One of the scariest things about market panics is their unpredictability. All of us remember the dark days of 2008 and 2009, not so many the October 1987 crash. For me, both of those crashes carried the same sense of disruption—the feeling that things would never be quite the same again.

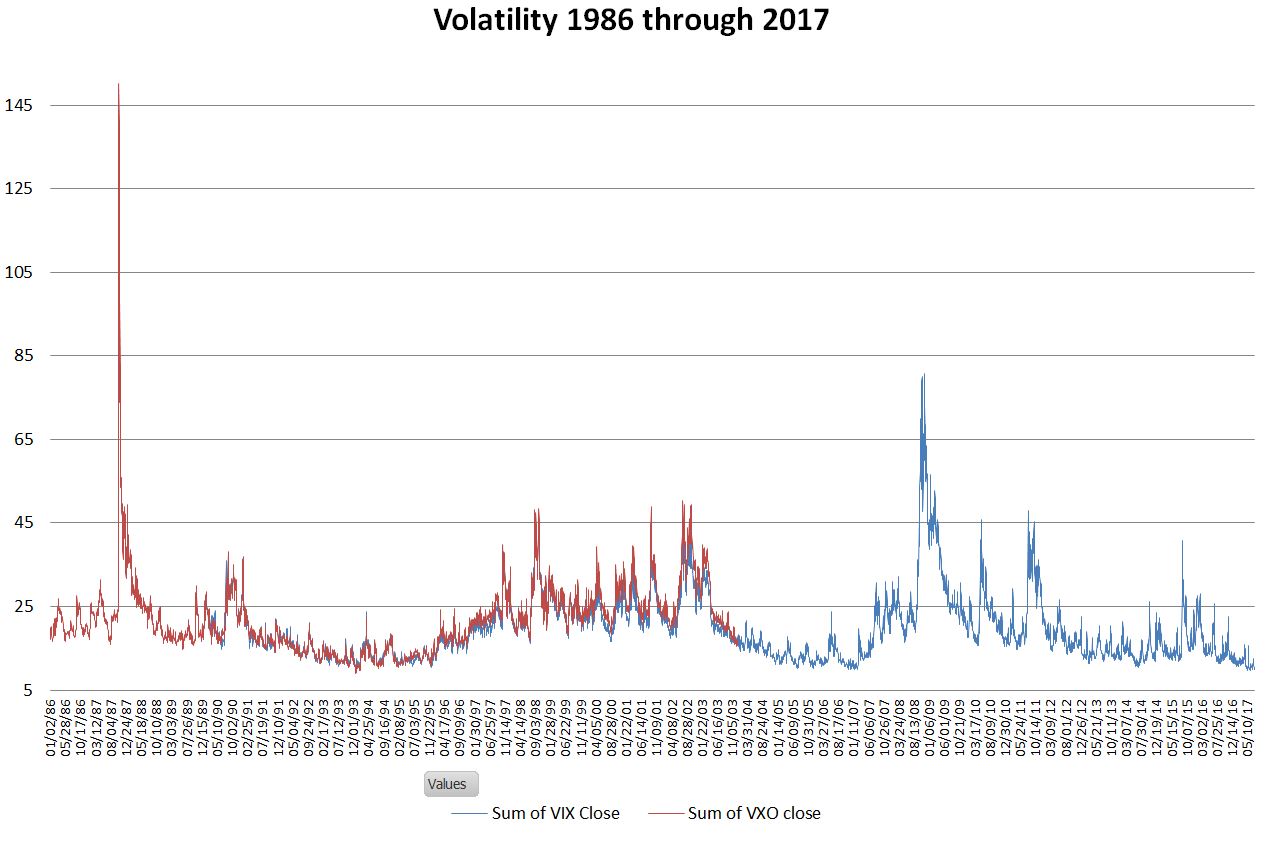

I’ve been looking at the history of volatility because it’s clear to me that volatility spikes are a big danger in the inverse volatility investing that I’m been doing. Shorting VXX, or being long SVXY is great while we are in a bull market, but things can get very ugly in a hurry. The chart below shows a history of volatility, starting in January 1986. Neither the VIX, or its predecessor VXO existed at that point, the original index started in 1993, but the CBOE has projected the old style VXO index back to that year.

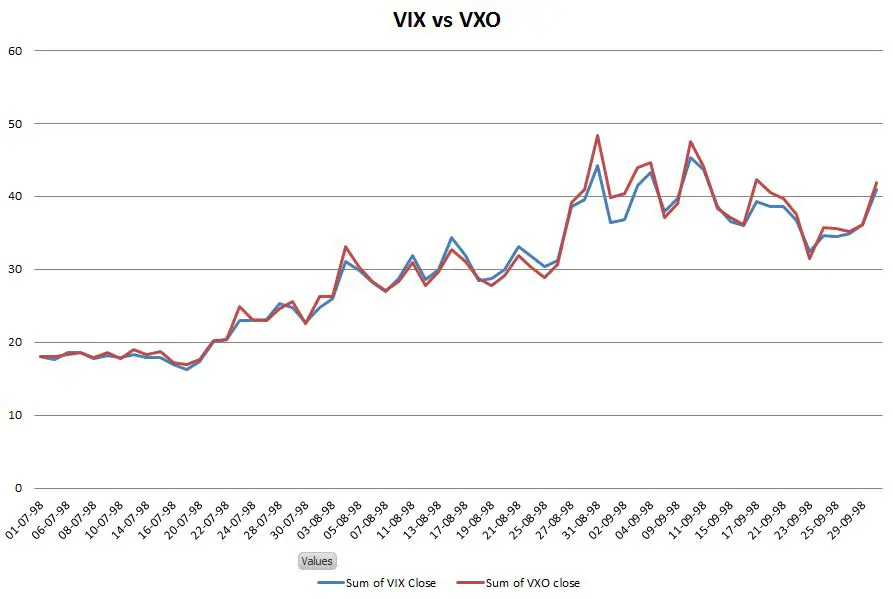

I’ve never looked closely at the original VIX index, which is now called the VXO. The VIX methodology we now use was put in place in 2003. The chart below shows the two indexes during a fear spike in the fall of 1998. The two track each other closely enough that for normal and semi-normal situations they look comparable.

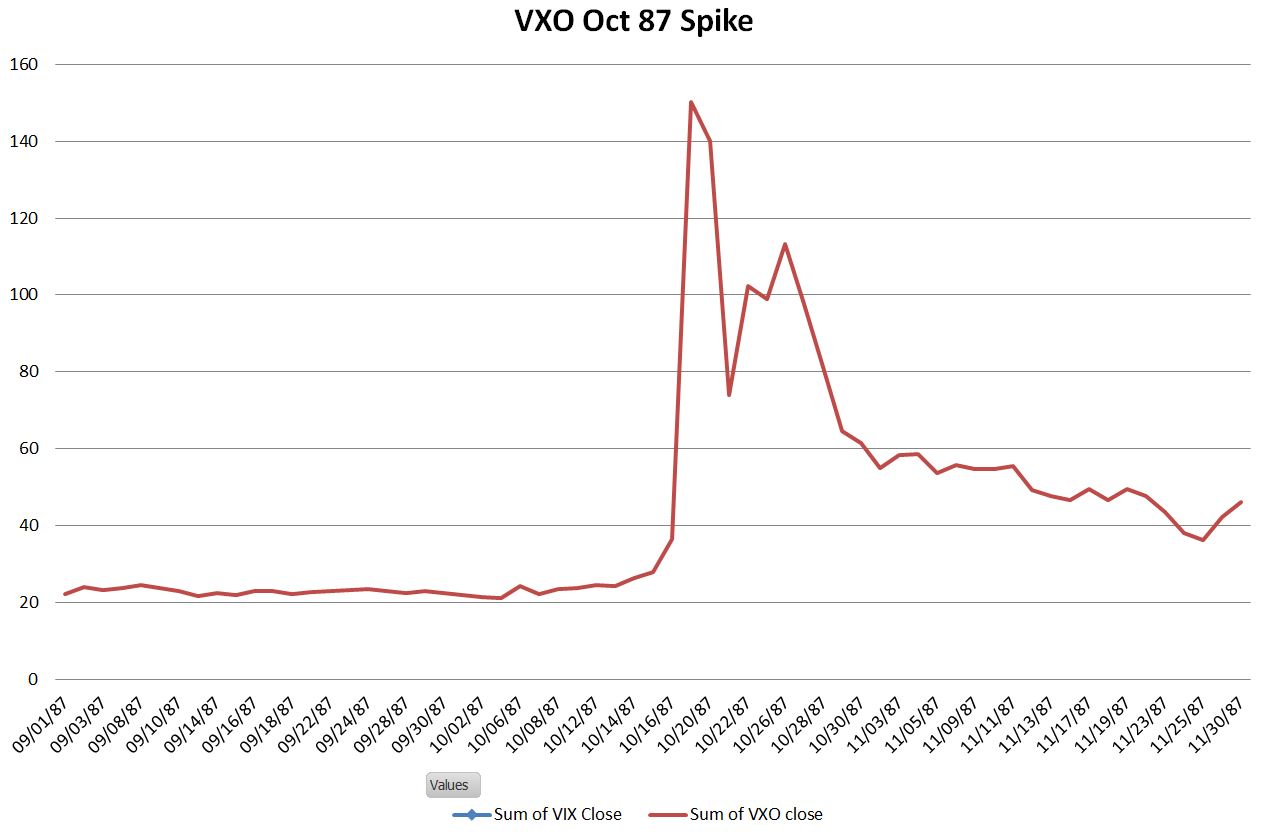

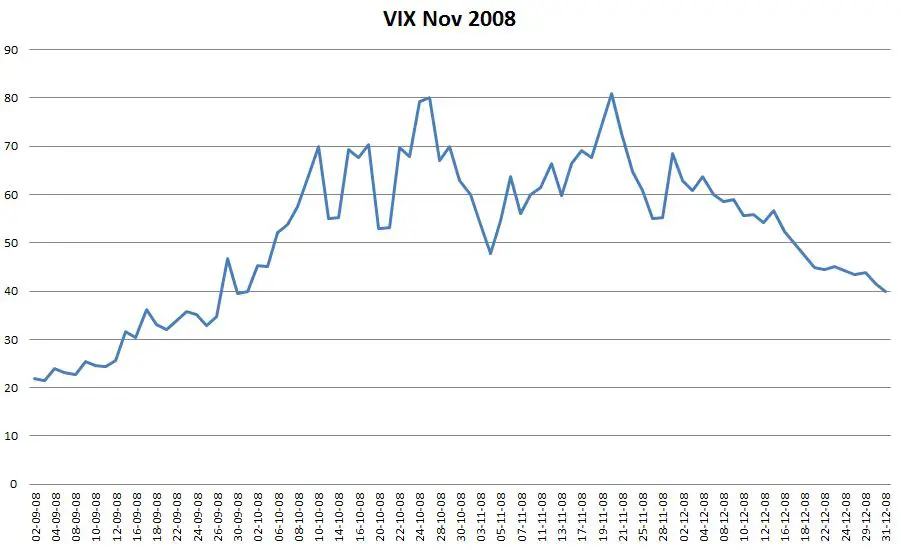

Below, I have zoomed in on the October 1987 and the November 2008 fear spikes.

Looking at these two monumental spikes, there doesn’t seem to be anything unusual about the run-up. Nothing in the data suggests that a massive spike in volatility is on the way.

For more information, and access to the raw data used see the CBOE’s microsite on VIX.

In the simplest of terms;

IF the VIX is at 25

THEN the “market” will carry a 25% chance of going Up by 25% the next 52-wk (1-year) once the VIX has a pivot

IF the VIX trading at 50 ( 75% ?)

THEN the market has 50% ( 75% ) chance of being 50% higher in 1-year

The Caveat is that the VIX can STAY at a Number for an indeterminate number of months before the Inflection Pivot.

I guess the trick is to always pay attention to the term structure. As far as I can tell, 2008 was in backwardation for quite some time (i.e. months), and one should’ve stayed on the sidelines during that time.

I agree. Until the backwardation lets up the market is pretty risky.

Caption should be VXO Oct 87 spike, not 86.

Fixed. Thanks!

Can you explain what xiv is

Hi,

XIV is an exchange traded product that is designed to go up when the market volatility goes down. You buy / sell it like a regular stock, except instead of betting on a company you are betting on volatility. Typically XIV will do very well in a bull market, but horribly when the market is down–because volatility spikes up during market corrections.

— Vance

Also note that spikes in the VIX decay exponentially. Now, try to trade it and let me know how that goes…

On my calculations one year ago I remember that XIV’s max drawdown would have been 80% over several weeks in 2008.

You can use options instead of spot. That will mitigate the risk bigtime, while keeping the returns more or less same, depending on the strategy used.

So it’s clear that an investment in XIV would have been zeroed out that day in 1987 and heavily damaged in 2008. But if this happens every 21 years, just be sure to cash out a buy-and-hold XIV position before 2029…