Just about anyone who’s looked at a multi-year chart for a long volatility fund like Barclays’ VXX has thought about taking the other side of the trade. ProShares’ SVXY is an Exchange Traded Fund (ETF) that allows you to bet against funds like VXX while avoiding some of the issues associated with a direct short.

This post will discuss SVXY‘s inner workings, including how it trades, how its value is established, what it tracks, and how ProShares makes money with it.

SVXY went through some serious trauma in February 2018. An unprecedented VIX spike and a VIX future liquidity gap in the late afternoon of February 5th, 2018 resulted in a 90% drop in SVXY’s value and the termination of XIV—a similar fund. On February 27th, 2018, Proshares moved to reduce the chances of a similar event in the future by lowering SVXY’s leverage from -1X the daily moves of SPVXSP, the VIX futures index it tracks, down to -0.5X. This change reduces the chances of a similar drawdown, or of the fund terminating but also reduces the upside potential of SVXY. This leverage change became effective February 28th, 2018.

Since 2018, SVXY has been the only leveraged inverse volatility Exchange Traded Fund (ETF) available, but recently the -1X leveraged SVIX ETF was introduced. For more on that newcomer see “How Does SVIX Work?”

How does SVXY trade?

- SVXY trades like a stock. It can be bought, sold, or sold short anytime the market is open, including premarket and after-market time periods. With an average daily volume of 14 million shares, its liquidity is excellent and the bid/ask spreads are a few cents.

- SVXY has options available on it, with five weeks’ worth of Weeklys and strikes in 50 cent increments.

- Unlike Barclays VXX, VelocityShares’ TVIX, and ProShares’ UVXY, SVXY is not on a hell-ride to zero.

- SVXY can be traded in most IRAs / Roth IRAs, although your broker will likely require you to electronically sign a waiver that documents the various risks with this security. Shorting of any security is not allowed in an IRA.

- SVXY is subject to termination risk. Termination can occur (and did with XIV, a very similar fund on February 5th, 2018) if the daily positive move in the VIX futures market approaches or exceeds 200%. ProShares guarantees that SVXY will not go negative so to protect themselves they will cover their short positions and terminate the fund if things get bad enough. For more on this see XIV Termination.

How is SVXY’s value established?

- Unlike stocks, owning SVXY does not give you a share of a corporation. There are no sales, no quarterly reports, no profit/loss, no PE ratio, and no prospect of ever getting dividends. Forget about doing fundamental style analysis on SVXY. While you’re at it forget about technical style analysis too, the price of SVXY is not driven by its supply and demand—it is a small tail on the medium-sized VIX futures dog, which itself is dominated by SPX options (notional value > $100 billion).

- The value of SVXY is set by the market, but it’s closely tied to the daily percentage moves of the inverse of an index (S&P VIX Short-Term Futurestm) that manages a hypothetical portfolio containing VIX futures contracts with two different expirations. Every day the index methodology specifies a new mix of VIX futures in the portfolio. On a daily basis SVXY moves in the opposite direction of the index with a leverage factor of -0.5X, so for example, if the index (ticker SPVXSPID) moves up 0.3%, then SVXY will move down precisely 0.15%. This post has more information on how the index itself works. The index is maintained by S&P Dow Jones Indices.

- As is the case with all Exchange Traded Funds, SVXY’s theoretical share value is just the dollar value of the securities and cash that it currently holds divided by the number of shares outstanding. This theoretical value is published every 15 seconds as the “intraday indicative” (IV) value. Yahoo Finance publishes this quote using the ^SVXY-IV ticker. The end of day value is published as the Net Asset Value (NAV). The NAV is computed at 4:15 ET, not the usual market close time of 4:00 ET, because VIX Futures don’t settle until 4:15. I recommend that anyone that trades SVXY also keep its IV ticker on your watchlist. If the two prices diverge significantly it indicates that the markets are in turmoil and extra care is mandated. If in doubt, trust the IV price.

- If the trading value of SVXY diverges too much from its IV value wholesalers called Authorized Participants (APs) will normally intervene to reduce that difference. If SVXY is trading enough below the index they start buying large blocks of SVXY—which tends to drive the price up, and if it’s trading above they will short SVXY. The APs have an agreement with ProShares that allows them to do these restorative maneuvers at a profit, so they are highly motivated to keep SVXY’s tracking in good shape.

What does SVXY track?

- SVXY makes lemonade out of lemons. The lemon, in this case, is the index S&P VIX Short-Term Futurestm that attempts to track the CBOE’s VIX® index—the market’s de facto volatility indicator. Unfortunately, it’s not possible to directly invest in the VIX, so the next best solution is to invest in VIX futures. This “next best” solution turns out to be truly horrible—with average losses of 5% per month. See this post for charts on how this decay factor has varied over time. For more on the cause of these losses see “The Cost of Contango”.

- This situation sounds like a short sellers dream, but VIX futures occasionally go on a tear, turning the short sellers’ world into something Dante would appreciate.

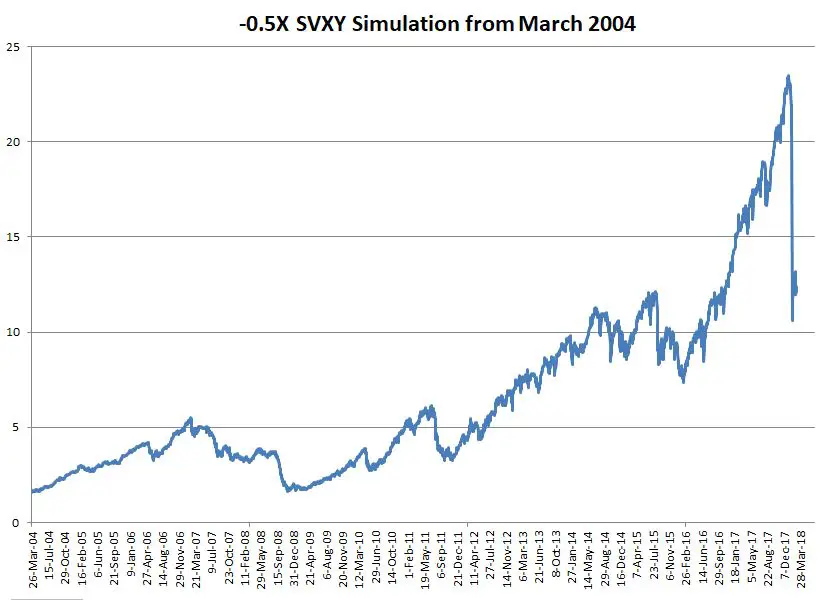

- Most of the time (75% to 80%) the SVXY strategy is a real moneymaker—the rest of the time it is giving up a lot of value quickly. My simulation shows that 65%+ drawdowns would have occurred if the -0.5X SVXY had been trading in the 2004 to 2017 timeframe. The chart below shows -0.5X SVXY from 2004 using historic VIX Futures values to generate simulated values.

- SVXY does not implement a true short of its tracking index. Instead, it attempts to track the -0.5X percentage inverse of the index on a daily basis. To maintain this -0.5X behavior the fund must rebalance/reset its investments at the end of each day. For a detailed example of how this rebalancing works see “How do Leveraged and Inverse ETFs Work?”

- There are some very good reasons for this rebalancing, for example, a true short can only deliver at most a 100% gain and the leverage of a true short is variable (for more on this see “Ten Questions About Short Selling”). The simulated -0.5X SVXY, on the other hand, is up over 600% since VIX futures started trading in March of 2004 and it should faithfully deliver a daily percentage move very close to -0.5X of its index.

- Detractors of the daily reset approach correctly note that SVXY and funds like it can suffer from volatility drag. If the index moves around a lot and then ends up in the same place SVXY will lose value, whereas a true short would not, but as I mentioned earlier, true shorts have other problems. Even with volatility drag daily reset funds don’t always underperform. If the underlying index is trending down, they can deliver better than -0.5X cumulative performance.

How does ProShares make money on SVXY?

- An Exchange Trade Fund like SVXY must explicitly hold the appropriate securities or equivalent swaps matching the index it tracks. ProShares does a very nice job of providing visibility into those positions. The “Daily Holdings” tab of their website shows how many VIX futures contracts are being held. Because of the -0.5X nature of the fund, SVXY will typically be short VIX futures contracts with a notional (list price) value half of the overall asset value of the fund.

- ProShares collects a daily investor fee on SVXY’s assets. The fee is stated as a 0.95% annual fee, but it’s implemented by subtracting 0.95/365 of a percent from each share’s value every calendar day. With current assets of around $400 million, this fee brings in around $3 million per year. That should be enough to be profitable, however, I suspect the ProShares’ business model includes revenue from more than just the investor fee.

- Exchange Traded Funds like SVXY recoup transaction costs in a non-transparent way. Transaction costs are deducted from the fund’s cash balance—resulting in a slow divergence of the fund’s IV value from the theoretical value of the index that it’s tied to. This differs from the approach that Exchange Traded Notes (ETN) use, their theoretical value is directly tied to the moves of the index itself, so the ETN issuers must pay for transaction costs other ways (e.g., out of the annual investor fee, or other explicit fees). In the case of SVXY, this hidden transaction fee has averaged around 0.28% per year.

- One clue on ProShares’ business model might be contained in this sentence from SVXY’s prospectus:

“A portion of each VIX Fund’s assets may be held in cash and/or U.S. Treasury securities, agency securities, or other high credit quality short-term fixed-income or similar securities (such as shares of money market funds and collateralized repurchase agreements).” Agency securities are things like Fannie Mae bonds. The collateralized repurchase agreements category strikes me as a place where ProShares might be getting significantly better than money market rates. With SVXY currently able to invest around $250 million this could be a significant income stream. - I’m sure one aspect of SVXY is a headache for ProShares. Its daily reset construction requires its investments to be rebalanced at the end of each day, and the required investments are proportional to the percentage move of the day and the level of assets held in the fund. SVXY currently holds $400 million in assets, and if SVXY moves down 10% in a day (the record negative daily move is -24%, positive move +18 %) then ProShares must commit an additional $20 million (5% of $400 million) of capital that evening. If SVXY goes down 10% the next day, then another $15 million capital infusion is required.

Important Dates

- SVXY Inception 3-October-2011

- SVXY Leverage Reduction from -1X to -0..5X on 28-February-2018

- SVXY 2:1 Splits 5-October-2012, 24-January-2014, 17-July-17 Reverse split: 1:4 18-September,2018

SVXY won’t be on any worst ETF lists like Barclays’ VXX, but its propensity for dramatic drawdowns (e.g. -48% on 5-Feb-2018!) will keep it out of most people’s portfolios. Not many of us can handle the emotional stress of holding on to a position with huge losses—even though the odds support an eventual rebound.

The eye-popping inverse volatility gains in 2016 and 2017 were followed by a mass destruction drawdown on February 5th, 2018 that hammered the old -1X SVXY and XIV EPTs by -90% or more. This new, lower leverage version of SVXY will be less prone to huge drawdowns/ termination, but bloodletting during volatility spikes will still occur. People will continue to forget how short volatility can be very volatile in its own right.

Vance, can you comment on how SVXY went to 11 which seems like an excessive drop given what VIX and UVXY did. Will there be an “adjustment” from the third-party that rebalances things or am I just clueless? thx!

liquidation. or fear of liquidation

I guess their statement doesn’t mean much then? (“Bethesda, MD (February 6, 2018) – ProShares, a premier provider of ETFs, announced today the performance on Monday of the ProShares Short VIX Short-Term Futures ETF (SVXY) was consistent with its objective and reflected the changes in the level of its underlying index. We expect the fund to be open for trading today and we intend to continue to manage the fund as usual.”).

What about today after market move? Makes sense?

lulz

Where can one get real time quotes on SVXY-IV?

Many offer real time IV to their clients. Finding the ticker symbol might require a call to their help desk. Schwab’s ticker is $SVXY.IV, Fidelity’s is SVXY/IV

Hi again Vance, not sure if you still active here? Do ETF/ETNs etc have to pre-announce splits?

Hi CK, I don’t know if it’s a legal requirement but in all cases I’m aware of there has been a pre-announcement. Seems like there’s usually more than 2 weeks notice. If the fund has options there’s definitely some pre-warning necessary to get the new options series ready.

awesome, thanks! Yes, I was worried because I’ve looked at some historical pricing data and post option pricing doesn’t look good. I know they give you equal amount in return, it just seems scary to hold through on options.

Thank you very much for your work.

At present, there is about over $1B asset for SVXY.

http://www.proshares.com/funds/svxy_daily_holdings.html

Thanks Peter. I don’t update this all the time, but my number was quite old. I suspect a lot of people are going to get burned during the next significant volatility spike.

Hello Vance, hope you’re doing well. Today market fell but VXX also fell. Is there any interesting reason. Thank you for the advise

Is it only me who thinks that SVXY has been tremendously flat (going sideways) the last month compared, to what we´re used to?

looks like its heading down to test $91 support… that’s the 200 day moving average for the 4 hour chart….

Hmm, I thought that technical analysis ain´t something that can be used due to its special nature, but I may be wrong. Which site or tool are your conclusions based upon? Just curious to learn.

i use the 200 day exponential moving average for a 4 hour chart.. it has bounced off of it 3 times this year.. i tend to look at 15min, hourly, 4 hour and daily charts.. the daily showed support at $99 which held (using 51 day exponential moving average.. ) i look at the 8 day, 21 day, 51 day and 200 day of each above mentioned charts… my program is thinkorswim

but any program will work, even sharpcharts… also full stochastic’s helps a lot, even bolingerbands … I dont see why any stock would not work with technical analysis, unless its thinly traded

Thanks, and sorry for the late reply. What I ment was that for the spikes that can sometimes last for months, these would be very difficult to see coming by using traditional analysis tools, isn´t that right?

Thanks for all the good info here. One question.. where it says “VIX futures occasionally go on a tear, turning the short sellers’ world into something Dante would appreciate.” Would a stoploss or trailing stop not protect SVXY holders or VIXY short CFD holders against such a tear, and close the trade before armageddon or could this happen overnight even? Since the opening, there were never a nightly change in price of more than 10 % (plus or minus).

HI Alf, Overnight risk is certainly an issue. My simulations suggest that since VIX futures inception the max overnight spike in VXX was 17%.. The other problem is flash crashes, Spiking volatility might result in inverse vol ETP prices that gap down. When a limit order is triggered it usually turns into a market order. Market prices in a flash crash might be well below the limit price. You risk being stopped out at the worst possible time because many times VIX levels will drop rapidly as people realize the sky isn’t falling after all…

Thanks Vance! Hmm, it´s strange if VXX had 17% but that I did not find such an overnight spike with the VIXY minute data set that I have. So instead of trading a reverse index such as SVXY, would it be better – for the flash crash situation – to go short with a CFD on a long instrument, such as VIXY?

Hi Alf, I re-did the calculation the number I see now as the biggest VXX overnight spike (previous day close to open) was +23% on 22-Jan-08. VIXY was not trading then so not surprising you don’t have that data. For short VIXY you don’t have the termination scenario to worry about, but a big volatility spike could lead to losing more than you initially put at risk–something that the inverse funds avoid. They essentially look like a zero price put that’s included with the inverse vol funds.

Hi Vance.

First of All. Thanks for such an amazing amount of infos available on this website.

Do you think is it possible to calculate the expected SVXY value on a certain date knowing the difference between F1 and F2?

Kindest Regards

Federico

Hi Federico, That’s a very good question. The trick is accurately modeling the curve between the futures. If you have a good estimate for the future F1 & F2 values then it is just known math to compute SVXY’s future value from those. Of course you have to assume the VIX futures term structure does not shift, so obviously the estimate has some severe limitations.

Hi Vance, what happens if svxy terminates due to a black swan event and I am short puts that expire in the future… Am I still liable for my short puts if the stock has terminated? I had this discussion with a friend and he seems to think that I would not be liable since the stock does not exist… Can you please shed some light on that… Thank you for your time and knowledge..

Hi Sal, My expectation is that the owners of SVXY puts would exercise them. Since the stock no longer exists the Open Clearing Corporation that is the clearing house for options would likely invoke its power to fix cash settlement prices in lieu of delivery of the underlying security ( Section G https://olui2.fs.ml.com/Publish/Content/application/pdf/GWMOL/Merrill_Lynch_Direct_Options_and_Clearing_Corporation_Prospectus.pdf ). This settlement price would likely be the Closing Indicative Value of SVXY which would be zero or higher, depending on what the VIX futures levels were at termination. Your loss would be the Strike Price of the option minus the Closing Indicated Value minus the premium you received when you sold the put.

Hi Vance,

Thank you for all your insight and advice, I’m looking for ways to protect against the next “black swan event”.. I’m a seller of puts in SVXY at a price range of $70-$75.. usually 1-3 weeks out… I’m considering going 4-6 weeks out and buy an equal amount of puts at a $45 range, it would cost about 20% of what I make and protect about 65% of my money… plus I can go through selling puts multiple times before my long put expires… would this work? what happens if the stock terminates before my expiration? I imagine I would still be responsible for buying the stock at $70 but I can still exercise my long puts at $45, right? thank you for any advice….

HI Sal, This question is outside the range of what I’m willing to answer for free. If you want engage me for consulting you can contact me at [email protected] .

Hello Vance,

as you know so many about the SVXY, can I ask you for your personal trading

strategy of SVXY, or other volatility-products?

Best regards

markus warnecke

Hello Vance. I am trying to get my mind around the risk of SVXY termination in case of a massive spike in volatility. I grasp the risk of a massive 80% type spike in a day, but what about a sustained spike that lasts several days but each day is more in the 20-40% range. In other words, does the daily resetting eliminate the termination risk for all but the intense one day swings?

The daily resetting functions as you say, it limits the termination risk to >= 80% intraday moves. Successive down days in the 20 to 40% range would really drive down the price, but wouldn’t cause termination.

how many shares are there of svxy?

etfdb.com reports shares outstanding as 6.4 million shares

HI Vance,

how can I view SPVXSPID on something like bigcharts, it doesn’t seem to recognize the symbol… from what I can see, that symbol did not double in price during the 2008 crash… Is that correct… I was first trying to compare SVXY to the $VIX futures but noticed when that went up over 50% on June 29th, SVXY went down less than 20%… so it wasn’t a 1 for 1 move… then I re-read your article again and noticed you specifically mentioned the symbol SPVXSPID was its direct comparison…

Thanks again!!

Sal S

Hi Sal, You can chart SPVXSPID here https://markets.ft.com/data/indices/tearsheet/summary?s=SPVXSP.ID:PSE It doesn’t track SVXY directly, SVXY is the daily resetting inverse of this index so the chart won’t help you. During the 2007/2009 period my simulations show SVXY would have dropped from 40 to 3.5. Regarding your 29-June observation, I suspect you were looking at the front month future only. SVXY is always tracking a mix of the front and second month futures, so you have to look at the correct combination of the two to understand the SVXY move.

Hi Vance,

Just wondering how the assignment process works in the case of SVXY. Say I sold strike 5 SVXY 150 puts of the July monthly options, and on expiration day the ETF closes at 149.50 and I decide not to close the position before 4:15 and to get assigned. What do I actually get? I am guessing 500 shares of the ETF, but just want to make sure. Thanks!

Hi Robbie, Yes, if you are in the money your options will be exercised. Normally you would get 500 shares. It turns out that SVXY has a stock split 11-July-17, so in this specific case you would get 1000 shares of SVXY, which would be trading around $75 at that point.

Termination is a nontrivial possibility for SVXY. What do you think is the most rational way to hedge this if you are long SVXY and have some calls.

You sir are a prophet, hoping you found a way to hedge if you bought it.

Hi Vance,

Many thank for this very good synopsis! I have a question. You wrote: “…SVXY has done two 1:2 splits to bring its price down into optimum trading levels”. Do you know the price of SVXY when these splits usually appears? I`m asking, because the current price of SVXY has become quit high and the dealing with options became quite expensive if you have just a small account. Or, do you know others ETF’s (like SVXY) and options dealing is possible?

Best regards

Markus

I’m not Vance but I see the split dates were 10/05/12 and 1/24/14, plus of course the recent one a couple weeks ago 7/17/17. I didn’t look up the price history again but if memory serves it was when the price was in the 150+ area…I know the one last month took place at 170 to 85 but was announced around the high 150s or 160ish level.

Thanks Steve!

Hi Markus, The only other inverse short term volatility fund I know of is Rex ETF’s VMIN. I’m sure the bid/ask spreads are wide but you might be able to get good mid-price fills with limit orders.

Vance

Hi Vance,

I have a question about SVXY. I currently own the stock and it is a large part of my portfolio.. I sell call options and then get back in the stock during market dips… I’ve done quite well, 36% return in 2016 and 18% return so for this year.. I even recovered nicely from the August 2015 correction… My question is that can I loose my entire stock during a “Black Swan” event? Or will I be able to “wait it out” like I did in 2015? I’m not margined against the stock at all (fully invested with my capital)…

Thanks

Sal S

Hi Sal, The short answer is yes. It is possible for XIV to be wiped out in a single day if there is a large enough jump in the underlying VIX Futures. For more info see https://www.sixfigureinvesting.com/2011/06/ivo-and-xiv-termination-events/ Ironically a low starting value of the VIX probably makes termination more likely because it’s much more likely that the VIX would double from a low previous close from say 12 to 24, rather than a move from 24 to 48.

Vance

Vance,

Thanks for the good synopsis. One thing I would like to add. K-1s are issued for SVXY as it is listed as a partnership. Any comment on this as a detriment to holding?

K-1s do add complexity to your tax return and it seems like they are always late to arrive, but my experience with them(not extensive) is that they don’t significantly change your tax burden. According the ProShares note (link below) it has section 1256 style treatment where all gains/losses are allocated as 60% long and 40% short term.

http://www.proshares.com/faqs/volatility_commodity_currency_proshares_taxation_faqs.html queston one.

HI Greg,

The June 27, 2011 event was a 8:1 stock split (forward, not reverse split). I think VelocityShares was trying to get the price down to a more tradeable range. I’ve attached ZIV’s performance (using VIX futures data before ZIV’s inception) to show its 13 year history. https://sixfigureinvesting….

Here is SVXY from 2004: https://www.sixfigureinvesting.com/wp-content/uploads/2017/03/svxy-2004.jpg

Best Regards, Vance

Thank You Vance I only wish I found this site before I invested in UVXY. You have been a great help.

Hi Vance

Should we be conceared that the market is up the last few days and Svxy is down? Is this a sign that it is time to get out. I really value your opinion as you are an expert in this field.

Thank you for your help

Greg

Hi Greg, The risk factors are definitely higher when the VIX & VXX start going up even when the market is up. It’s a sign that people are hedging heavily Of course people are often wrong, and it is notoriously tough to call the tops.

Hi Vance – Thanks so much. This really helps me. Can you explain what happened in August 2015 and why SVXY had a more severe correction than HVI.CA for 2 weeks? I am in Canada and trying to understand what happened during that time (HVU seems to be a steady upward trend over the past 5 years) where SVXY had that more nasty correrction. I know there will always be ups and downs, but SVXY has not recovered to the August 2015 highs, but HVI has.

Hi Matt, Most likely the divergence is because HVI’s index uses the 4PM ET values of the underling index SPVXSP as the close values instead of the 4:15PM values that SVXY and XIV use. This link provides more detail http://www.horizonsetfs.com/horizons/media/pdfs/Educational/The-Mechanics-of-HVI-HVI-Explained.pdf This may seem hard to believe but there can be a lot of market dynamics in that time period. The other factor may be currency hedging impacts.

Vance

Vance,

Your articles have been extremely helpful to me in understanding how VIX-related derivatives work.

If Credit Suisse went bankrupt, since XIV is an ETN, I think any XIV shares I held would be worth $0.

If ProShares went bankrupt, or decided to terminate SVXY, since SVXY is an ETF, I think there would be underlying assets to back the SVXY shares, and I would recover something, if not the full value of the SVXY shares.

Am I understanding this correctly?

Thanks,

ALP

Hi ALP, I agree with your analysis. The XIV note is debt that’s higher priority than the Credit Suisse stock holders, but in bankruptcy it’s still reasonable to assume that there wouldn’t be an value left. The assets held in SVXY are tied to the SVXY shareholders so a ProShares bankruptcy should not materially impact the balances there. In general I think anyone paying attention should be able to exit these funds before a bankruptcy occurred.

I think a far more likely risk for someone holding an inverse volatility product is if an overnight geopolitical / natural disaster occurs or a intra-day flash crash that spikes the VIX.

— Vance

There is a risk of closure in XIV if the VIX rises too much in one day. Could the same thing happen with SVXY although it is an ETF which invests in VIX futures?

The threshold for XIV termination is if the futures index drops 80% in a day. For SVXY the prospectus does not explicitly state a threshold, but they reserve the right to terminate the fund for any reason, and they also state that the fund’s NAV can’t go below zero. The VIX futures that SVXY is short could take the fund into negative value if the futures jump enough, so it’s certain they would terminate the fund if it starts approaching zero.

VH- REally appreciate the prompt reply and the chart…i knew that splits were my wild card. Still…the logic may hold until the next split.

i know about contango loss and vol drag….my bet is that those, relatively small, daily losses will be dwarfed by the sum of the pair when VIX spikes.

Its really just dynamic hedging between the 2. Its far from perfect but its “not bad” because the prices are currently close.

i refuse to believe its coincidence ….

JUST/NUGT same price

FAZ/FAS same price

TMF/TMV sasme price (few weeks ago)

direxion is gonna make a killing and i want a piece… just need to finish the math in 6hrs…. Korea tested a nuc cuz the market needs a reason to drop tomorrow.

tnx again!

also note that VXX/UVXY = exactly 2.

and the august 13 2015 split was a week before the crash…and they equalized the prices of vxx and xiv…..the recent split achieved the same goal.

VXX and XIV cost the same this week – about $36. First time this has happened….ever. Buy the pair for $72.

I dont see how the price for the pair can go lower.

Do you?