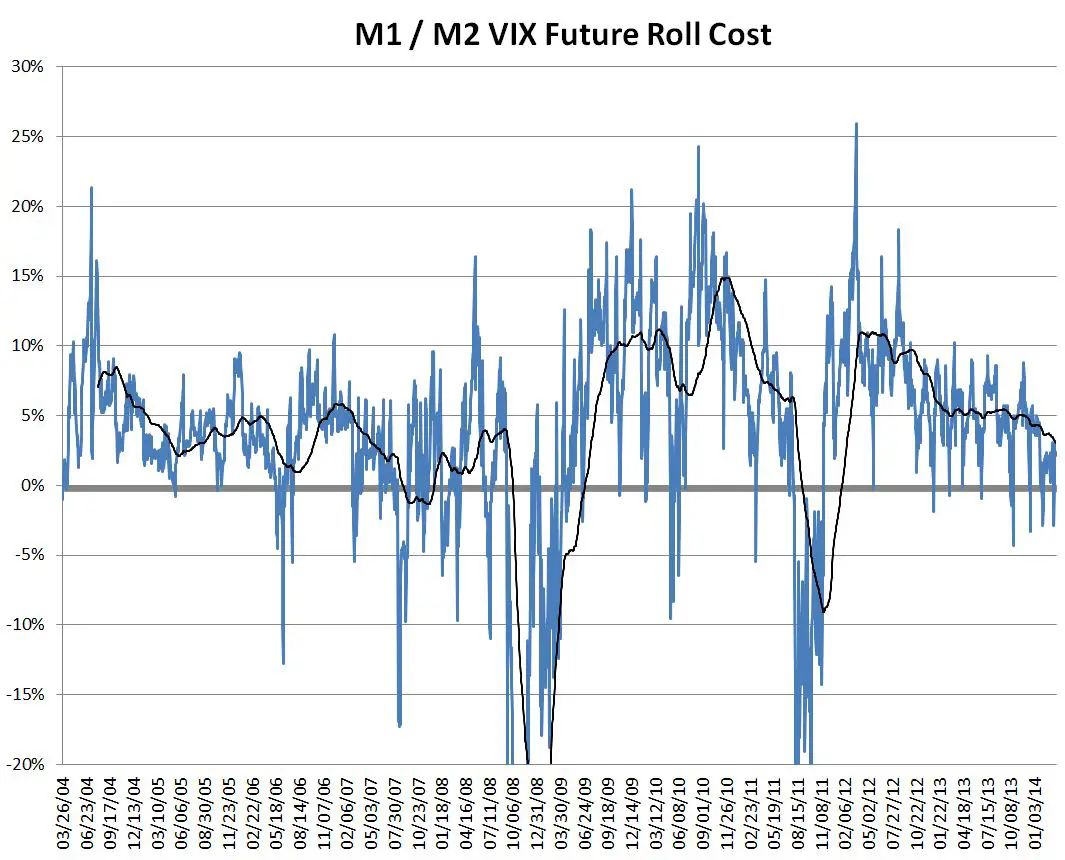

For most of 2009 through 2012 the monthly roll cost between the two front month VIX futures used by VXX averaged around 10% when the market was flat or rising (in contango). In 2013 this average cost dropped to around 5% and is headed even lower in 2014.

|

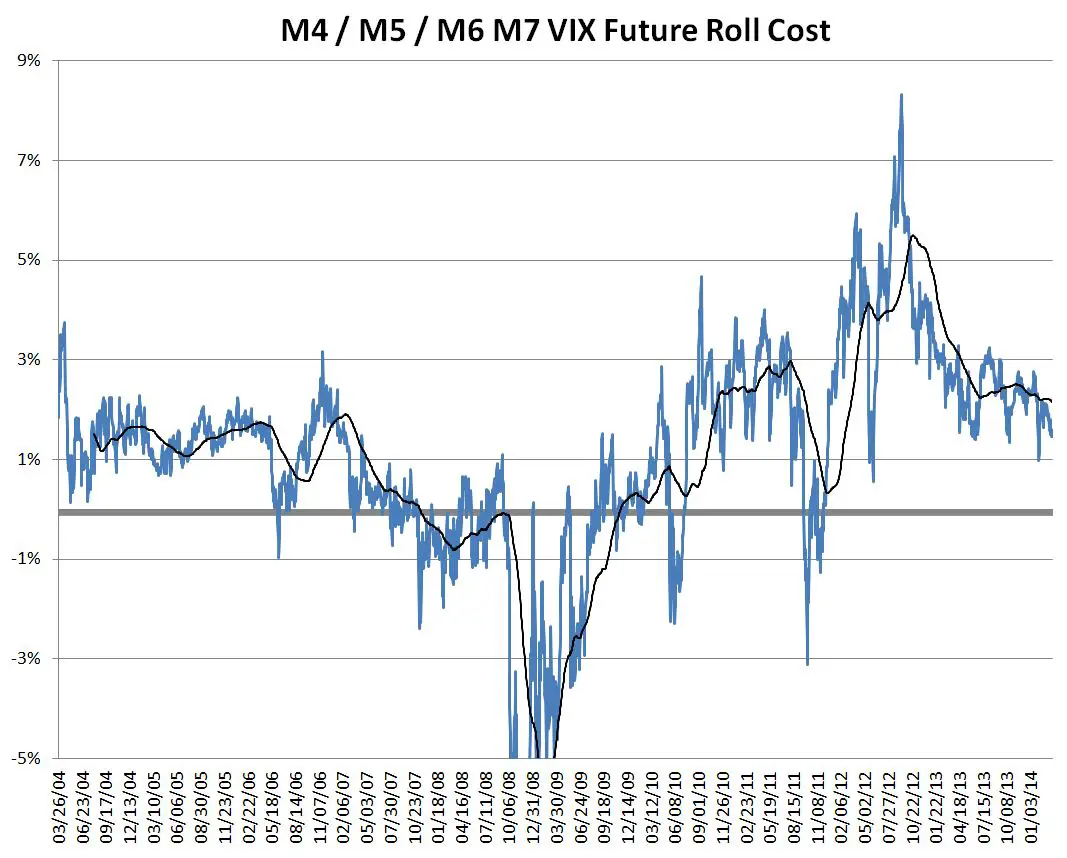

The monthly roll costs of the longer term VIX futures used by VXZ and ZIV have been declining also, dropping from historic 5%+ highs during 2012 to average slightly above 2% in 2013 and 2014.

|

This change was driven by a flattening of the VIX Futures term structure. In spite of the front month’s future being about the same value, the later dated futures values have dropped considerably since early 2013.

|

Why has the curve shifted?

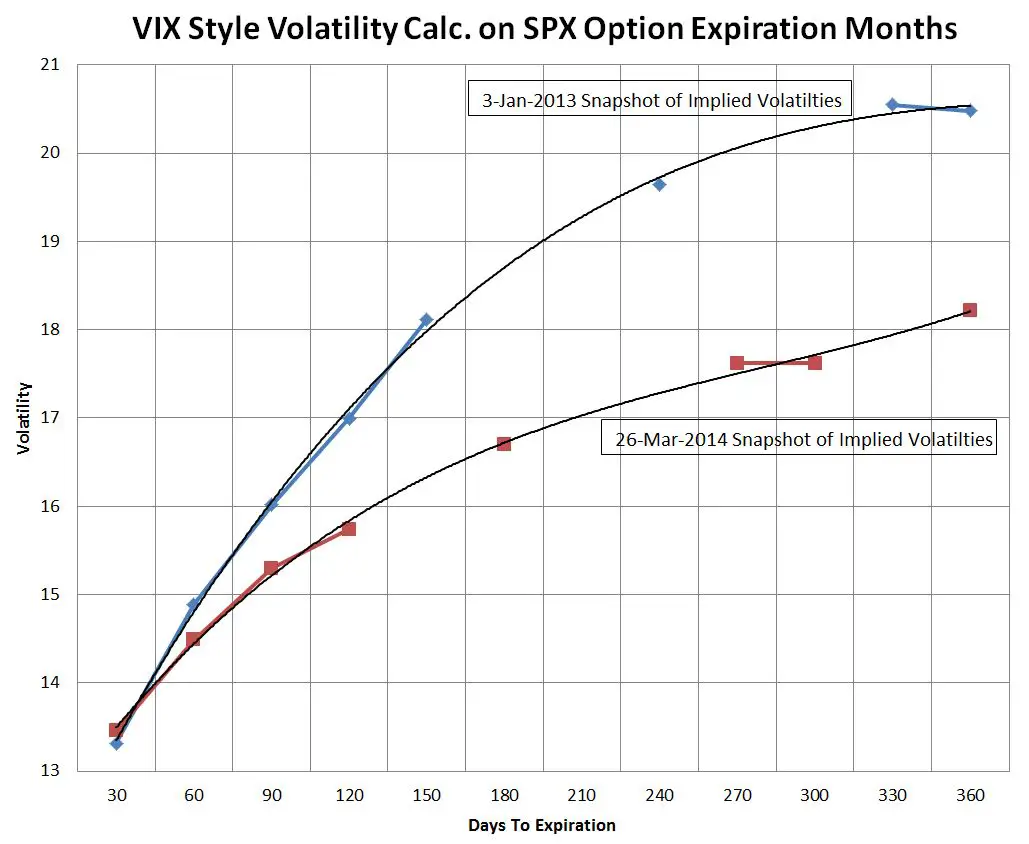

First of all it’s important to remember that VIX futures are ultimately tied to the prices of SPX options of the appropriate month (e.g., August VIX futures are settled to September SPX options). So the real driver is the much larger SPX options market. Not surprising the SPX options premiums have shown the same shift in term structure over this timeframe.

I think this big shift in longer dated volatility is due to two factors:

- A lot of people have taken short volatility positions in the last year and a half

- Traders are less concerned about volatility spikes in general, so they are paying less for longer term “insurance” via SPX options and VIX futures

Both of these factors would tend to depress longer term SPX option prices—and VIX futures prices. It’s possible that this trend will continue, leading to the flattened term structure we saw in 2007 and early 2008 —at the end of the last bull market. But I doubt it; instead I expect the term structure to stabilize until we see another real VIX spike (into the 40’s).

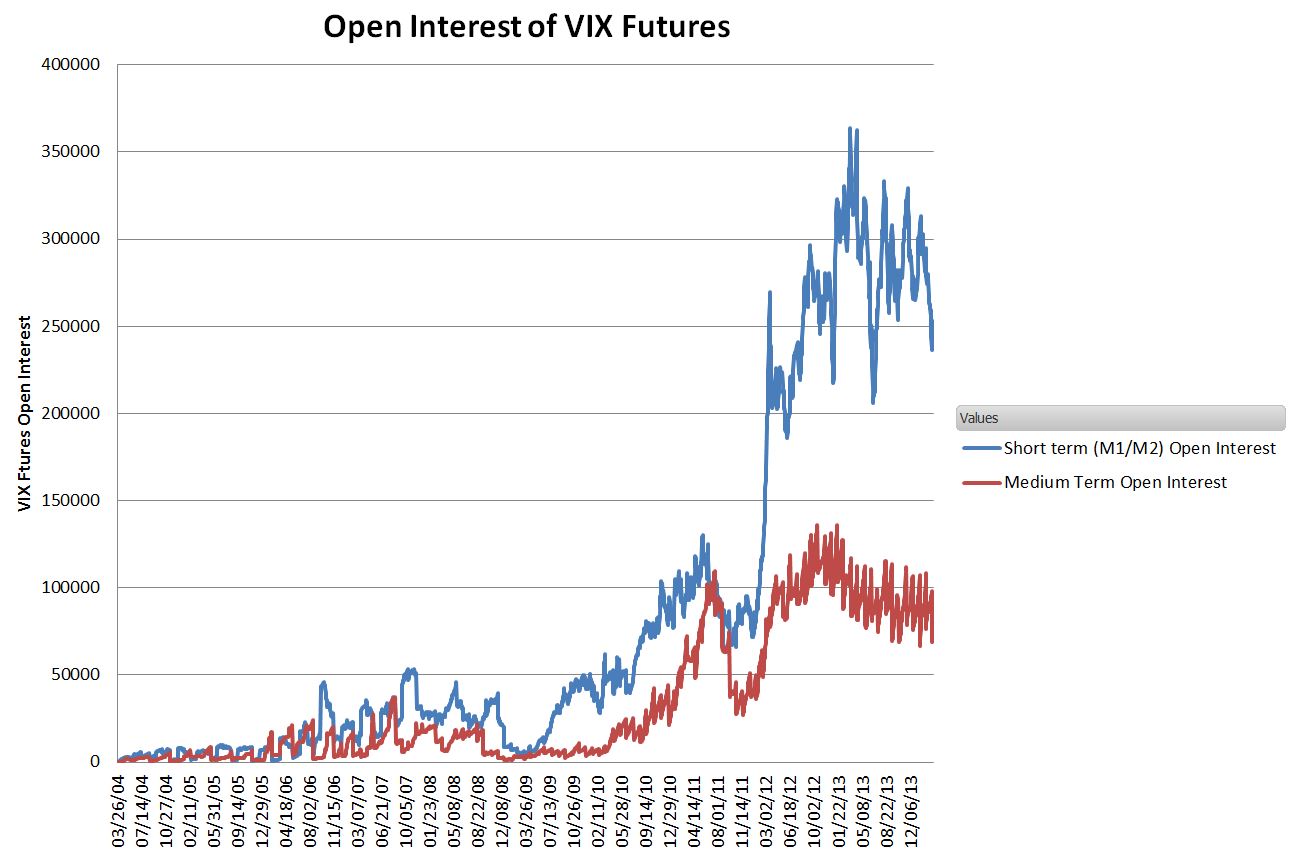

Coincident with the drop in contango, there has been a leveling off of the open interest in VIX futures. I don’t think either of these changes caused the other—but perhaps I’m missing a linkage.

|

Up until 2013 the open interest had been growing 40% per year, but since then the shorter term open interest has stabilized and the medium term open interest has pulled back around 20%. VIX futures volume on the other hand has continued to set records. Volatility ETP asset growth was a big driver in VIX futures starting in 2009, but currently the total assets in those funds have hit a plateau.

VXX will probably set some new lows in the next month or two, but expect it to moderate its losing ways for a while.

Click here to leave a comment