It’s been said that we learn more from failures than success. Hopefully the chart below will be an illustration of that. It displays the near real-time prices of VIX futures vs. the predictions of a “simple” model I’ve created. My intent with the model is not to achieve high accuracy (it won’t) but rather to distinguish between when VIX futures prices are truly unusual, and when they are displaying typical behavior.

The yellow dots show the percentage error between my estimate and the actual quotes.

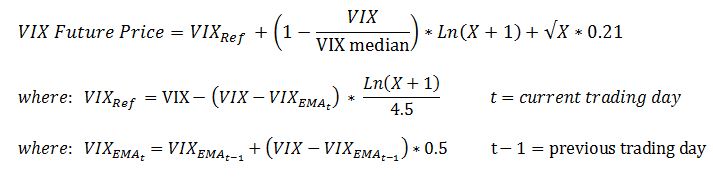

I put simple in quotes above because I recognize that most people would not consider the formulas below simple. But compared to the typical academic treatment of VIX Futures pricing this is a simple model.

The difference between this model and the one I described in the very simple model displayed below is the addition of functionality that addresses VIX jumps and slumps. The VIX itself is quite volatile with daily double-digit percentage changes being relatively common. Typically VIX futures lag these moves by about half (e.g, if VIX moves +10% the VIX futures term structure might shift up 5%).

I modeled this behavior with an exponential moving average of the VIX, using a coefficient of 0.5. This enhancement works well for the longer-dated futures, but shorter-term VIX futures have progressively tighter tracking to the VIX. To address this, I tweaked the jump/slump term, using a natural log function to extinguish the jump/slump lag as the time to expiration approaches zero.

A Very Simple Model

The graphs and descriptions below belong to my very simple model, which does not incorporate the historical patterns of the VIX at all.

The percentage errors are shown in yellow organized by expiration date.

The current VIX futures quotes are from Yahoo Finance (e.g., ^VIXnov). Unfortunately as far as I know they aren’t providing quotes on the new Weekly VIX Futures yet. The chart below shows the model’s predictions for their values.

that I’ve created

You can check over at vixcentral.com if you want to get the current values for both traditional monthly and the new Weeklys VIX futures (click on the “VIX Term All” tab).

My estimates are produced using this equation:

Where VIX is the current VIX index value, VIX Median is the historic VIX Median value (18.01 for March 2004 through September 2015), and X = days until VIX Future expiration.

For more information on this equation see, “A Very Simple Model for Pricing VIX Futures.”

Thanks for the article. I have a few questions: VIX EMA – how many days for calculating EMA? Is X calendar days or trading days? Do you have an article on Change SPX –> Change VIX Futures? Thanks.

Hi Peter, I used trading days. An EMA doesn’t have a fixed number of days, it just has a weighting factor for how much to factor in today’s data vs yesterday’s EMA. The sensitivity of VIX futures moves to VIX moves is not constant, it changes as the futures approach expiration, so a fixed ratio is not possible. This article https://www.sixfigureinvesting.com/2014/08/hedging-market-with-vix-vxx-uvxy-vix-futures/ is probably the best one to look at.

The VIX term structure really reminds me of CDS term structures, I wonder if there’d be anything interesting in using a jump-to-default model on the data.

Sounds interesting. Can you point to any references?

— Vance