In spite of its name, XIV is not the inverse of the VIX index—it is the daily percentage inverse of an index called SPVXSP, which you can monitor on Bloomberg here. This index very closely tracks the same index that VXX uses, SPVXSTR.

Last week XIV did not track VXX’s daily moves particularly well. There has been a lot of speculation about what was causing this disruption—ranging from turmoil in the futures markets, XIV’s daily re-balancing, to the heavy backwardation in the soon-to-expire August volatility futures.

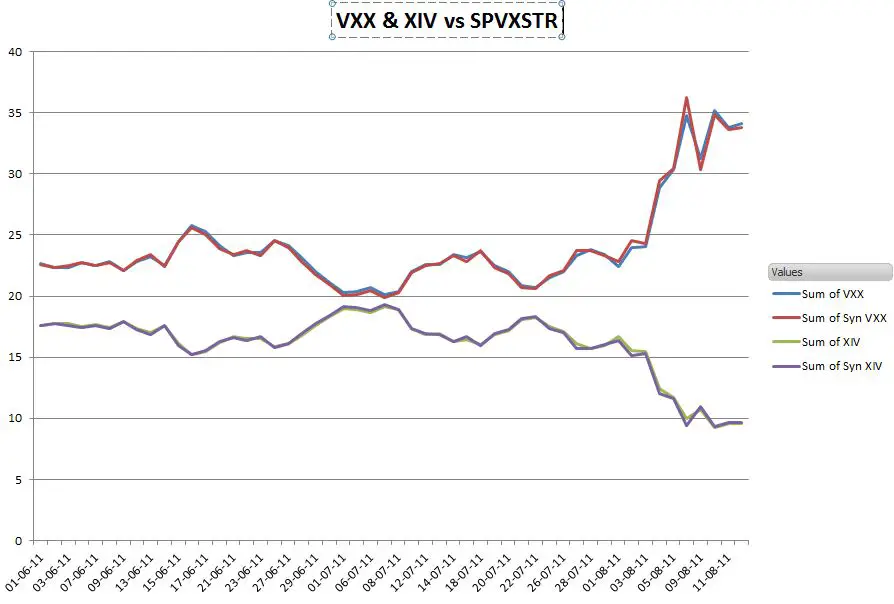

Below I have ploted VXX and XIV against the values they should have based on the index:

Things do not look seriously out of wack. Most importantly, we aren’t seeing a divergence between the index and the VXX/XIV prices. Daily errors are being compensated for over time. The next graph shows the daily VXX/XIV divergence from the index in percent. The interesting thing here is that VXX is having trouble tracking too—it’s just in the positive direction.

Looking at these graphs I’m inclined to say that the tracking problems are not specific to XIV, but rather due to the volatility/disruption of the futures market associated with the S&P downgrade.

Hi Vance I’m trying to understand how XIV etc. works. You can see on the velocity web page what position XIV has in the front and back month future (in USD terms). I’m still struggling to understand XIV’s performance on the back of that. With a short position of ~50/50 in 1st and 2nd month future and Mar and Apr future down 7.5 and 5.5% XIV was only up 4.5% the next day futures dropped only ~2% and it was up 3% ….

What am I missing? Thx. Marco.

Hi Marco, For XIV the allocations to front and back futures change on a daily basis. What specific days were you looking at? If you give me the dates I can tell you the allocations for those days, futures moves, and XIV’s corresponding moves.

— Vance

I know the allocation is 100% front month future on the day the old future expires and that is rolled daily into the back month future.

lets take 4th Mar

Mar future from 16.35 to 14.95 -8.5%

Apr future from 16.90 to 15.85 -6.2%

XIV from 19.81 to 20.79 +4.9%

I think the allocation on the 1st of Mar according to the web site (in USD amounts) was 51/49 (or the other way round?) but as both futures dropped more than XIV gained the allocation doesn’t really matter. Even if it was all in April why did XIV gain less than the April future fell? In one of the following days (5th?) it did gain more than the fall in either future, leaving me scratching my head,

Thanks!

M.

Hi Marco, The VIX futures market closes 15 minutes later than the NYSE, so the futures settlement values are not sync’d up with the typical close values you see for XIV and VXX–these are 4:00pm ET numbers. The VelocityShares XIV website shows a different Daily Indicative Value number than the regular market close. This is the number you should use for your calculations. Fidelity Active Trader Pro provides aftermarket IV values also. For XIV they give 19.51 for the 1-Mar-13 aftermarket and 20.97 for the 4-Mar-13 aftermarket — a percentage change of +7.5%, which matches the inverse of the SPVXSTR index change. The futures allocation mix at close 1-March-13 was 13/24th 1st month and 11/24ths 2nd month of the total index value.

Best Regards,

Vance

ah I thought the VIX future prices were also as of 4 p.m. ET. Makes more sense now. Thanks for your help

I have another question regarding XIV and VXX please. From my understanding XIV and VXX take the opposite position in VIX 1st and 2nd month futures. How comes that VXX is down ~25% over the last 3 month while XIV is only up ~13%. Seems if you can short VXX you can make more money on being short vol and contango this way than being long XIV or am I missing something?

thanks,

m.

Hi Marco, Daily rebalancing -1X funds like XIV have the same compounding errors as leveraged 2X and 3X funds. In choppy markets they will seriously underperform. For example if in two days VXX goes up 10% and then down 9.09% it will end up at the same price–XIV on the other hand will end up down 1.8% (e.g., 10 x 0.9 = 9, 9*1.0909=9.818). Shorting VXX does not have compounding errors but your leverage starts dropping if you are right and increases above one if you are wrong so you need to monitor your position very carefully. Also the best case gain for a short position is 100%, (stock goes to zero) so you would have to rebalance to do better than that.

thanks for your comments Vance. helping me understand the matter better. Much appreciated. m.

Hi Chris, I agree that these two funds use different indexes (they differ in whether Treasury bill interest is included) but I don’t agree that this explains XIV’s non-short tracking performance. Since Treasuries have effectively been yielding 0% for the last 1.5 years the difference is near zero (the drop in SPVXSP since 3-Jan-11 is -29.922% vs SPVXSTR of -29.9964%) it does not explain the difference in in short VXX vs XIV performance.

The difference is that XIV is a daily inverse percentage fund vs a true short (e.g., XXV, IVOP)–which introduces path sensitivities a true short position does not have. For example, a +10% day on VXX followed by a -9.09% percent day would leave VXX with no change, but XIV would end up down 1.8%.

–Vance

Vance,

Thanks for the reply. That’s a helpful explanation.

-Chris

What about the performance of XVIX?

Hi Steve,

You mean relative to its index–SPVXTSER (Bloomberg SPVXTSER:IND)?

— Vance

Thank you for the analysis, it eases my worries about XIV :).