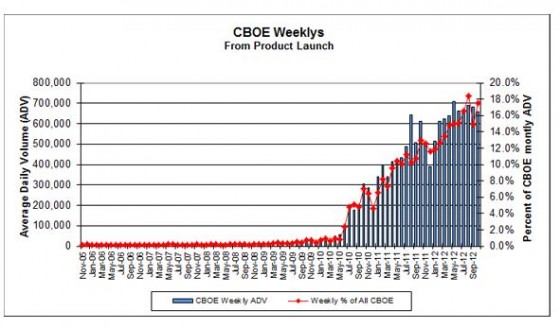

The volume of CBOE’s Weeklyssm options has grown rapidly since they expanded their listings into equities and Exchange Traded Products in June 2010. Now weekly options comprise almost 30% of the CBOE’s average daily option volume. The list of available weekly options is available on the CBOE website.

Among other things, option traders take advantage of the Weeklys to position themselves for earnings releases, harvest rapid premium decay near expiration, and place low-cost directional plays.

Two press releases suggest that the Options Clearing Corporation (OCC) and the CBOE are moving to the next phase—making up to 5 weeks of options available on popular securities and moving existing options to look more like the Weeklys. The specific moves are:

- Five weeks of Weekly options for many securities (press release)

- Initially Weekly options were only made available 9 days before their expiration. If you needed a later expiration date your only choices were monthly options with their 3rd Saturday of the month expiration, or in some cases quarterlies. In 2013 the CBOE started making SPX options available with weekly expirations 5 weeks in advance. Evidently encouraged, they rolled out additional weekly expirations for additional indexes and stocks (e.g., SPY & AAPL). Overall I think the advantages of a more regular set of dates will outweigh the problems with spreading option volume across more option classes.

- Rationalizing ticker symbols with SPX options (press release)

- There are two different tickers for SPX options, SPX, and SPXW. Unlike other options there are weekly options (PM settled) on the same week that the monthly (AM settled) expire. For more on SPX options see this post.

In general the move to weekly options has been gradual and non-invasive. One of the side benefits of the rise of the SPX weeklys is that now there are always options series that closely bracket the 30 day volatility window of the VIX calculation. Using the monthly SPX options there were sometimes longish extrapolations required with suspect accuracy. In October 2014 the CBOE switched the VIX calculation methodology to take advantage of the SPX weeklys availability. Ultimately this new VIX calculation was needed to support VIX Weekly futures and VIX Weekly options.

Click here to leave a comment