LONGVOL and SHORTVOL Indexes (free)

$0.00

LongVol and ShortVol index calculations back to 20-Dec-2005.

Description

LONGVOL and SHORT are two new indexes distributed by the Cboe. They are intended to enable more robust VIX futures markets by quantifying trading strategies that even the buying or selling volume of VIX futures required to roll and rebalance short term volatility Exchange Traded Products. For more information on these indexes see Why We Need the New LONGVOL and SHORTVOL indexes

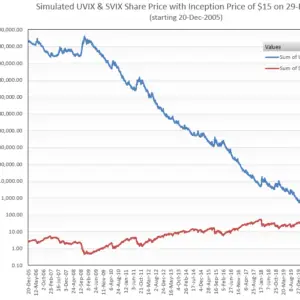

The spreadsheet includes simulated SVIX , UVIX, and ZIVB performance in addition to sheets with the SHORTVOL and LONGVOL indexes.

The time-weighted average TAS spread calculation was not included until January 2021. That change was coincident with the CBOE changing the VIX futures settlement time to be the same as the equity market closing times, typically 4 PM ET.

Related products

-

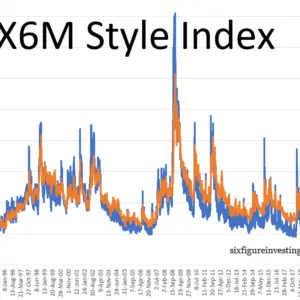

VIX6M Style Index Calculation From 1990

$149.00 Add to cart -

Velocity Shares -1X SVIX, 2X UVIX, and -1X ZIVB ETFs Backtest + Associated Indexes (free)

$0.00 Add to cart -

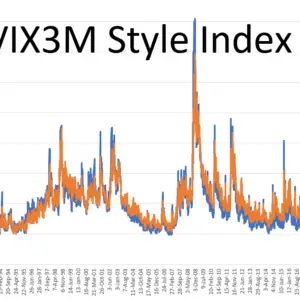

VIX3M Style Index Calculation Back to 1990

$149.00 Add to cart -

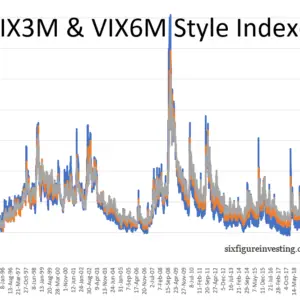

VIX3M and VIX6M Style Index Calculations Back to 1990

$199.00 Add to cart