Unlike the S&P 500 or Dow Jones Industrial Index, there’s no way to directly invest in the CBOE’s VIX® index. Some really smart people have tried to figure out a way, but there’s just no way to do it directly with something like a VIX index fund. Instead, you have to invest in a security that attempts to track VIX. None of them do a great job. The rest of this post discusses going long on volatility— if you think volatility is going to go down see Going Short on the VIX.

For the average investor there are five ways to go long on VIX:

- Buy a leveraged exchange-traded product (ETP) that tends to track the daily percentage moves of the VIX index. The best of these from a short term tracking standpoint is Volatility Shares’ 2X leveraged UVIX. The other choice is ProShares UVXY.

- Buy Barclays’ VXX (short term), VXZ (medium-term) Exchange Traded Note (ETN) or one of their competitors that have jumped into this market. Volatility tickers gives investors a full list of volatility ETN/ETFs. For more information on VXX see How Does VXX Work?

- Buy VXX or VXZ call options ( ProShares’ VIXY, VIXM)

- Buy UVIX options ( 2X leveraged ETF using the new LONGVOL index)

- Buy UVXY options (1.5X leveraged version of the short term rolling futures index used by VXX)

- Buy VIX call options / short VIX put options (Thirteen Things You Should Know about VIX Options

Aggressive

The choice is not for the faint of heart. VIX’s moves are often extreme, so if you bet wrong you can lose money in a big hurry (think 15% or more in a 24-hour period), of course, there is the equivalent upside if you get it right. In my opinion, these are tools for day traders that stay stuck to their screens and have an excellent sense for market direction. Unless the market is in a sustained high fear mode (e.g., February through March 2020) these funds (e.g, UVIX, UVXY) will often erode dramatically over a multi-day period. But if you are looking for the best ETN/ETF to track the VIX short term moves this is as good as it gets.

Volatility Shares UVIX and ProShares’ UVXY, are Exchange Traded Fund (ETF). The good news is that the financial backing of an ETF, unlike an ETN is not dependent on the creditworthiness of the provider because they are guaranteed to be backed by the appropriate futures/swaps. The bad news is that those futures change the tax status of the fund to be a partnership—which requires filing a K-1 form with your tax returns. Typically this is not a big deal but requires a little extra work at tax time if held in a taxable account. In tax-sheltered accounts like IRAs, there’s typically no effort required a tax time to handle these.

While UVXY and especially UVIX do a respectable job of tracking the VIX on a daily basis, they will not track it one to one. These funds are constructed using VIX volatility futures that aren’t constrained to follow the VIX—sometimes they are lower than the VIX, sometimes higher. The VIX index tends to drop on Fridays and rise on Mondays due to holiday effects in the SPX options underlying the VIX—the VIX futures don’t track these moves and hence the ETPs don’t track them either.

Mainstream

The second choice, buying non-leveraged volatility ETNs like VXX, is not as twitchy, but be aware that the VXX will definitely lag the VIX index (think molasses), and it is also not suitable as a long-term holding due to the fact that the VIX futures that the fund tracks are usually decreasing in value over time. This drag, called roll loss occurs when the futures are in contango. It usually extracts 5% to 10% a month out of VXX’s price. Proshares has an ETF version, VIXY, that tracks the same index as VXX—if you’d rather use an ETF for playing the VIX this way.

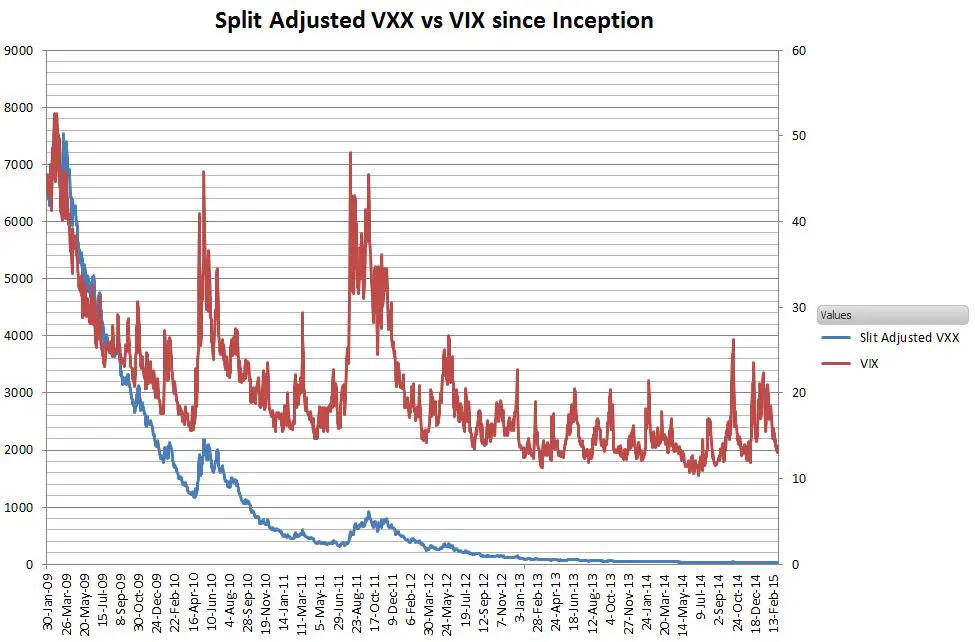

Volatility Funds vs the VIX

The chart below shows how VXX’s price has fared relative to the VIX. The VIX is a range-bound index (scale on the right side of chart) that stays between around 9 and 80, whereas VXX erodes over time and must be reverse split to keep its price in a reasonable trading range.

On this scale, you can see that VXX “tracks” the VIX only in the loosest sense. Given its dismal track record, it’s surprising that VXX usually trades over 50 million shares a day. I think the allure comes from its reliable negative correlation with the equity markets (-3x). If SPY has a significant down day, you can be pretty confident VXX will have a good day—unlike some investments like gold.

Options

On June 1st, 2010 options on VXX were introduced and became almost immediately successful. I think retail investors flocked to them because they lacked most of the VIX option eccentricities—such as European exercise, different expiration dates, VRO based settlement values, and Greeks that are generally wrong. VXX options have VXX as the underlying, which avoids the perpetual confusion associated with VIX options where volatility futures behave much more like the underlying than the VIX. VXX weekly options are also available.

UVXY & UVIX options are quite expensive due to the volatility of the ETF, but if want to increase your leverage, or reduce your capital exposure they are a possibility.

- The bid / ask spreads can be wide. Never pay what is offered, use limit orders and split the bid/ask prices (e.g., if the spread is 3.40/3.80 and you want to buy, offer 3.60 or 3.70 with a limit order.) More on trading VIX options here.

- The VIX options are European exercise, unlike most equity options—practically this means the VIX options will predictably match (approximately) the VIX index, only once a month—the moment they expire.

- The posted greeks (delta, gamma, etc.,) are almost always wrong. See more here.

- Like all options, their premium value erodes with time, especially as you approach expiration.

If you want to trade the VIX you are probably hoping to speculate on its big swings, or you are trying to hedge your portfolio against big, sharp declines. If you want to speculate, be prepared to move in a hurry—the VIX drops quickly once the market angst subsides. Most of the action is over in a few days.

If you want to hedge over the longer term I’d avoid these securities and look at the longer-term strategy funds described next.

Strategy Funds

There is one volatility-based strategy fund, PowerShares’ PHDG is a portfolio solution that combines equities (S&P500) and a volatility hedge.

The downside of a volatility strategy fund is that sometimes it significantly underperforms regular equity positions, it doesn’t respond quickly to fast volatility events like overnight scares or flash crashes, and it doesn’t track daily VIX moves all that well. However, volatility strategy funds should do very well in bear market scenarios, taking advantage of the strong backwardation in VIX futures that occurs during panicky times.

Bottom line, it’s very tempting to try and guess when the VIX will spike, but in practice, most people don’t get the timing right. If you buy options or ETPs like UVIX, UVXY, or VXX you will likely see your money wither away. If you want to trade long volatility, probably the best strategy is to wait until there’s a volatility spike already in progress. Most likely it will be a false alarm, but if the downturn develops into a full-scale correction or bear market there are some serious money-making possibilities.

Are xvz and vixm the same thing except for minor differences such as fees?

Barclay’s vxz is quite similar to vixm. The biggest difference is that VXZ is an ETN and VIXM is an ETF. Barclay’s XVZ is a pretty different animal. It shifts its assets based on market conditions.

Best Regards, Vance

Can someone explain to me why when the VIX is up almost 5% today (2/27), VIX calls are down (some significantly) and puts are up ? Seems bizarre…

VIX options are effectively tied to VIX futures not the VIX itself. E.g., the May options track the May VIX futures. Unless very close to expiration the futures tend to have a mind of their own. For more see https://www.sixfigureinvesting.com/2010/01/trading-vix-options/

Hi Vance, why does VXZ decay less than VXX?

Hi Gregory, Short answer is that VXZ dynamically shifts the VIX futures it holds, often holding some short positions to offset the contango losses. For a longer answer see: https://www.sixfigureinvesting.com/2011/09/under-the-hood-of-xvz/

Thanks again Vance, I’ve had nearly 2 years of success thanks to your blog.

Hello Vance,

Compared to their respective lows in mid Dec 2015, VXX is up about 17.5%, and $VIX about 16.5%, at today’s close.

From your excellent discussion, this implies that F1 and F2 have been in backwardation during this time, rather than the much more typical contango. Considering that $VIX has been declining since Jan 20, this seems especially significant.

How do you understand this change, and what factors do you think would sustain or curtail it ?

for the record, the referenced close is 2016-03-15

The VIX futures were slow to move back into contango, even though the VIX was declining. Watching the behavior of the VIX (reflecting SPX option premiums) vs VIX futures is a very interesting exercise. Not clear which market is right more often.

is there any chance TVIX to go 20 again ?

It would take a 2008 style crash get it that high,

— Vance

any chance JNUG to trade 300 again ?

It would take a massive rally in Gold. I’d say no.

At the moment the best of these from a short term tracking standpoint is ProShares’ UXVY and…

You need to correct the symbol in your text. UVXY is the correct symbol.

Thanks. Fixed…

Hi Vance, glad to see people out there also interested in VIX. As I am new to VIX, I have a probably obvious technical question regarding selling call options of VIX: what happens if the call options are ITM upon expiry? Will the options be exercised? If this is the case, what exactly would I be selling since VIX cannot be directly invested?

Thanks!

Hi there Vance,

What are your thoughts about profiting from the tracking errors in VXX as well as the contango that it experiences. For example, buying a Feb 22 ATM VXX put while simultaneously buying a Feb 19 ATM VIX call. Even if VIX does experience a large spike, the VXX put would be minimally affected on the downside and the VIX call would fully realize the spike. This would work especially well if the spike only lasted for a few days, which it seems to usually do. Additionally, if it does turn out to be a long-term spike, the profit from the VIX call would more than likely surpass the premium paid for the VXX put.

Thank you for the article and your time.

Hi Adam, Using 31-Dec numbers your ATM put S42 would cost around 2.94 (VXX at 42.5) and your ATM call (S14) around .83. To get a 50% profit on the position you would need VXX to drop about 13% in the next 8 weeks. Not a bad bet, but any significant volatility uptick in the interim would derail the put. If volatility goes up you would need VIX to go up to around 18 to breakeven. Again not impossible, but a significant move. Don’t know what tracking error on VXX you’re referring to. It doesn’t track the VIX particularly well, but that’s because of lethargic VIX futures and contango. VXX tracks its index very well. Hopefully you know that the VIX Call will not track the VIX, but rather the Feb VIX futures.

–Best Regards, Vance

Hello Vance. You say that contango extracts 5-10% from VXX. Should we expect that decay to exist in the long term? I’m considering buying SVXY shares and just hold them “forever” to profit from VIX futures contango.

Hi Vedast, The big problem is volatility spikes. You could easily see 50%+ of the value of your position vanish in a few days. Yes, eventually it will probably recover, but it might take years. Not many people can stomach that big of a drawdown without pulling out. Using a ratio like VIX/VXV to manage your position would probably help some, e.g., my backtest for XIV, stay in if the ratio is less than 0.917 limited the drawdown to “only” 25%.

— Vance

Hello Vance. Thank you for your reply. I realize that volatility can be really high, and I’d try to compensate that with other parts of my portfolio. Do you think that the monthly expected returns in the long run are as high as 5%-10% per month (minus VXX and SVXY annual fees)? I wouldn’t care dealing with big drawdowns if I have that kind of expected returns 🙂

HI Vedast, Using 28Dec11 through 28Dec12 the VIX was only down 7% for the year, but XIV’s monthly CAGR was +7.5%. This was a quiet period, but it shows what a contango powered period is capable of. By the way, I expect 2013 to be a more volatile year than 2012–maybe something like 2007.

— Vance

I strongly disagree on CVOL. Yes, it is thinly traded but spikes heavily at times of uncertainty. It may trade 25,000 in a day then trade 200,000 a week later. I like it much more than VXX which is not as volitile. I think VIX ix going to 50-60 in early 2013 and CVOL will spike more than any other VIX trade and at a much higher % than VXX.

Hi, I hadn’t looked at CVOL in a while. I agree the volumes are respectable and the spreads aren’t too bad. The contango losses are bad, but much better than TVIX / UVXY. I’ve changed my post to put CVOL equivalent to UVXY. However medium to Long term I think CVOL will go away. Citigroup should have reverse split it by now if they plan to go with it long term. With only $6 million in assets they will probably let it fade away/ delist. It will probably take a year for that to play out.

— Vance

the best way to hedge a long portfolio is holding etfs that pay good dividends and reinvesting when it hits the bargain basement. When you have almost 13 million shares of SPY we are going to be PAID no matter what the market does.

You can’t trade the VIX directly. You can trade VIX options, which are based on VIX futures, or VXX / VXZ and their options–which are based on a two month rolling mix of VIX futures. See my “popular posts” section on the right side of my blog for more info.

Is trading the Vix like trading a stock or does it expire like an option

Hi Sam, I assume your question relates to the VXX, because you can’t directly trade the VIX itself. The VXX doesn’t expire, so in that sense it is like a stock. However the VXX will never behave like a good growth stock with the prospect of growth every year. Instead it is fated to bounce between two levels, one established by elevated volatility, and the other established by the moderate movements of a quiet market. In fact, its long haul prospects are even worse than that–because its sponsors must continually roll over the futures contracts it’s based on there is a structural erosion factor built into the VXX. Over the long run (multiple months) the VXX will always go down. For that reason I don’t consider the VXX a buy-and-hold candidate. You should only buy it when you think the market it going to fall sometime in the near future.

Hi Vance,

I didn't realized this was your new blog. Anyway I like the new look and feel and have replaced the old blog with the new one on my blogroll.

Hoping seven or eight figure investing is just around the corner,

-Bill

Hi Bill,

Thanks for the feedback. I’m hoping to learn more about SEO, and my son, who is a web designer informed me that WordPress was the way to go. It was a significant learning curve, I hope it’s worth it. Thanks for the bogroll mention, I really appreciate it.

— Vance

Hi Paul,

The vol curve is not something that I follow directly. Bill at http://vixandmore.blogspot.com/ is a better resource.

As a longer term investment VXX has shown that it doesn't track the VIX index short term volatility metric particularly well. Their methodology requires them to roll over from current month to next month volatility futures on a daily basis–which hurts them if the next month futures are valued higher than the present month (“in contango” in futures terminology)–which seems to the be the typical case. VXZ is not very popular (only $30M in assets compared to $704M for VXX), so I suspect the bid/ask spreads are wide.

can i hold uxvy for long term ,say 12 month or longer

Hi Benson,

Historically UVXY declines around 90% a year, so holding onto it for that long would almost certainly be a bad idea.

— Vance

Hi Vance,

Thank you for reply my question.

So what make it declines 90% a year,is that all ETF is not for long term holding. for example like NUGT ,DUST.

Hi Benson, Most ETFs are ok for long term holding. The problem in general with leveraged ETFs (e.g, 2X and 3x) is compounding loss (see http://finance.yahoo.com/news/7-mistakes-avoid-trading-leveraged-130053722.html). TVIX has an additional problem, negative roll yield. For more see this post. http://vixandmore.blogspot.com/2012/02/four-key-drivers-of-price-of-tvix.html

Best Regards,

Vance

Hi Bill,

Thanks for the correction on the beginnings of the VXX/VXZ ETNs. I have corrected the post to reflect the January 2009 launch.

— Vance

what does the stock price differential between VXX and VXZ tell you about the term structure of vol? Early 2009 both ETNs were priced above 100 and now a big difference. Has vol curve really steepened that much? Would you view those as good vehicles for playing a flattening, or steepening, of vol curve?

thanks

I'm delighted to see someone else who is interested in the VIX and volatility — and has some excellent content on the subject.

I am with Charlie in that the best way for a retail investor to assemble a pure play on S&P volatility is with a straddle on the SPX or SPY. Here an investor also has the benefit of a favorable bid/ask spread and liquidity. The next best choice is probably VIX futures, from which, as you point out VXX and VIX options (for all practical purposes) are derived.

As an aside, you may want to check your data source on VXX to make sure you have data going back to the 1/30/09 launch.

Cheers and welcome to the blogosphere,

-Bill

I would say the best option if you want to go long S&P volatility is a near-term delta-neutral straddle as opposed to VXX tracking errors and/or going long VIX futures options.

Is there any chance TVIX to go 20 again ?