It’s clear that the volatility ETN/ETFs have begun to dominate the VIX Futures market. What isn’t clear is whether it matters. Volatility isn’t a commodity like gold or corn that is physically limited, so future position limits don’t seem applicable. When the price of VIX futures is attractive, more can be created—and appropriate hedges put in place. But are these hedges distorting the overall market?

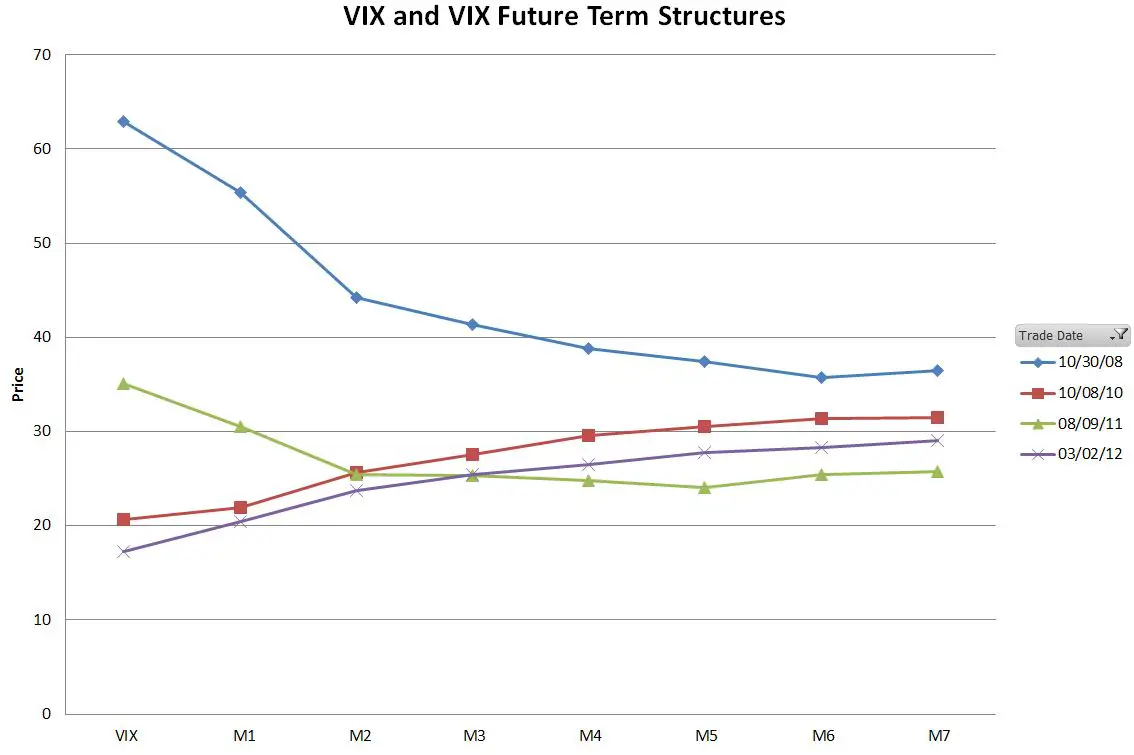

Some people have pointed at the current state of the VIX futures’ term structure relative to the VIX as evidence of market distortion. The long-dated futures (e.g., 7 months out) have recently been over 11 points higher than the VIX index. Although they ultimately expire close to the VIX index (VRO settlement), VIX futures tend to have a mind of their own. When the market is not panicky VIX Futures are normally priced higher than the VIX index, and the longer the term of the futures (expiration date further out), the higher the premium. Think of it as insurance, the longer the term of the insurance, the more expensive it will be. The chart below shows the VIX index price at the far left, with the VIX futures prices for months 1 through 7 shown left to right for several dates—two times of high fear (2008 crash, August 2011), and two times when the VIX has been low compared to the futures (November 2010, and March 2, 2012)

The recent term structure doesn’t appear to be totally out of whack with the comparable period in November 2010.

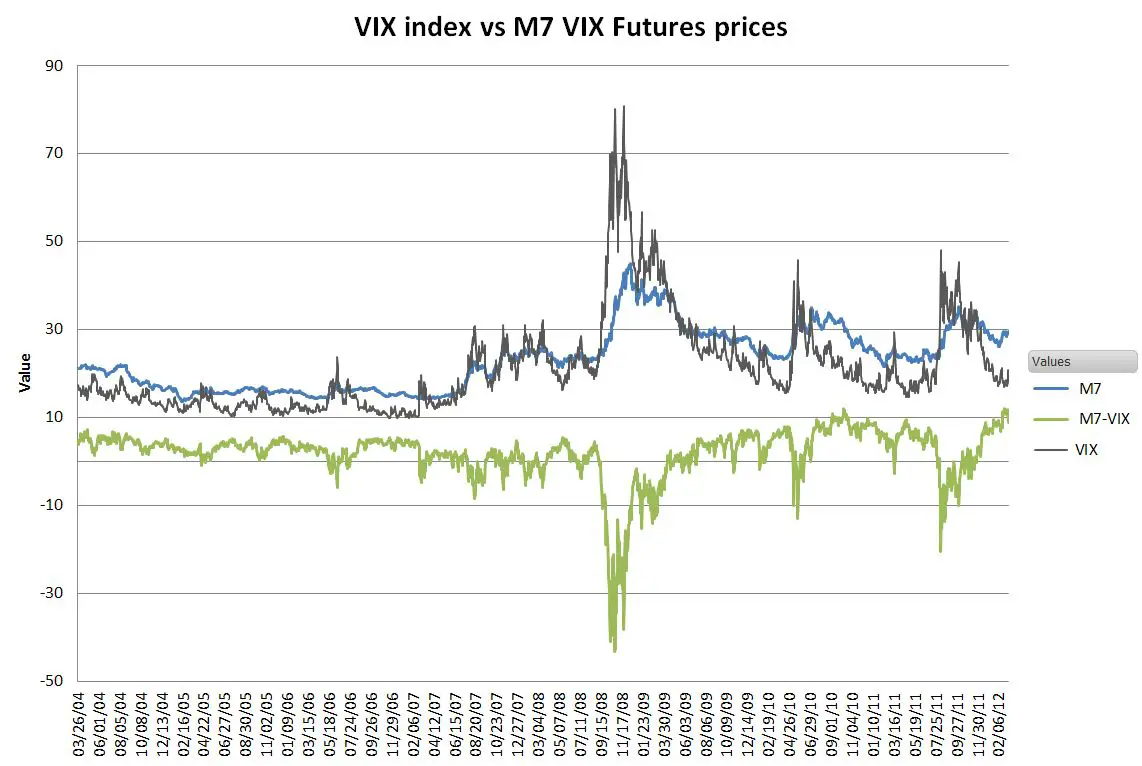

The chart below shows the relationship between the VIX index and the 7th-month VIX future (M7), with the green M7-VIX line showing the difference between the two.

Compared to the 40 point negative difference in 2008 the current VIX vs M7 relationship looks pretty pedestrian.

The other, much noisier discussion has been on the volume impact of the volatility ETN/ETFs on the VIX futures market. The assets that the funds hold are growing rapidly and their required daily activities in the VIX futures markets are 90% plus of the market. Specific concerns:

- Is it a problem that Volatility ETN/ETFs now do most of the trading on the VIX Futures Market?

- Volatility ETN/ETFs have known trading patterns. Their prices are based on daily future rolls (selling nearer months and buying further out months) in order to preserve a constant time maturity. Can this knowledge be exploited to game the market against the ETN/ETF providers?

- Will the overall growth of the VIX futures market cause problems?

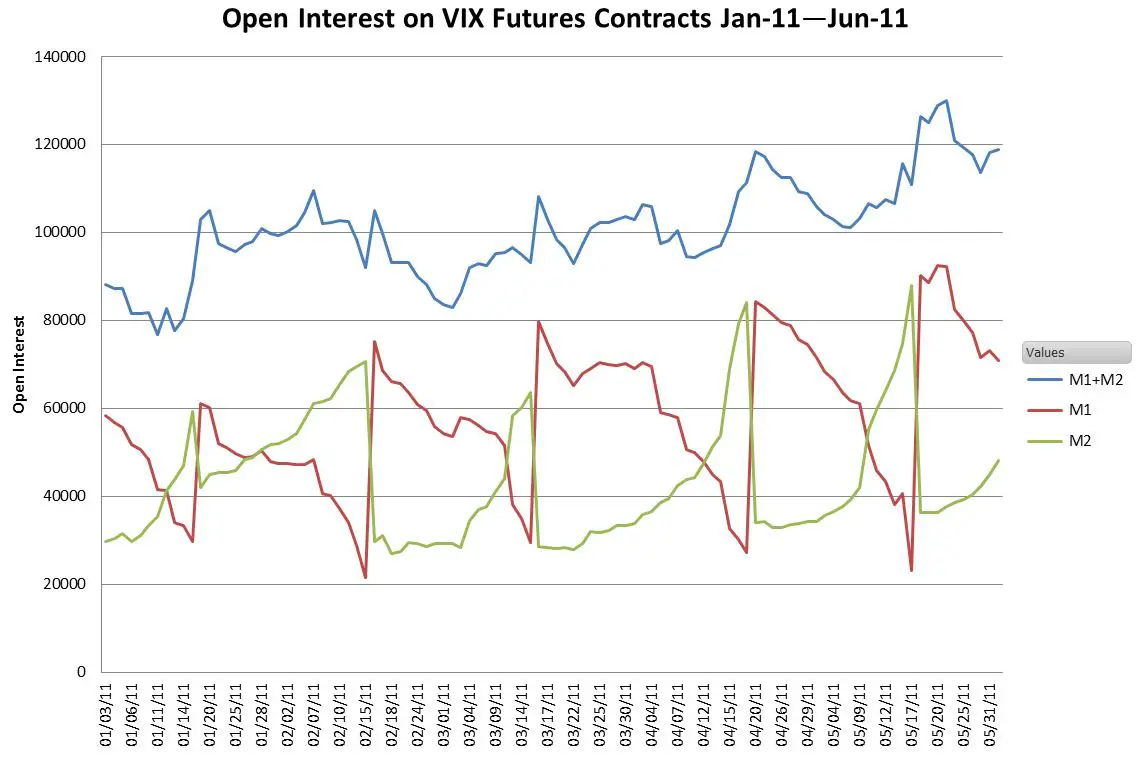

Barclays’ introduced the first Volatility ETNs, the short term VXX and the medium term VXZ in January 2009. This next chart shows short term VIX futures open interest in the era of the volatility ETN.

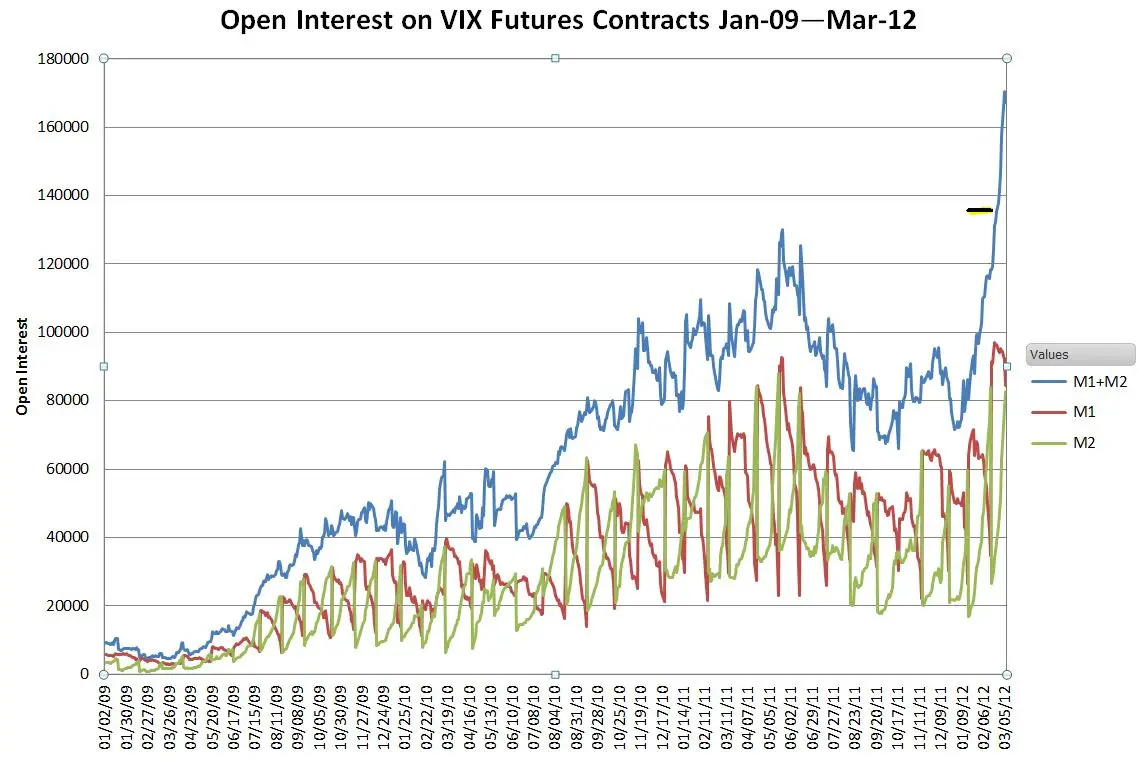

Things have heated up a bit in 2012…

Credit Suisse’s halt to TVIX share creation on February 22nd, 2012 (horizontal black bar on chart), doesn’t seem to have slowed things up. The CBOE’s March 6th announcement that they have reached a record open interest of 280,000 VIX futures contracts (including all their volatility futures) is not surprising.

Clearly, the volatility ETN/ETFs (see Volatility Tickers for the full list) are on a huge growth spurt. Their volumes now dominate the VIX futures market—but so what? It wouldn’t be the first time broad retail acceptance of a product overtook the institutional/commercial market (e.g, computers). Yes, they have a characteristic monthly pattern, but the term structure doesn’t show any sign of that demand distorting the prices—I would expect a bump in the M2 prices if that was the case.

Credit Suisse at least is feeling the growing pains, but so far Barclays and ProShares (the other rapidly growing fund provider) aren’t complaining.

I don’t see any evidence that SPX options are behaving strangely. I understand that shifting $50 million or more a day to rebalance an ETN with a billion dollars in assets is not a trifling thing, but compared to the $10 trillion market cap of the S&P 500 this feels like a tempest in a teapot.

Hi, can you check out the new product vvix of cboe? vis of the vix?

sounds very interesting…

Hi Do, I saw the announcement too. For now it is an index, but if they start offering futures on it, then things could get interesting. I will take a close look on this in a week or two.

— Vance

hi Vance

Does XVZ have a termination point?

Hi Hendra, XVZ does not appear to have a termination value like XIV or IVOP. There is not much that can drive it down, other than contango, which it is not too sensitive to. If Barclays goes bankrupt there is a process to value / close out the fund, but that is all I found.

— Vance

so,let’s say I buy some XVZ shares and Barclays goes bankrupt.

it means that I will lose that money on XVZ? Or is there any procedure so I can sold my XVZ?

Hi Hendra, Yes, if an ETN issuer goes bankrupt your shares would become worthless. Until close to the time of bankruptcy you should be able to sell your shares at the NAV (reference price). Lehman Brothers had several ETNs before they went bankrupt. My understanding is that those traded fairly until just a few days before the bankruptcy. You can check the health of a bank by checking its CDS rate–effectively the rate of insurance for insuring against the bankruptcy of t that bank. The higher the CDS cost, the riskier the bank. You can get the quotes from this post: http://www.distressedvolatility.com/2010/07/nice-to-see-cds-quotes-credit-default.html

— Vance

I think the problem with the VIX ETNs/ETFs being such a large share of the VIX futures market is what happens when volatility spikes. This was best described by the paper from Deutsche Bank that was eventually removed from Volatility Futures and Options, but boils down to the argument that hedge positions on these products drive up vol-of-vol and SPX skew, since after a big movement in either direction, they have to buy or sell a ton of vega.

The worry is that after a big move, it may be difficult to move that much vega at a reasonable price or without distorting the market.

Hi Tim, I did see the DB paper, in fact I have the pdf if you would like a copy. To me the key issue is the depth / resiliency of the VIX Futures market. So far in 2012 it has supported explosive grown in open interest (30% higher than previous highs, 140% higher than the beginning of 2012) without any significant distortion. .

Without detailed knowledge of VIX Futures market making processes it is hard to say when things will get strained, but the SPX options volatility pond is pretty deep. I suspect any price distortions would get arb’d out very quickly.

I know that historically front month VIX futures go into heavy backwardation during volatility spikes–perhaps a larger VIX futures market would damp out some of that behavior…

— Vance

It would be great if you could send me this DB Paper.

Thank you and regards

Ulrich

Yes, please share the DB paper.

o PLEASE keep the fish trading these products!!! i will trade the Futures and short them net = lets NOt allow other to tap lasss and scare away the fish!

Excellent post! Thanks!

I woul very much like to get this DB Paper.

Best regards

Ulrich