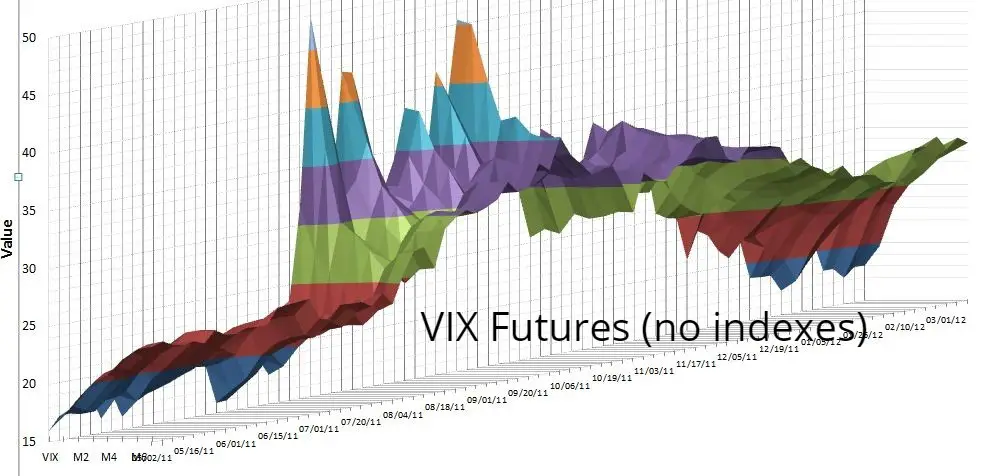

VIX Futures Data March 2004 – Most Recent Quarter

$99.00

Description

This spreadsheet integrates all available monthly VIX futures data from 2004 through the end of the most recent quarter (see this table for specific dates) and organizes it into a continuous-time series organized by the future’s order of expiration. This data can be used to compute volatility indexes like SPVXSTR, SPVXSP, SPVXMSTR, and SPVXMP but those calculations are not included in this spreadsheet.

This spreadsheet also includes a worksheet TermS that reports 7 months of VIX Futures data starting in March 2004, their associated expiration dates, and days to expiration for each futures for each trading day

The spreadsheet is designed for updates using the latest VIX Futures data and includes required expiration dates through the end of 2024.

I do offer a two spreadsheet combination that in addition to presenting the VIX futures data also generates the key volatility indexes (e.g., SPVXSTR & SPVXSP) and simulates the Indicative Value closing prices for the popular VIX futures based volatility funds. For more on this extended package see Computing Volatility Indexes and ETP Values

I offer a quarterly update service for these spreadsheets.

The source of the Cboe raw futures data is here: Cboe Volatility Index (VIX) Futures Data