There are over 2800 ETFs right now, with more in registration. This explosion of alternatives is great for driving down fees and giving investors choices. However once we figure out what we want to buy, we often discover the fund we chose is lightly traded—perhaps only hundreds of shares are traded on any given day.

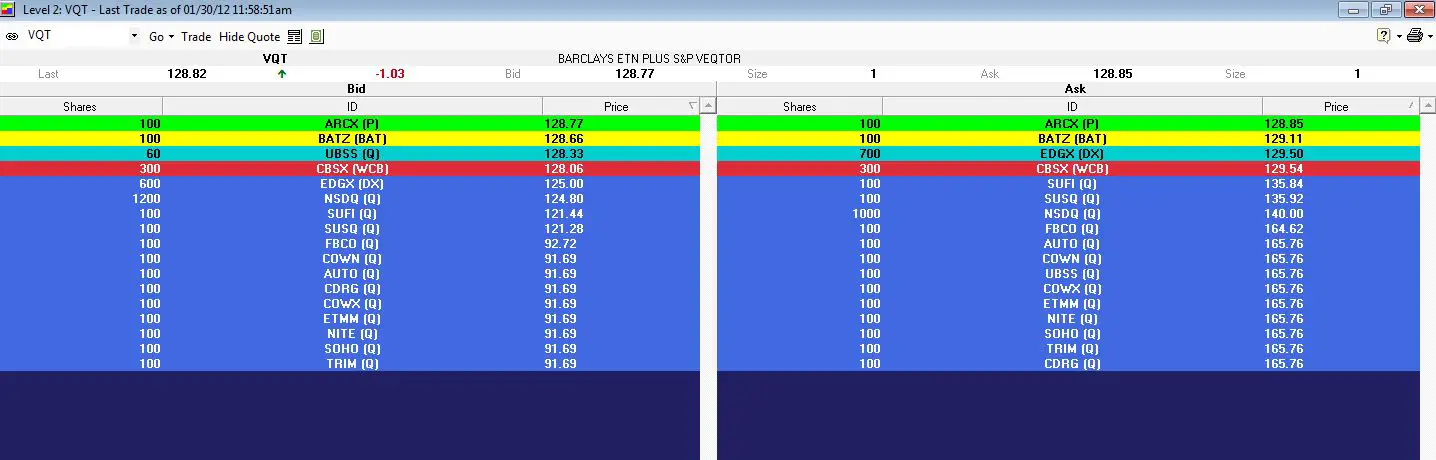

With a lightly traded fund, the bid/ask spread is usually significantly wider than the one-cent spreads we see with the big ETF funds and stocks. The thumbnail below (click to enlarge) is from Fidelity Active Pro’s order book of Barclays’ VQT in early 2012. At that point, it had almost $200 million in assets under management—but its Level 2 order book was still ugly.

The best-quoted bid/ask spread is $0.08—not great but only a 0.06% hit on the overall value of the trade. However, those quotes are only for 100 shares. For 200 shares the spread widens to $0.44, and for 1000 shares the visible book widens to 125/129.54—a chilling $4.54 spread.

If someone was careless enough to enter a market order to sell 1000 shares the likely result would be an average price of 126.86—1.5% lower than the best bid price. It’s possible that a market maker would step in to prevent this sort of carnage but I doubt it.

This brings us to rule #1: Always use limit orders unless the security you are trading has narrow spreads and deep liquidity.

However, things are not nearly as grim as they seem. Unlike stocks, ETFs have built-in processes to provide liquidity when needed. This share creation/redemption process enables companies designated as Authorized Participants (APs) to routinely respond to the market’s demand/disdain for ETFs shares in 25K or 50K+ share increments.

For example, if market forces are causing an ETF’s price to drift higher than its intraday net asset value (iNAV), then an AP can step in and execute a profitable, essentially risk-free arbitrage transaction that creates more shares. The AP (and the ETF) are happy to create shares until the increased supply has driven the market price down close to the iNAV value. The reverse situation, with the ETF price below the iNAV is also profitable for the AP to correct by redeeming shares.

This brings us to rule #2: Know the IV / iNAV value of your ETF/ETN before you trade.

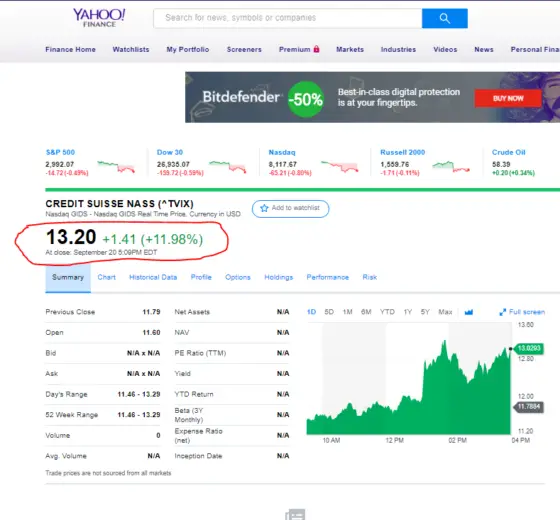

The indicative Value (IV) or iNAV value is available on Yahoo Finance by adding a “^” to the beginning of the symbol and a “-IV) at the end. For example, the iNAV symbol for UVXY is ^UVXY-IV. On Bloomberg add IV:IND to the end of the symbol to get, UVXYIV:IND. For Schwab, start with $ and end with .iv , $UVXY.IV. For Fidelity add /I, for examplem UVIX/IV. See the picture below for an example IV quote. You will probably will not be able to buy or sell at the IV price, but you should be able to get close.

Knowing the IV value will help you recognize if the market is out of balance. Normally the IV will be close to the middle of the bid/ask spread—if not be especially careful.

If your trade is going to be large (e.g., 10,000 or more shares) you should work with liquidity providers like Wolverine, KCG Holdings, or Wallachbeth to see if they can facilitate your trade. These firms can provide great quotes for even million share transactions on lightly traded ETFs, see this excellent webcast from ETF.com for some demos. This post gives a nice overview of the institutional landscape for trading ETFs.

If your trade is small, say 100 shares or less, then a limit order should be fine. If you want to score a few pennies on the spread you can try placing your order between the bid/ask price and see if it fills. If it doesn’t execute you can cancel your order and improve your offer until it does complete.

For larger orders, things get a bit trickier. I’ve tried “all or none” limit orders without much success. What has worked for me is a limit order set within the bid/ask price, biased a few cents in the market maker’s favor. If I’ve specified a good limit price I will see partial fills in 100 share blocks over the span of a minute or two until the order is complete. You only pay your commission once, assuming the order completes within the trading day. Of course, there are risks to this; the market might move against you, or liquidity might be exhausted, but compared to the risk of a lousy price these are good risks to take.

And rule #3: Even lightly traded ETFs typically have good liquidity, but it’s your job to coax it out.

For more on this see https://www.sixfigureinvesting.com/2015/08/determining-liquidity-of-low-volume-etf-etn/

Hi Vance

FYI. To get the NAV inside of Fidelity’s Active Trader Pro it is VQT/IV

– Arden

Hi Arden,

Thanks for the tip. Just today I was wondering if Fidelity was getting around to supporting IV quotes. I added the info to the post itself.

— Vance

Hi Vance,

A couple of weekend questions on GASZ for you. I will be taking a closer look at this one.

(1) Any idea of how this is performing against how you would expect it to perform? Particularly, it is making money in this shart contango environment. I am wondering how it would perform it a flat or slightly contango environment – i.e., does it need strong contango for positive returns.

(2) Did you see Lee’s comment over on VIX and more that his theoretical index has GASZ performing poorly in the 10 years before 2006?

Hope you enjoy Super Bowl weekend.

Steve

Hi Steve,

The 5 year backtest on GASZ gave a annualized return of 17%, so it’s performance so far is approx. in line with that. I have wondered if a rebound from the current free fall in gas prices will be a problem, but I have not checked. The biggest risk to me seems to be a structural shift in the term structure. This is probably why the older backtest you mentioned performed poorly.

At least we don’t need to worry about the futures activity due to GASZ moving the market…

— Vance

The share price for VQT is relatively high so 100 or 200 shares for a small spread is not as bad as it might seem. 100 shares is $12.5K, 200 shares is $25K. The 1000 shares example you give is $125K. Good rules though, just thought I would point that even 100 shares isn’t a bad chunk of change on this ETF (at least for me).

Hi Steve, I agree that for the 100/200 share blocks the normal spreads are usually very reasonable. Although, I do see distortions at opening especially that are pretty bad. The people that really need to get familiar with this are the brokers that are handling big retirement accounts, etc. They are used to Mutual funds. This is a whole new world for them.

— Vance