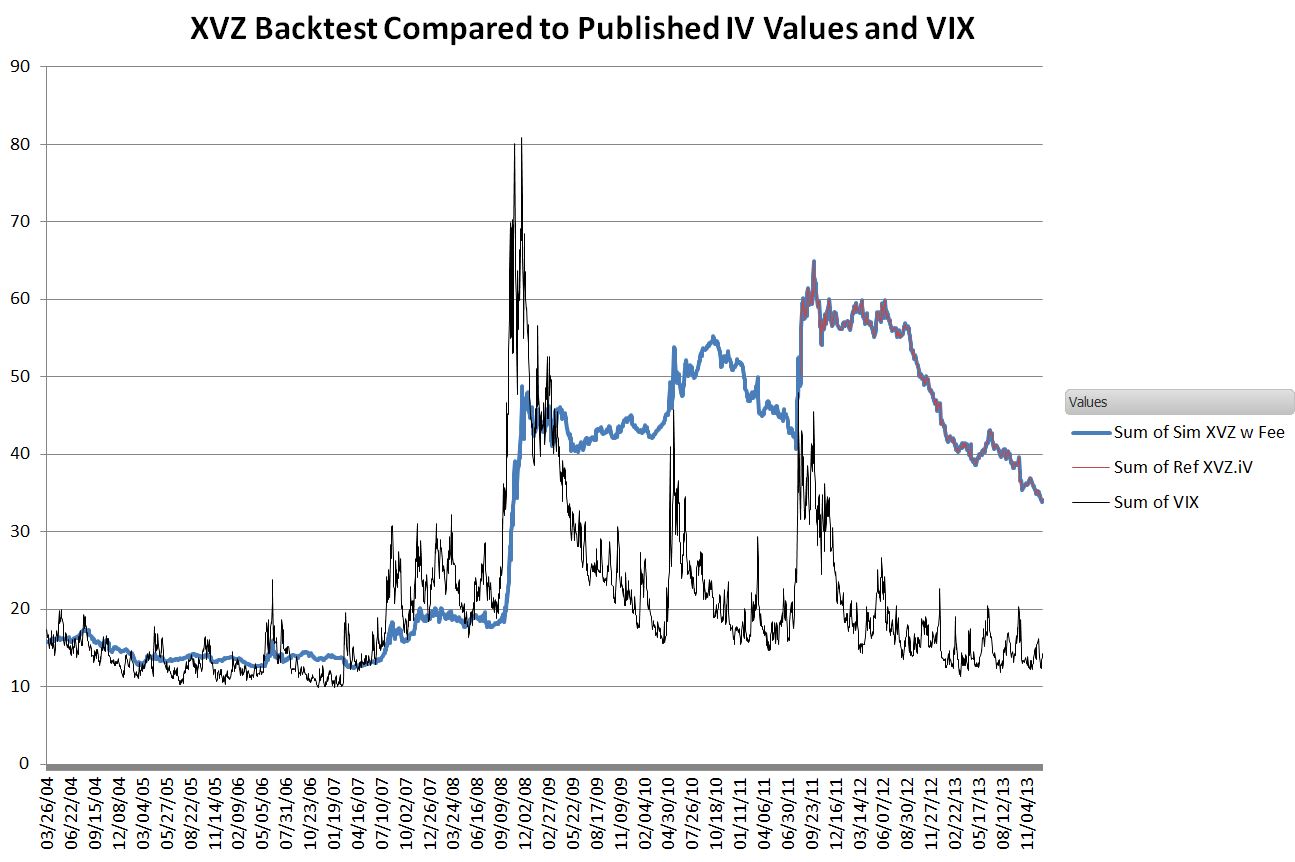

I have now backtested Barclays’ XVZ ETN back to when VIX volatility futures first started to trade in March 2004. I have made two versions of the spreadsheet available for purchase below. One with results data only and the other version with formulas and required indexes included. I have included the simulated daily closing values with and without the 0.95% annual fee from March 29, 2004 until January 2nd, 2013. The results of the simulated values compared to actual values are shown in the chart below. My results match the published SPDVIXTR underlying index within 0.001%.

>

XVZ appears to be a good way to hedge your portfolios during market corrections / crashes, unfortunately, it tends to decline during bull markets. For details on how to do this see:

For a detailed analysis of the inner workings of XVZ see Under the Hood of Barclays’ XVZ

For more information on the spreadsheet see this readme.

My thanks to Omar Qureshi for finding the defect in my spreadsheet that had blocked me for days.

If you purchase the spreadsheet you will be directed to paypal where you can pay via your paypal account or a credit card. Please email me at [email protected] if you have a problem, question, or request.

If you don’t see the purchase information below click on this link.

Hi, i find your research interesting. Before I buy your BT, my questions are: 1) how did you get historical data on VXV since 2004, as CBOE provides data since 12/4/2007? 2) does you spreadsheet have all the formulas for computing SDVIXTR fully disclosed?

Dias

Hi Dias, The VXV data was provided to me by another investor. The VXV data from March 2004 on is provided in the full spreadsheet. If you buy the full spreadsheet, not just the data you get the full formulas and indexes used in the computation. My version of the index that compares very closely to SDVIXTR is the column labeled $ Sim XVZ.

— Vance

Hi,

I was able to get historical VXV data back to 2002.

–Vance