Update

A comment on this post from “~”, writer of the Volatility Futures and Options blog, revealed that in this post I made the mistake of assuming that correlation meant causation in analysing the data—a danger I warn against in Patterns, Predictions, and the Correlation Fairy. It’s too bad, it was a fun story. I’m not beating myself up about it, but it illustrates the dangers (and ease) of constructing a story to fit the data. The coincidences in this case seemed compelling, but a little additional research might have found the information that “~” discovered.

Here’s his comment:

“the explanation for the abrupt decline of daily range is much simpler – S&P changed the way it computes high and low. The timing of this change just happen to coincide with the futures listing. “… the index high and index low were compiled by aggregating the highs and lows of individual firm prices for each day. This amounts to assume that the highs and lows for all 500 companies occur at the same time in each day. This is clearly an incorrect assumption and amounts to an overestimate of the highs and an underestimate of the lows. As a result, the ranges are over-estimated.” Source: Ray Y. Chou (2006), Modeling the Asymmetry of Stock Movements Using Price Ranges, in Dek Terrell,Thomas B. Fomby (ed.) Econometric Analysis of Financial and Economic Time Series (Advances in Econometrics, Volume 20 Part 1) Emerald Group Publishing Limited, pp.231 – 257″

Original post July 2013

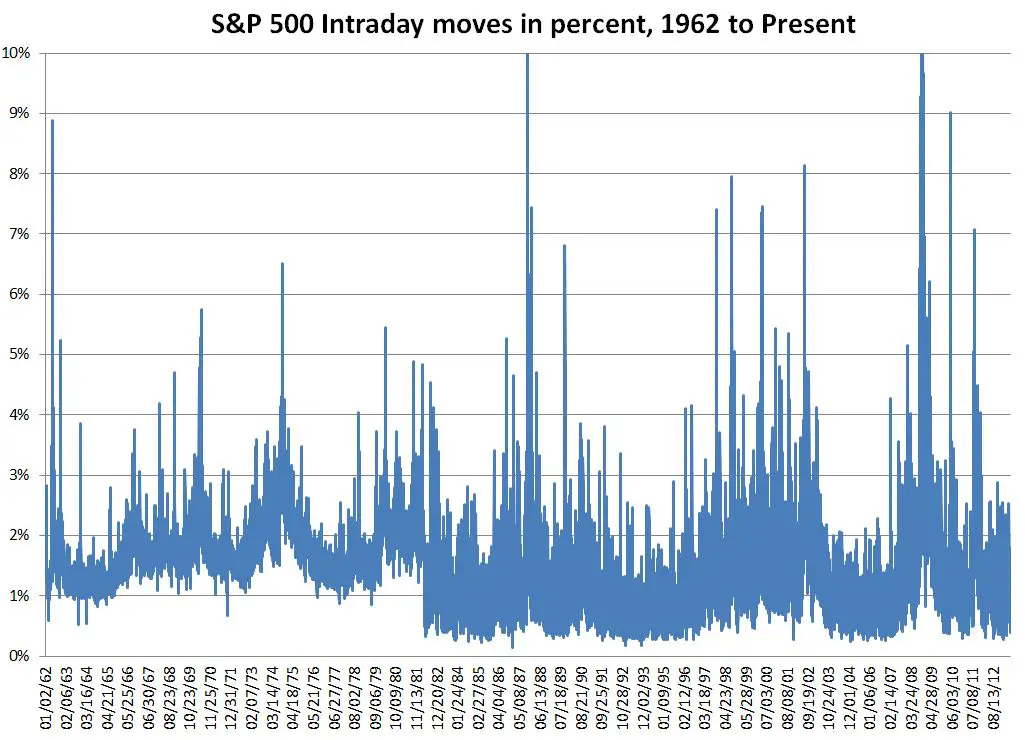

Recently I have been analyzing long term volatility trends using S&P 500 index daily results. One of the things I calculated was the high-low daily range expressed in percentage. The chart looks like this:

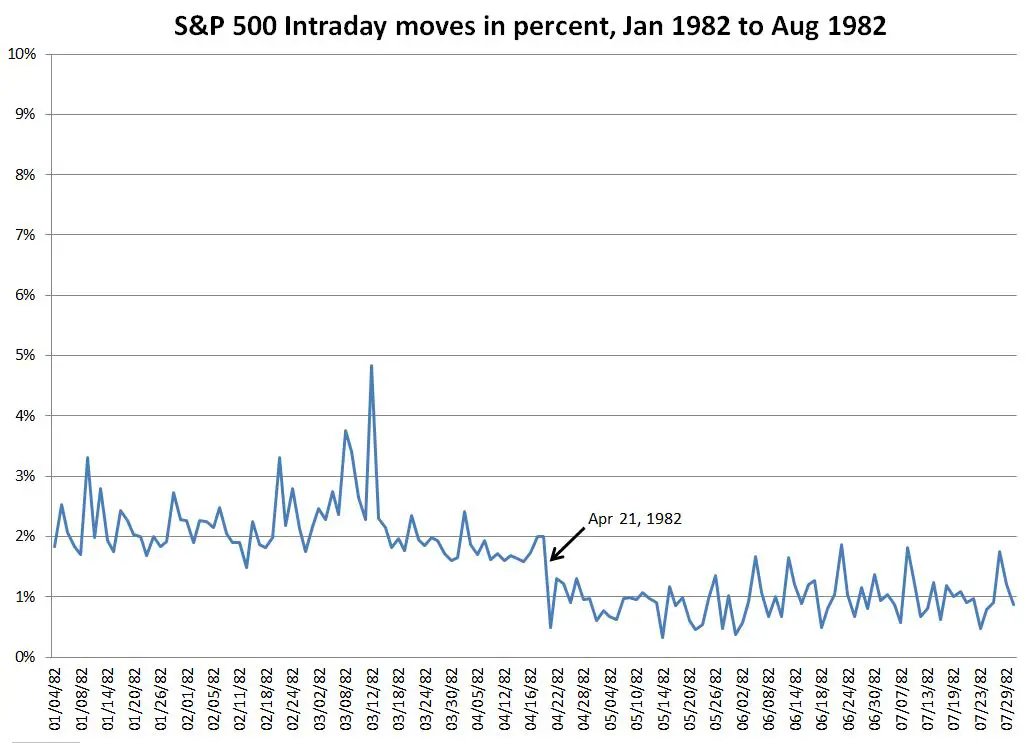

What caught my eye was the drop in the lower bound in 1982. Before 1982 the daily range rarely dropped below 1%, and then it dropped instantaneously to around 0.3%. The upper bound did not seem to be significantly affected. I zoomed in on the first half of 1982.

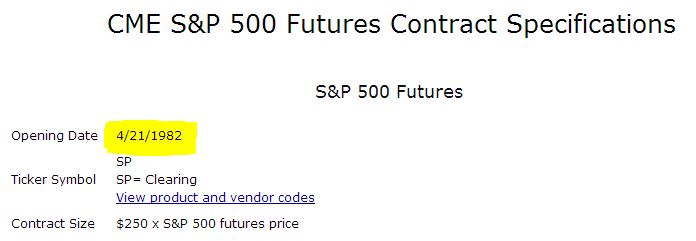

The shift happened on April 21st, 1982. That date didn’t ring any bells for me, so I did a Google search and found this.

This was the day S&P 500 Futures started trading. I don’t think the change in the intraday range was a coincidence.

The S&P 500 index went from being a metric to an investible security, and the behavior of the entire market was impacted. This change was almost certainly driven by arbitrage. With futures it’s straightforward to capture any signficant differences between what a future is trading at and the value of the underlying stocks (see this post for more info). Arbitrage tends to keep the futures price aligned to the index, but since the underlying stocks are being bought/sold en-masse as part of the arbitrage operation—without regard to their individual situation it also increases the correlation between stocks in the index.

Since this beginning in 1982, the rise of the tradable index has changed the face of investing, and is one of the key drivers of the increased volatility of the market.

Hi Vance, the explanation for the abrupt decline of daily range is much simpler – S&P changed the way it computes high and low. The timing of this change just happen to coincide with the futures listing. “… the index high and index low were compiled by aggregating the highs and lows of individual firm prices for each day. This amounts to assume that the highs and lows for all 500 companies occur at the same time in each day. This is clearly an incorrect assumption and amounts to an overestimate of the highs and an underestimate of the lows. As a result, the ranges are over-estimated.” Source: Ray Y. Chou (2006), Modeling the Asymmetry of Stock Movements Using Price Ranges, in Dek Terrell,Thomas B. Fomby (ed.) Econometric Analysis of Financial and Economic Time Series (Advances in Econometrics, Volume 20 Part 1) Emerald Group Publishing Limited, pp.231 – 257

Hi ~, Damn, there goes my clever theory–leaving me with another case of correlation not being causation. I’ll update the post with your solution. Thanks! By the way, glad to see you blogging again. Best Regards, Vance

Increased volatility? Isn’t that an argument for decreased volatility?

My assertion is that Increased correlation in the S&P 500 during fearful times has increased the realized volatility. If the stocks in the S&P 500 were uncorrelated with respect to each other (random moves) the average would have very low volatility.

— Vance

Thanks for the response. I’m not sure that I agree, though. What you seem to be pointing out is that the market moves less during the day. (S&P percent changes from low to high have gone down.) I would think that would decrease volatility. What you leave out is what happens overnight (which would be influenced less by the introduction of futures trading). Just based upon what you have presented (less movement of the index during the day), I’d take it as an argument for lower volatility.

Now, you can’t look at S&P returns overnight using the index open since that open level contains many “stale” prices. Hmm. I’ll have to think about how to measure that back to ’62.

I agree that the chart displayed doesn’t prove my assertion. While the peak intraday volatility does increase and I think that is at least partly due to index trading the minimum and avg volatility do go down. Among other oddities after the futures started trading it became much more likely that the index closed at the high or low for the day. I speculate this might be because there were buy or sell on close orders that drove most/all of the 500 stocks to their bid or ask values for the last print. Back in the days of fractional prices this was a sizeable difference.

This chart https://www.sixfigureinvesting.com/wp-content/uploads/2013/08/SP-HV22.jpg shows that there has been a multi-decade increase in average inter-day volatility, but it doesn’t show any 1962 anomolies that finger the futures. I think my increased correlation argument driven by tradeable indexes on fearful days is pretty strong as the root cause, but it is still in the arm waving category in terms of proof.

–Vance

nice post, thanks for your work