Update

As of February 28th, 2018 SVXY will target -0.5 leverage instead of -1X. This change was in response to the events of February 5th, 2018 when a massive VIX futures spike occurred in the last 30 minutes of trading, probably in part due to the rebalancing required by the 2X UVXY and -1X SVXY funds. This change to SVXY will reduce its rebalancing requirements and make it less susceptible to a termination event if VIX futures were to increase 100% or more from the previous day’s close. This leverage change will reduce SVXY’s performance when VIX futures are dropping in value. Proshares Press Release

——————————————————————————————————————————————————————–

Just about anyone who’s looked at a multi-year chart for a long volatility fund like Barclays’ VXX has thought about taking the other side of the trade. ProShares’ SVXY is an Exchange Traded Fund (ETF) that allows you bet against funds like VXX while avoiding some of the issues associated with a direct short.

To have a good understanding of how SVXY works (full name: ProShares Short VIX Short-Term Futures ETF) you need to know how it trades, how its value is established, what it tracks, and how ProShares makes money with it.

How did -1X SVXY trade?

- SVXY trades like a stock. It can be bought, sold, or sold short anytime the market is open, including premarket and after-market time periods. With an average daily volume of 8 million shares, its liquidity is excellent and the bid/ask spreads are a few cents.

- SVXY has options available on it, with five weeks’ worth of Weeklys and strikes in 50 cent increments.

- Like a stock, SVXY’s shares can be split or reverse split—but unlike VXX (with 4 reverse splits since inception) SVXY has done three 1:2 splits to bring its price down into optimum trading levels. Unlike Barclays VXX, SVXY is not on a hell-ride to zero.

- SVXY can be traded in most IRAs / Roth IRAs, although your broker will likely require you to electronically sign a waiver that documents the various risks with this security. Shorting of any security is not allowed in an IRA.

- SVXY is subject to termination risk. Termination can occur (and did with XIV, a very similar fund on February 5th, 2018) if the daily positive move in the VIX futures market approaches or exceeds a 100%. ProShares guarantees that SVXY will not go negative so to protect themselves they will cover their short positions and terminate the fund if things get bad enough. For more on this see XIV Termination.

How was -1X SVXY’s value established?

- Unlike stocks, owning SVXY does not give you a share of a corporation. There are no sales, no quarterly reports, no profit/loss, no PE ratio, and no prospect of ever getting dividends. Forget about doing fundamental style analysis on SVXY. While you’re at it forget about technical style analysis too, the price of SVXY is not driven by its supply and demand—it is a small tail on the medium-sized VIX futures dog, which itself is dominated by SPX options (notional value > $100 billion).

- The value of SVXY is set by the market, but it’s closely tied to the daily percentage moves of the inverse of an index (S&P VIX Short-Term Futurestm) that manages a hypothetical portfolio containing VIX futures contracts with two different expirations. Every day the index methodology specifies a new mix of VIX futures in the portfolio. On a daily basis SVXY moves in the opposite direction of the index with a leverage factor of -0.5X, so for example, if the index (ticker SPVXSPID) moves up 0.3%, then SVXY will move down precisely 0.15%. This post has more information on how the index itself works. The index is maintained by S&P Dow Jones Indices.

- As is the case with all Exchange Traded Funds, SVXY’s theoretical share value is just the dollar value of the securities and cash that it currently holds divided by the number of shares outstanding. This theoretical value is published every 15 seconds as the “intraday indicative” (IV) value. Yahoo Finance publishes this quote using the ^SVXY-IV ticker. The end of day value is published as the Net Asset Value (NAV). The NAV is computed at 4:15 ET, not the usual market close time of 4:00 ET, because VIX Futures don’t settle until 4:15.

- If the trading value of SVXY diverges too much from its IV value wholesalers called Authorized Participants (APs) will normally intervene to reduce that difference. If SVXY is trading enough below the index they start buying large blocks of SVXY—which tends to drive the price up, and if it’s trading above they will short SVXY. The APs have an agreement with ProShares that allows them to do these restorative maneuvers at a profit, so they are highly motivated to keep SVXY’s tracking in good shape.

What did -1X SVXY track?

- SVXY makes lemonade out of lemons. The lemon, in this case, is the index S&P VIX Short-Term Futurestm that attempts to track the CBOE’s VIX® index—the market’s de facto volatility indicator. Unfortunately, it’s not possible to directly invest in the VIX, so the next best solution is to invest in VIX futures. This “next best” solution turns out to be truly horrible—with average losses of 5% per month. See this post for charts on how this decay factor has varied over time. For more on the cause of these losses see “The Cost of Contango”.

- This situation sounds like a short sellers dream, but VIX futures occasionally go on a tear, turning the short sellers’ world into something Dante would appreciate.

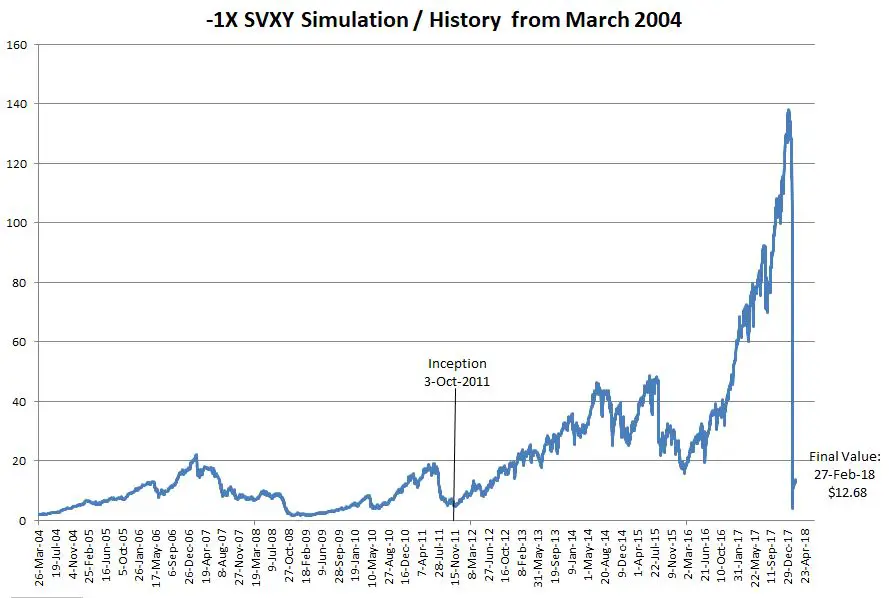

- Most of the time (75% to 80%) SVXY is a real moneymaker and the rest of the time it is giving up much of its value in a few weeks—drawdowns of +90% are not unheard of. The chart below shows SVXY from 2004 using actual values from October 2011 forward and simulated values before that.

- Understand that SVXY did not implement a true short of its tracking index. Instead, it attempted to track the -1X percentage inverse of the index on a daily basis. To maintain this -0.5X behavior the fund must rebalance/reset its investments at the end of each day. For a detailed example of how this rebalancing works see “How do Leveraged and Inverse ETFs Work?”

- There are some very good reasons for this rebalancing, for example, a true short can only deliver at most a 100% gain and the leverage of a true short is rarely -1X (for more on this see “Ten Questions About Short Selling”. -0.5X SVXY, on the other hand, would be up over 200% if it had been trading since the original -1X SXVY started trading 3-Oct-2011. It faithfully delivers a daily percentage move very close to -0.5X of its index.

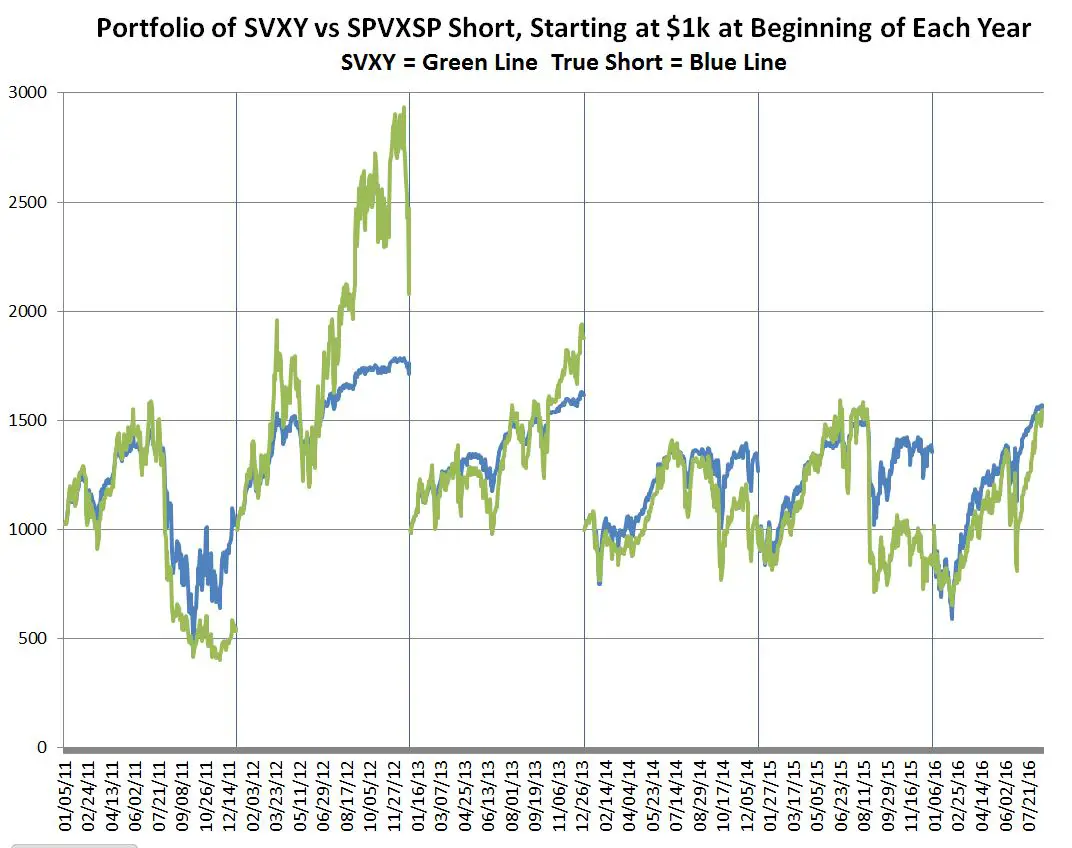

- Detractors of the daily reset approach correctly note that SVXY and funds like it can suffer from volatility drag. If the index moves around a lot and then ends up in the same place SVXY will lose value, whereas a true short would not, but as I mentioned earlier, true shorts have other problems. Even with volatility drag daily reset funds don’t always underperform. If the underlying index is trending down, they can deliver better than -1X cumulative performance. The chart below shows the relative one-year performance of SVXY and a true short starting with $1K invested in January for 2011 through 2016.

- For a more analytic description of what’s going on here see “A Hat Trick for Inverse / Leveraged Volatility Funds”

How did ProShares make money on -1X SVXY?

- An Exchange Trade Fund like SVXY must explicitly hold the appropriate securities or equivalent swaps matching the index it tracks. ProShares does a very nice job of providing visibility into those positions. The “Daily Holdings” tab of their website shows how many VIX futures contracts are being held. Because of the -1X nature of the fund, the face value of the VIX futures contracts will be very close to the negative of the net “Other asset/cash” value of the fund.

- ProShares collects a daily investor fee on SVXY’s assets. The fee is stated as a 0.95% annual fee, but it’s implemented by subtracting 0.95/365 of a percent from each share’s value every calendar day. With current assets at $1 billion, this fee brings in around $9.5 million per year. That should be enough to be profitable, however, I suspect the ProShares’ business model includes revenue from more than just the investor fee.

- Exchange Traded Funds like SVXY recoup transaction costs in a non-transparent way. Transaction costs are deducted from the fund’s cash balance—resulting in a slow divergence of the fund’s IV value from the theoretical value of the index that it’s tied to. This differs from the approach that Exchange Traded Notes (ETN) use, their theoretical value is directly tied to the moves of the index itself, so the ETN issuers must pay for transaction costs other ways (e.g., out of the annual investor fee, or other explicit fees). In the case of SVXY, this hidden transaction fee has averaged around 0.28% per year.

- One clue on ProShares’ business model might be contained in this sentence from SVXY’s prospectus:

“A portion of each VIX Fund’s assets may be held in cash and/or U.S. Treasury securities, agency securities, or other high credit quality short-term fixed-income or similar securities (such as shares of money market funds and collateralized repurchase agreements).” Agency securities are things like Fannie Mae bonds. The collateralized repurchase agreements category strikes me as a place where ProShares might be getting significantly better than money market rates. With SVXY currently able to invest around $250 million this could be a significant income stream. - I’m sure one aspect of SVXY is a headache for ProShares. Its daily reset construction requires its investments to be rebalanced at the end of each day, and the required investments are proportional to the percentage move of the day and the amount of assets held in the fund. SVXY currently holds $400 million in assets, and if SVXY moves down 10% in a day (the record negative daily move is -24%, positive move +18 %) then ProShares must commit an additional $20 million (5% of $400 million) of capital that evening. If SVXY goes down 10% the next day, then another $18 million capital infusion is required.

SVXY won’t be on any worst ETF lists like Barclays’ VXX, but its propensity for dramatic drawdowns (e.g. -91%! in the Jan/Feb 2018 timeframe) will keep it out of most people’s portfolios. Not many of us can handle the emotional stress of holding on to a position with huge losses—even though the odds support an eventual rebound.

The eye-popping inverse volatility gains in 2016 and 2017 pushed SVXY’s assets beyond VXX’s but with its February 5, 2018 reset it dropped well below that level. It will be interesting to see how the next few years go. I suspect we’ll see additional bloodletting as people rediscover short volatility can be very volatile in its own right.

Click here to leave a comment