All of the volatility based ETN/ETF products are relatively new. Barclays’ VXX and VXZ oldsters started in January 2009—just a few months before the end of the 2008/2009 crash. This lack of historical data over full market cycles makes it hard to assess the risks associated with new products—such as VelocityShares’ ZIV (medium-term inverse volatility) which started in November 2010. test

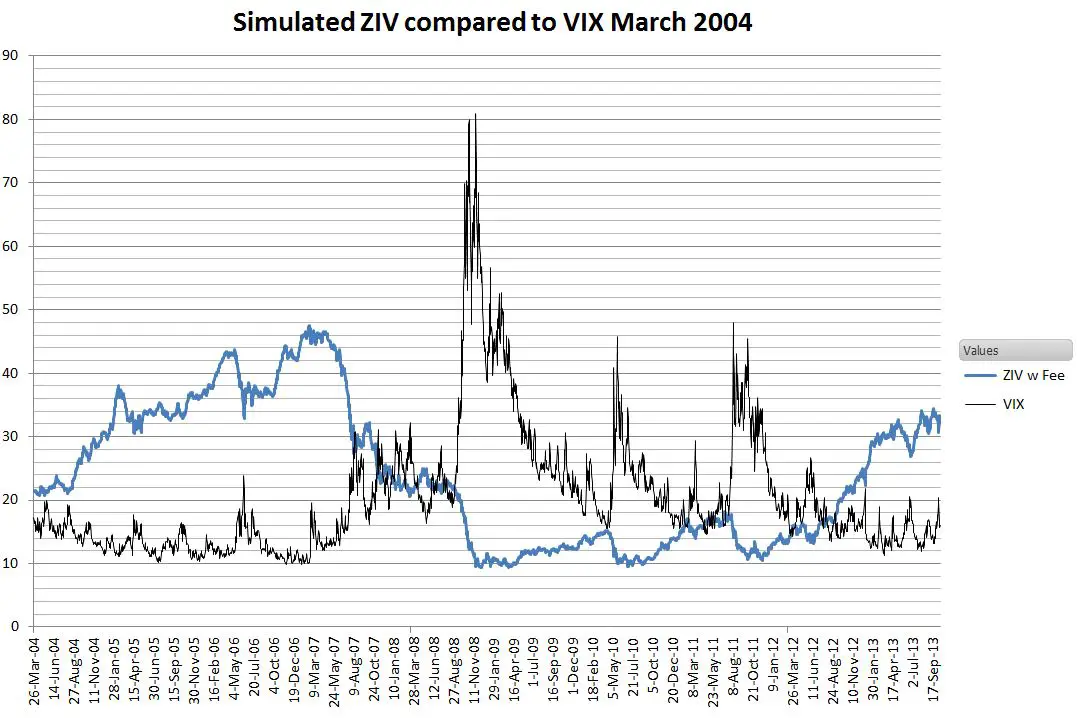

I have backtested ZIV starting from March 2004, including the impact of fees and treasury bill interest. The results for this presumably tamer inverse volatility ETN, are shown below.

I was surprised at how volatile, and how low this hypothetical ZIV went during the recent bear market—losing 80% of its value from 2007 to 2008. ZIV appears to be a bull market only instrument and not suitable for buy and hold. For one approach to timing investments in inverse volatility see Taming Inverse Volatility with a Simple Ratio.

If you are interested in obtaining the full simulation results for ZIV back to 2004 see Backtests For Popular Volatility ETPs.

Please, can you post the prices for ZIV going back to 2006?

Hi Giorgio, I sell ZIV simulated data back to 26-March-2004 for $20. Please contact me at [email protected] if you are interested.

Best Regards, Vance

What VIX futures months does ZIV track? Thanks – love your blog.

Hi Ragu,

ZIV is tied to the inverse of the 4/5/6/7 month futures. As the 4th month is rolled off the 7th month is picked up. The ticker for the index is SPVXMP:IND. For a full list of ETPs and associated futures months see

https://www.sixfigureinvesting.com/2010/12/volatility-tickers/.

— Vance

It is surprising indeed. I thought the value of ZIV comes from two contributors: the VIX futures price between 4 to 7 months and contango(80% of the time)/backwardation. Since VIX is mean-reverting, the effect of the former diminishes over time. From the chart, when VIX and SPVXMSTRcame back down to a previous levels, ZIV did not return to previous highs. Something else is eroding its value.

Hi Yuman,

The other factor might be path dependency. For example if VXZ went up 10% one day and then down 9% the next it would end up about where it started. ZIV on the other hand would end up 2% down. At some point I’ll try to analyze the data to see if that is the reason for this behavior.

— Vance

IMHO the backtest is flawed because VIX spiked in 2008 like it has never before. VIX hit 70+ in October of 2008, which I don’t think will repeat any time soon. It’ll probably take at least 15 years for VIX to head above 50. It does not happen that often. How about backtesting XIV starting from 2000 if that’s possible? The 2008 year was the worst year for the VIX and is therefore an anomaly. Vix has never spiked like that since its inception.

Hi John,

I agree that the backtest is probably flawed, but not for the reasons you describe. The VIX (or the CBOE’s backward projection) of the VIX has been over 40 five times in the last 15 years. On May 21, 2010 the intra-day VIX reached 48.2–pretty close to 50. The 1987 crash would have had VIX levels in the neighborhood of 120–so overall I don’t agree we can say that 2008 was a one-of sort of event. I think the increased interconnnectedness of the world’s financial systems are making panics more likely rather than less.

I do suspect that the 2008 crash seriously disturbed the term structure of the volatility futures–putting them into much stronger contango than they were before. I need to verify this, but I’m pretty sure that is the case. The next question is will this be a permanent change, or something that will fade away. My guess is that it will be persistent. An analogy is the volatility smile on option’s IVs that appeared after the 1987 crash and has never gone away.

If the high contango situation continues with the medium term futures, then I expect ZIV to perform significantly better than the backtest would suggest. But I’m going to be trying to protect myself against those pesky VIX spikes.

Unfortunately the volatility futures that these products are based on have only been trading since 2004, so backtesting earlier than that is not possible. Lack of history is going to be a problem for a while–especially if the underlying behaviours keep changing.

— Vance

Thanks! Not the results I would have expected. From the results here, There doesn’t appear to be any reason to buy zix.