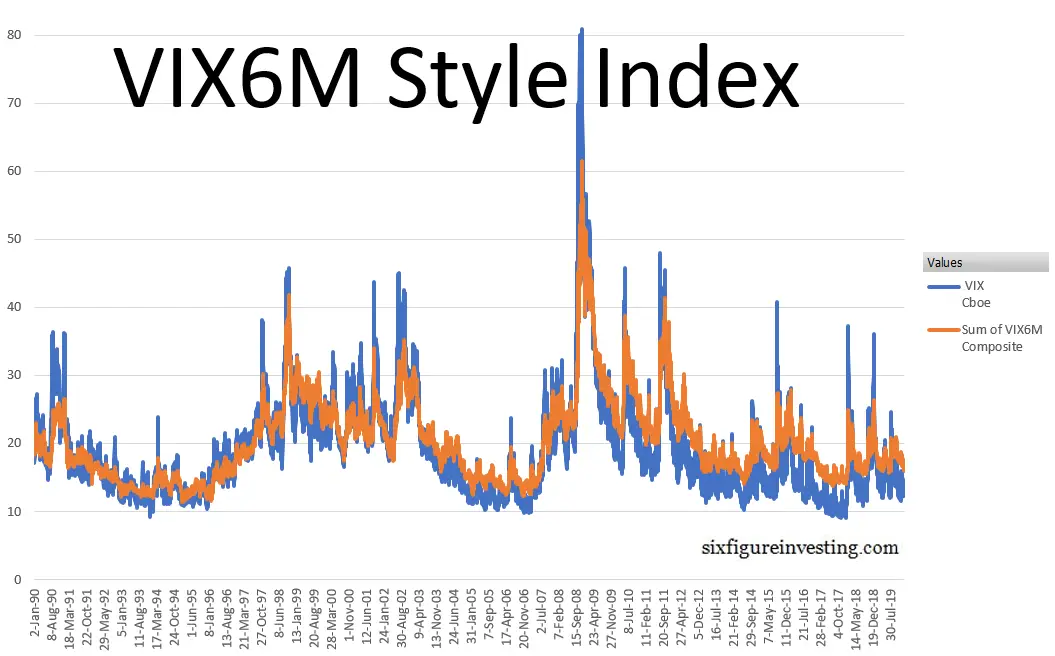

VIX6M Style Index Calculation From 1990

$149.00

Description

The VIX6M is a Cboe VIX® style index, which uses the VIX style calculation methodology but has a 184-day horizon instead of the VIX’s 30-day outlook. The VIX6M was introduced by the Cboe in 2013 (it was named VXMT at that point) and provided the historical appropriate calculations back to January 2008. I have taken the SPX option historical option and US treasury data and used the VIX6M methodology to compute VIX6M style results back to January 2nd, 1990–adding 18 years of daily close historical data. For details on this calculation, difference analysis, and long term trend analysis see Calculating a VIX6M style index back to 1990 and Calculating a VIX3M style index back to 1990.

I also offer a VIX3M style calculation back to January 1990 also as well as a combo product with both the VIX3M and the VIX6M indexes that is significantly cheaper than buying the two products separately.

The VIX6M style results are available in a spreadsheet that includes:

- Composite VIX6M that includes my VIX6M style calculations merged with Cboe data (giving Cboe data priority) starting January 1990. The indexes are updated through at least April 2023 (see this table for specific dates). My data is the day end close (4 pm ET) value only.

- The Cboe’s VIX data starting on January 2nd, 1990

- My stand-alone VIX6M style calculations from January 2nd, 1990 through February 26th, 2010 (I computed 2 years of data where Cboe data was already available to validate my calculations)

- The VIX/VIX6M ratio from January 2nd, 1990

- Thirty-day rolling min/max values for VIX/VIX6M (useful for evaluating long term trends in volatility)

The spreadsheet does not include the data or any of the formulas that were used to compute the VIX6M values, however, it does include formulas to make it easy to update the VIX and VIX6M composite data by importing the publicly available updated spreadsheets provided by the Cboe (VIX, VIX6M).

I also offer a quarterly update service for this spreadsheet. For more information see https://www.sixfigureinvesting.com/2011/02/quarterly-update-service/

My calculations typically do not exactly match the Cboe’s results on the days when both results are available (January 2nd, 2008 through Feb 26th, 2010). The median difference is -0.02% and the standard deviation of differences is 0.22% so the results are usually very close. However, there are a few 20 days with differences larger than +-2%. which occurred on very volatile days. I discuss the root cause of these differences in Calculating a VIX3M style index back to 1990.