I have had several requests to do an analysis of a pair trade with the position being short VXX and short XIV. The idea behind the trade is to take advantage of the compounding effects caused by XIV’s daily reset feature that cause it to diverge from a true short. For example if VXX goes up 20% one day and then down 16.7% VXX is back to its starting point, but XIV would be down almost 7% after that sequence. The intent of the short VXX position would hedge the overall position against changes in market volatility.

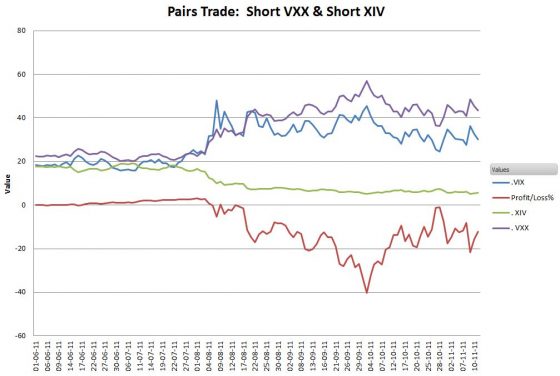

For my analysis I assumed the short positions started with the same dollar amount, shorting 1000 shares of VXX and shorting enough XIV shares to provide the same dollar amount. The results putting the position in place 1-June -2011 are shown below:

The end result is a position that never goes more than a little positive, has a lot of volatility, and as of 11-Nov-2011 would have had a 12% loss.

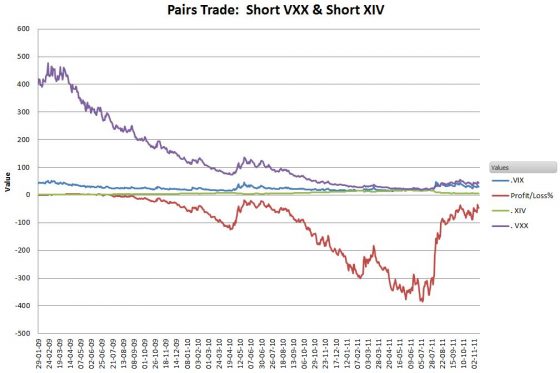

For a long term performance picture I ran the backtest from 29-Jan-2009, when VXX first started trading. I used simulated XIV results for the data before its 30-Nov-2010 introduction.

This one gave a 46% loss. Not all starting dates result in losses. Starting the beginning of 2011 gives a nice 17% gain.

I think the biggest problem with this combination is that the leverage of a short position is variable. When the VXX price is close to the price that the short was initiated the leverage is around one, but if VXX moves significantly higher then the leverage gets higher (see this post), and the vice versa when VXX drops. The XIV short shows the same behavior.

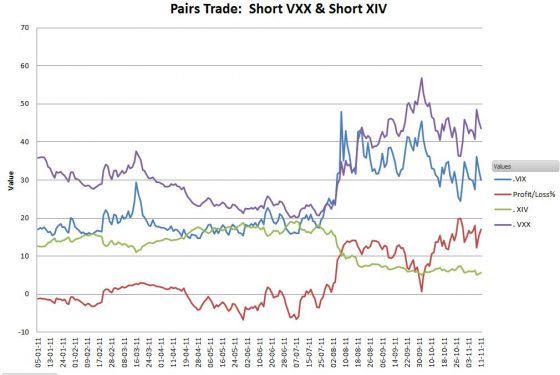

Ideally a pairs trade would remove some of the volatility out of a position, but I think this combination is as tricky as a straight VXX or XIV position. The spreadsheet I’ve used to create these graphs makes it easy to try any start date after 29-Jan-2009, so if you think the key is when you initiate the position you can backtest your hypothesis. See this post for download information.

If you only could choose one, would you rather short VXX or buy XIV?

This is an interesting idea but can’t be an effective strategy return-wise, betting on both sides at the same time.

A related question, the VIXY and VXX both seem to suck at tracking ^VIX returns due to contango as per http://goo.gl/jvDUZ However, XIV seems to do a good job at inverse tracking. The question is: would shorting XIV be a good way then to track ^VIX returns?

Hi Jon, Looking at a Yahoo chart http://finance.yahoo.com/q/ta?t=2y&s=XIV&l=on&z=l&q=l&c=%5Evix%2Cvxx&ql=1 it doesn’t look like shorting XIV would be better than long VXX. Contango hurts both positions.

What sort of time frame are you looking at? For very short timeframes CVOL and UVXY do a decent job of tracking the VIX.

— Vance

Hi Vance, I’m looking at a 1-3 year time frame. As per your chart above, when the ^VIX made 100% gain sometime in Oct 2012, XIV lost 50% of its value. Towards the end of the chart (e.g. Mar 2013), XIV is nearly 100% up, when the VIX has lost 50%.

That looks like pretty good tracking over a 2 year period. Or perhaps I am reading the chart too casually?

Hi Jon, I don’t understand the purpose of such a long term short–you’re almost guaranteed to lose a lot of money. Is your goal to catch the next VIX spike?

— Vance

Hi Patrick, I haven’t run the numbers but I would expect VXX’s contango impact to drag the combination down during the 75% of the time the market is in contango. Rather than static allocations I prefer the XVZ approach that shifts the mix based on market conditions.

— Vance

Vance,

Thanks for this analysis! I sort of suspected that strategy wouldn’t work…

Andrew

Hi Andrew,

Yup… Not many free lunches out there.

— Vance