How does VXX trade?

- For the most part, VXX trades like a stock. It can be bought, sold, or sold short anytime the market is open, including pre-market and after-market time periods. With an average daily volume of 30 million shares, its liquidity is excellent and the bid/ask spreads are a penny.

- It has a very active set of options available, with five weeks’ worth of Weeklys and close-to-the-money strikes every 0.5 points.

- Like a stock, VXX’s shares can be split or reverse split— 4:1 reverse-splits are the norm and can occur once VXX closes below $25. For more on historic VXX reverse splits see this post.

- VXX can be traded in most IRAs / Roth IRAs, although your broker will likely require you to electronically sign a waiver that documents the various risks with this security. Shorting of any security is not allowed in an IRA.

How is VXX’s value established?

- Unlike stocks, owning VXX does not give you a share of a corporation. There are no sales, no quarterly reports, no profit/loss, no PE ratio, and no prospect of ever getting dividends. Forget about doing fundamental style analysis on VXX.

- The value of VXX is set by the market, but it’s closely tied to the current value of an index (SPVXSTR: S&P VIX Short-Term Futurestm) that manages a hypothetical portfolio of the two nearest-to-expiration VIX futures contracts. Every day the SPVXSTR index specifies a new mix of VIX futures in that portfolio. For more information on how the index itself works see this post or the VXX prospectus.

- Around 85% of the time the 2nd month VIX future is priced higher than the front month future. This configuration is called contango in futures’ parlance and is usually associated with a drop in VXX’s value. However, contango does not in itself cause VXX’s decline. Some people incorrectly believe that VXX’s end of trading day rebalancing, where sooner to expire VIX futures are sold and longer term VIX futures bought, results in losses when the term structure is in contango. But VXX’s daily roll of futures from the next to expire month the to 2nd month does not change its value, it is equivalent to making change, trading two nickels for a dime.

- VXX’s value is established by the value of the VIX futures it holds. Normally when the VIX future’s term structure is in contango both the VIX futures will be trending down, and VXX’s value will drop but in some situations, typically associated with upcoming uncertainties like elections, the two front-month futures can be steady or increasing in value even when the 2nd month future is priced higher than the 1st month. VXX rising in value while the term structure was in contango occurred in late August 2020. For more on contango and its impact on VXX’s value see “The Cost of Contango, It’s Not the Daily Roll.”

- The SPVXSTR index is maintained by the S&P Dow Jones Indices and the theoretical value of VXX if it were perfectly tracking the index is published every 15 seconds as the “intraday indicative” (IV) value. Yahoo Finance publishes this quote using the ^VXX ticker.

- Wholesalers called “Authorized Participants” (APs) will at times intervene in the market if the trading value of VXX diverges too much from the IV value. If VXX is trading enough below the index they start buying large blocks of VXX—which tends to drive the price up, and if it’s trading above they will short VXX. The APs have an agreement with Barclays that allows them to do these restorative maneuvers at a profit, so they are highly motivated to keep VXX’s tracking in good shape.

What does VXX track?

- Ideally, VXX would track the CBOE’s VIX® index—the market’s de facto volatility indicator. However, since there are no investments available that directly track the VIX Barclays chose to track the next best choice: VIX futures.

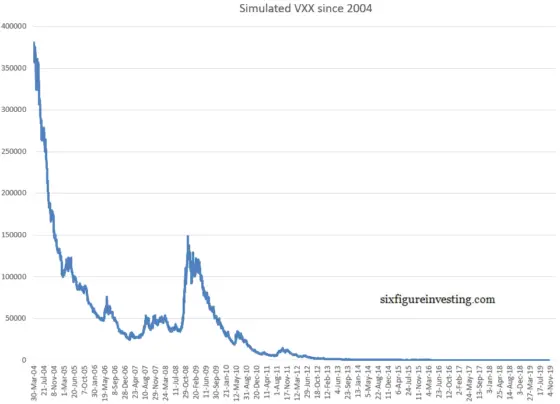

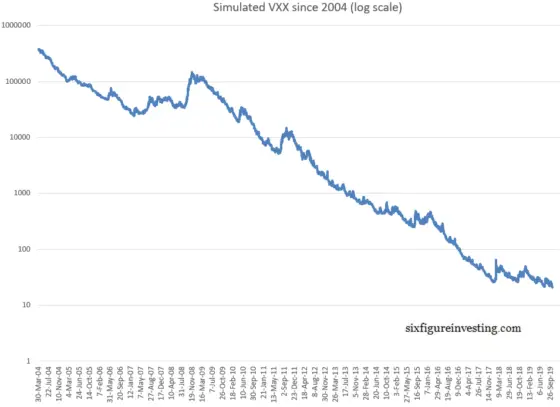

- Unfortunately using VIX futures introduces a host of problems. The worst is horrific value decay over time. Most days both sets of VIX futures that VXX tracks drift lower relative to the VIX—dragging down VXX’s value at the average rate of 4% per month (30% per year). This drag is called roll or contango loss.

- Another problem is that the combination of VIX futures that VXX tracks does not follow the VIX index particularly well. On average VXX moves only 45% as much as the VIX index.

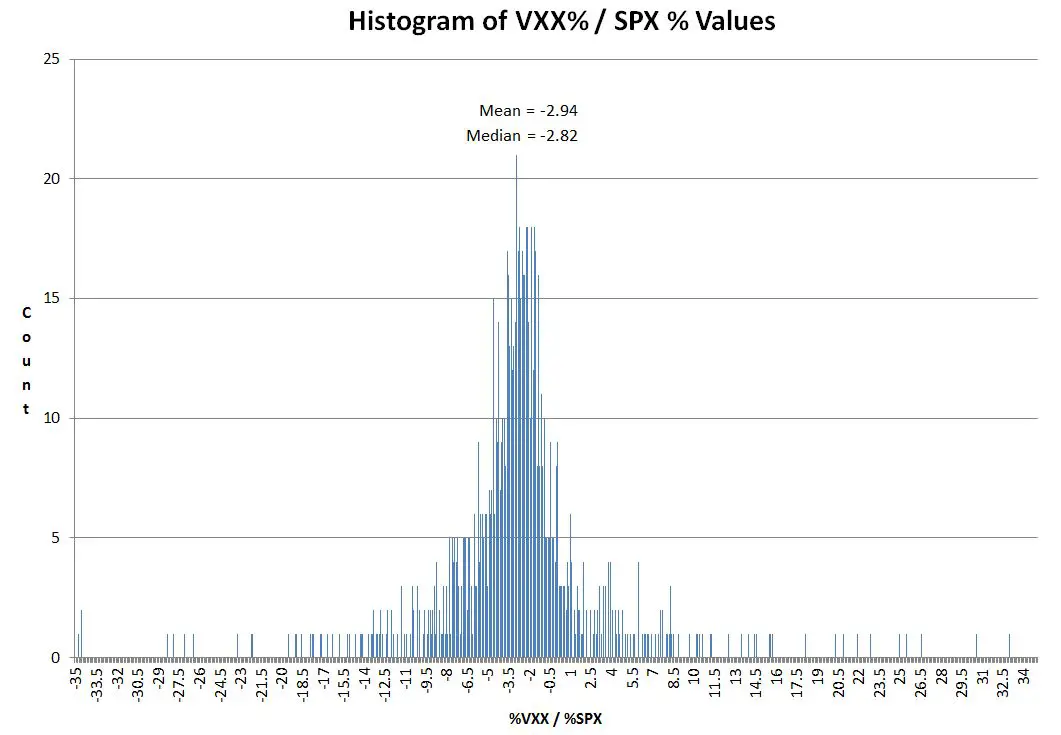

- Most people invest in VXX as a contrarian investment, expecting it to go up when the equities market goes down. It does a respectable job with the VXX averaging percentage moves -2.94 times the S&P 500, but 16% of the time VXX has moved in the same direction as the S&P 500. The distribution is shown below:

- With lethargic tracking to the VIX, erratic tracking with the S&P 500, and heavy price erosion over time, owning VXX is usually a poor investment. Unless your timing is especially good you will lose money. For a backtest of VXX starting in 2004, see this post.

How does Barclays make money on VXX?

- Barclays collects a daily investor fee on VXX’s assets—on an annualized basis it adds up to 0.89% per year. With current assets at $230 million, this fee is enough to cover Barclays’ costs and be profitable. But even if it was all profit it would be a tiny 0.1% percent of Barclays’ overall net income— which was $1.8 billion in 2018.

- From a public relations standpoint, VXX is a disaster. It’s frequently vilified by industry analysts and resides on multiple Worst ETF Ever lists. You’d think Barclays would terminate a headache like this or let it fade away, but they haven’t done that even though 5 reverse splits—which suggests that Barclays is making more than $10 million a year with the fund.

- Unlike an Exchange Traded Fund (ETF), VXX’s Exchange Traded Note structure does not require Barclays to specify what they are doing with the cash it receives for creating shares. The note is carried as senior debt on Barclays’ balance sheet but they don’t pay out any interest on this debt. Instead, they promise to redeem shares that the APs return to them based on the value of VXX’s index—an index that’s headed for zero.

- If Barclays wanted to fully hedge their liabilities they could hold VIX futures in the amounts specified by the index, but they almost certainly don’t because there are cheaper ways (e.g., Over the Counter Swaps) to accomplish that hedge. In fact, it seems possible that Barclays might assume some risk and not fully hedge their VXX position. According to ETF.com’s ETF Fund Flows tool, VXX’s net inflows were at least $5.99 billion since its inception in 2009. At least $4.8 billion dollars of that asset value was lost by investors and an equivalent amount by Barclays if they were hedged at 100%. If they were hedged at say 90% they would have cleared a cool $480 million over the last 4 years in addition to their investor fees. Barclay’s affection for VXX might be understandable after all.

VXX’s 2022 share creation crises

On 14-Mar-2022, Barclays suspended share creations of VXX due to an administrative screw-up. During the suspension, VXX traded at premiums as high as 52% over its IV price. This premium over the IV price can develop because share creations are a key process required for doing the arbitrage operations that keep Exchange Traded Products trading close to their tracking indexes. For more on these processes see Why Arbitrage is Essential For Exchange Traded Products. The IV price tracks an index, SPVXSTR that is computed based on the settlement prices of VIX futures rather than the assets that Barclays holds. When VXX’s share creations resumed on 26 September 2022, its tracking to the IV prices went back to the typical +-1% range.

Important Dates

- Original VXX Inception 30-January-2009

- VXXB Inception 25-January-2018 Hello VXXB, Goodby VXX

- Original VXX termination 30-January-2019

- Renaming of VXXB to VXX 2-May-2019 Goodby VXXB, We Hardly Knew Ye

- VXX reverse splits: See this post

VXX is a dangerous chimeric creature; it’s structured like a bond, trades like a stock, follows VIX futures, and decays like an option. Handle with care.

Purchase simulation of VXX 2004—20123

Updated Oct 11, 2023

For more information:

Hi Vance,

For selling a volatility option short, would you recommend the VIX or VXX options?

I have found that many more contracts of the VIX options seem to be traded (for some months), perhaps making for greater liquidity and better fills (although the bid/offer spreads still don’t seem to be that tight). Also, with the European-style VIX options, one is protected against early assignment. With no dividend on the VXX, early assignment on an option seems unlikely, but an unexpected assignment on a short call can be costly – Etrade currently charges a 2% fee on a short position (if they can even find stock to borrow).

Thanks for your helpful articles!

HI Davy,

I think the market does a good job making choices like this mostly a coin toss. I agree early assignment on VXX options is a pretty low risk. VIX options have variable sensitivity to the VIX depending on how many days they have to expiration in addition to the normal options delta changes. On any option trade I recommend starting with mid-price limit orders between bid and ask to start with. Often you can get fills around that price.

Just a silly question, do Authorized Participants intervene during pre-market and after-hours when pricing deviates from the indicative value? My trading style would be placing market orders overnight, so if they aren’t intervening pre-market then my pricing can get jacked up whenever I trade.

Vance,

Sorry for all the words. It would have been clearer to ask:

If no one is buying or selling the VIX futures, but a lot of people start buying VXX, would the price of VXX go up?

If so, would that be because of the demand for VXX, or another reason?

VXX won’t go up because Authorized Participants start shorting VXX in that scenario. Think of this like the SPY ticker that tracks S&P 500. The buy demands cannot derail SPY from tracking S&P 500 and vice versa.

Hi ALP, There are two issues here, one is how well does VXX track the front month VIX futures and the other is a liquidity issue–if someone bought billions of dollars of VXX what would happen.

Regarding tracking–as commented by John in his comment in a normally functioning market the APs keep the price of VIX futures / VXX closely linked. If the calculated values differ by much, a percent or two then they do coordinated buy/selling operations that lock in risk free profits.

At some point extra-ordinary amounts of VXX buying would influence the VIX futures market too. If the buying pressure on VXX was heavy, the APs would be shorting VXX as it diverged from it’s IV price calculated by the underlying VIX futures and buying VIX futures to hedge their shorts. The VIX future market is like any market, if there is an unusual amount of buying it will tend to drive its prices up. WIth heavy demand VIX market makers would be raising their prices and hedging their positions with VIX futures of other months, VIX options, and SPX options–which would impact their prices. If there was nothing else going on other than this extra-ordinary amount of VXX buying this constellation of hedging choices associated with VIX futures would blunt the impact of the buying on the VIX futures prices. The wagging tail might move a the dog a bit, but not much.

I’d be curious to learn what happens when everyone shorts VXX. APs would buy VXX shares then sell VIX futures; will Contango eventually go away as a result? Shorting VIX ETFs is getting widespread attention these days and people are making money, and I find it hard to believe that there is no downside to this trading strategy.

Hi John, Despite all the press if you look at the actual ETP assets under management they are relatively balanced between the short and long funds.

Heavy shorting of shorter term futures tends to increase contango because the associated selling depresses their prices.

The downside is simple–volatility spikes can do huge damage to short volatility positions. People are routinely blown out of their positions if they aren’t equipped emotionally / with enough margin to survive volatility spikes.

“Heavy shorting of shorter term futures tends to increase contango because the associated selling depresses their prices.”

That’s actually making this trade even sweeter then 🙂

On volatility spikes – I’ve analyzed past VXX data and iirc the biggest overnight gap-up was around 10% (I’m on a business trip so I don’t have the data, but easily verifiable via yahoo finance). While 10% isn’t small, it’s not that big either. And intraday run-ups can easily be mitigated by stop-loss orders. Tbh I don’t find volatility spikes that concerning, personally.

If one keeps on shorting volatility during financial meltdown like 2009…well, they have themselves to blame. But we all have plenty of time to get out before that.

Vance,

How does buying and selling VXX affect the price of VXX, – a little, a lot, or not at all?

Since VXX is calculated from the two nearest month’s VIX futures contracts, that might mean that buying and selling VXX has no effect on the price of VXX – only trading in the VIX futures.

Since VXX is an ETN, I would expect that buying and selling VXX might result in buying and selling these two VIX futures contracts involved in calculating the price of VXX.

But your article “How Does VXX Work?” says:

“If Barclays wanted to fully hedge their liabilities they could hold VIX futures in the amounts specified by the index, but they almost certainly don’t because there are cheaper ways (e.g., swaps) to accomplish that hedge.”

That implies that my buying or selling VXX does not necessarily cause Barclay’s to buy/sell the VIX futures on which the price of VXX is based.

So, when the price of VXX starts running up, that is not necessarily because there are a lot of people buying VXX. It can be due to reasons that have nothing to do with the trading demand for VXX. Right? What are those reasons?

Can you enlighten me?

Thanks,

Alp

One thing I don’t understand is this. The “Authorized Participants” intervene in the market to make sure VXX stays reasonably close with ^VXX-IV. For VXX, most of the traders are short-selling, which means the APs are buying and end up with a huge unrealized loss.

Is anything going to happen to their long position? It doesn’t look like APs or Barclays are going under because of this, but in which case who’s losing the money as shorts make money?

The authorized participant (AP) involvement is very low risk for them. In the case you mention, where there is a lot of shorting, then the trading price will tend to drift lower than the IV price. In that case the APs will buy the underpriced VXX shares and hedge their position at the time by shorting the appropriate VIX futures positions. This locks in their profit. They close out their positions end of day by presenting the VXX shares they have for redemption. The ETN issuer (Barclays in this case) gives them cash in exchange for the VXX shares at the end of day IV price. The APs close out their VIX futures positions at the same time, so the transaction is netted out with a profit.

If VXX is trading higher than the IV then the APs short VXX and take long positions in VIX futures to hedge their positions.

For Exchange Traded Funds (e.g, VIXY) , the issuers internally hold the actual shares of the underlying index (VIX futures in this case) so when the shares are redeemed they deliver the actual futures instead of cash. The APs use those directly to close out their VIX futures short positions.

Vance,

Thank you very much for your quick yet elaborate response! Makes a lot of sense now.

hi Vance,

Is this ETN considered an IPU (index participation unit) and can a mutual fund invest in it?

Hi M, I don’t think VXX is an IPU. It follows an index, but it’s not a passive trust, the issuers are actively creating / redeeming shares. I don’t see any reason why a mutual fund couldn’t invest in VXX, it’s an active, listed security.

hi Vance, a mutual fund can only invest in an ETF if it’s considered an IPU. If it follows a widely quoted market index in the US or Canada then it’s considered an IPU. But i dont think the index it follows is considered a widely quoted market index. i tend to agree with your explanation though it doesn’t follow the index passively, but by way of derivatives? does it use leverage?

Hi M, VXX follows SPVXSTR which seems to me to be is a widely quoted index, As described in the article VXX’s market value is kept close to the index value via the arbitrage actions of the authorized participants.

How does this instrument still exist except for traders? Seems to me that shorting this thing over the long term is money in the bank. Granted it could explode against you very quickly, but even taking a ’08 type vix spike into account (such a scenario would send VXX to $150 from a $38 level today or x4 in a few days) but If you can muster the margin requirement (cash) to cover the short position loss, you could make 50% a year? Certainly not for the faint of heart. I’ve always heard shorting vol is like picking pennies up in front of a bulldozer, but wouldn’t mind hearing your thoughts.

Hi Joe, For starters you should check out this post: https://www.sixfigureinvesting.com/2016/10/is-shorting-uvxy-tvix-vxx-the-perfect-trade/

Thanks for this and many others interesting posts! Only a question, I see that on investing.com the name is “iPath S&P 500 VIX Short-Term Futures Exp 30 Jan 2019 (VXX)”… The expiration date “30 Jan 2019” what does it mean? Thanks in advance!

Hi Giulio, I called Barclays regarding this. The person I talked to said that they can’t just extend the date on VXX, so they will very likely create another ETN like VXX that has a farther out expiration date. I suspect they will figure out how to move the VXX ticker over to this new fund, but that might be an open issue.

Vance

I wish I have seen this article before I took my position at the pre-split price.

Currently own 40 VXX 1/2018 Strike 60. Now they are called VXX1 (ask .40 Bid 0)

I can’t even sell them. My lost is $3,000

what an expensive lesson it was. Barclys your a scam business.

Hi Scott, At the risk of offending you, do you know that you can put in a limit order between the bid/ask price? The current bid/offer is 0/.45. My rule of thumb is that normally you can usually get a limit sell order fill at midprice between the bid ask, or a nickel less in the market makers’s favor. In this case I would start with .25, let it sit for 10 minutes, drop it to .20, sit for 10 minutes, drop to .15, Normally I would be surprised if it didn’t fill at at least .15, but it could be that these adjusted strike series are just horribly liquid. I would be surprised if you couldn’t get some sort of fill above zero.

Hi Vance, no offense taken. I am thinking to hold on in case of a major event that might spike the vxx much higher. I don’t know I am just at a lost on best course of action.

Yeah, me too. so what? Just hold it or sell? Could it really go to zero?

I’m a bit late to the conversation, Scott, but I would say holding and hoping for a gigantic spike is just smoking the hopium. Even if there were a spike like 2008, you would never get back to your cost basis. You learned a lesson, an expensive one. We’ve all been there. Your best way to play VXX is to just short a small position and hold until the instrument is closed down, periodically adding when the size becomes irrelevant in your portfolio.

Never held it and sold the options the night of Trump winning. Cut my losses 30% and never looked back.

VXX is a day trader if that.

I beg to differ. It’s a GREAT short to hold. I trade a lot of options around my core position, but I’ve had a direct short since 2013 and have added to it after reverse splits. VXX will always trend down for all the reasons stated in the above article. I consider spikes in VIX a gift from the market gods. Those are the times to add to the core position, write calls and/or ad a short term portion to the short. Sell and Hold VXX for sure.

Hi Vance-

What about “XIV” (reverse VXX) ………..is that effective or ineffective at moving up when the VIX declines ?

Hi Vance, on the VXX May 16 Calls – 20 Strike price, there is over 50,957 in open interest. Does that indicate anything? I am long with 20 contracts at that strike price. Not sure if I should get out or wait to see if there is small pop up on the VXX.

Hi Matt, I don’t think open interest is predictive, just means a lot of activity at that strike. Signals on market are quite mixed right now. VIX is low, historic volatility is low, VIX/VXV ratio is low, but RSI is high, VIX futures are at a premium. Your ~$500 position is essentially a bet on a big vol spike in the next couple of weeks. Feels to me like maybe a 20% chance it will pan out.

— Vance

An open interest is just an open option contract that is not closed yet: I write an option and you buy it from me – this constitutes an open interest.

I rarely ever go long VXX and never during times of serious contango like we are experiencing presently. Also, you don’t know if that open interest represents longs or shorts. I would be willing to be the open interest is ppl looking to sell calls. Short VXX on VIX spikes and then sit tight, short more when your position gets too small, and watch the proverbial paint dry. Isn’t VXX slated to be shuttered in 2019?

Hi wwt17,

VXX’s notes are scheduled to mature in 2019. Since it is a money maker for Barclays they will figure out a way to extend it, either by amending it, or opening up a new set of notes.

— Vance

It’d be nice not to have a big tax hit on VXX in 2019! Not really germane to the discussion, but I think shorts should be treated the same as longs as far as L/T, S/T cap. gains are concerned.

I want to write a call credit spread against VXX but my hesitation is that a reverse split is coming soon. Any idea what would happen if I had spread open?

Hi Iyad, First of all I think the reverse split will still be a while, historically VXX is trading around $13 when it happens. Nothing horrible happens to options when there’s a split. On a reverse split the strikes are reduced (4X in this case), so that the net value stays the same. Liquidity of the adjusted strikes might not be that good so it might make sense to exit before the split happens–there is advance notice of when they will happen. See https://www.sixfigureinvesting.com/2014/01/uvxy-reverse-split/ for more discussion on options and reverse splits.

— Vance

Would it not make sense for a long term investor to buy VXX while it’s so low, assuming that eventually volatility will increase? And after XIV hits near 52 week lows, sell VXX and buy XIV? Seems pretty straight forward. What am I missing?

Hi Chris, Being long VXX is only a short term strategy. VXX decays much like an option, so even though volatility will eventually increase from its current levels your losses due to the decay process will likely consume any profits you might get. Normal VXX losses are about 5% per MONTH.

— Vance

The VXX tracks futures prices. If volatility is anticipated to rise in the future, then this will already be reflected in the VIX futures and hence in the VXX. More technically speaking futures prices are semi martingales.

Hi Vance,

What do you think about short the VXX using options ( long puts ATM + short calls ATM ) instead to short directly the ETN?

David.

Hi David, The synthetic short long put / short call combination) will work. Right now it looks like you pay around a $1 premium for the ATM options, but that would probably be fairly stable until close to expiration. In VXX’s case no real worries about call option assignment because it has no dividends–and therefore no ex-dividend dates to worry about.

— Vance

Thanks Vance.

And I have another doubt. Is it possible to know how many new shares of VXX are “created” every year by Barclays? Do you thing that knowing it we could have an idea about which are Barclays future expected lost value of this ETN?

Thanks in advance,

David.

Hi David,

The number of VXX shares created / destroyed in a year is not knowable by anyone because it depends on investor inflows / outflows. Barclays does not control that. Normally VXX decays around 5% a month but that is dependent on the general state of the market (e.g, bear or bull) and the amount of contango in the VIX futures.

— Vance

Ok Vance,

But how it’s explained the difference in performance between VXX and XIV? If I supose the same investing amount every day ( long XIV vs. short VXX ), the profit obtained shorting the VXX is much more that can be explained for the ETN fee ( 0,89%/year ).

I understand that the two ways to trade have to be inversely similar, but in reality if you choose to short the VXX the profit substantially more than buying the XIV, even taking account for the expenses to borrow the shares.

What’s the reason? What is the effect that I’m not taking account and provoque that disparity?

Could you figure it?

Thanks, again, in advance. Your site is simply fantastic but it remains small compared with your kindness to help.

Regards,

David.

Hi David,

The mechanisms at play here are related to the compounding that is inherent to the operation of the daily resetting leveraged funds (-1X and 2x) . The compounding tends to erode the value of leveraged funds if the volatility of the underlying securities is high, and boosts them if the underlying security goes into a strong supporting trend.

I discuss the underlying operation in this post, https://www.sixfigureinvesting.com/2012/03/under-the-hood-of-a-leveraged-etf/ and I give some additional examples in https://www.sixfigureinvesting.com/2012/10/a-hat-trick-for-inverse-leveraged-volatility-funds/

The fairly frequent trips the vix has made into the 20’s recently has propped up the value of VXX and the general increase in the realized volatility of volatility has eroded XIV and SVXY.

Best Regards,

Vance

Hi Vance,

I don’t understand your above comment. The number of outstanding VXX notes is 100% percent controlled by Barclay’s since they are the only ones who can issue new bonds. Investor outflow cannot decrease the number of outstanding notes since you have to sell your notes to another investor. The 5% price drop per month decreases the total outstanding debt obligation Barlcay’s has to the VXX holders but does not affect the number of outstanding notes. The best way to think about the VXX is like a corporate bond whos value is index linked to to the short term VIX futures index.

Hi again,

I missed that you can redeem early so your are right Vance, sorry. If you look at my other recent post you will see that it is hard to redeem for a private investor. Also if you look at the net assets of the VXX at yahoo finance you can see that it is 1.13B and if you calculate the current value of all the notes Barclay’s has issued I get a value of 1.1B so it seems redemptions have been very rare or non-existent. If you want I can email you my spread sheet which has collected the information of all VXX issues.

Hi Anders,

I think it is important to distinguish between shares and the overall bonds/notes. Shares are easily redeemed/created by the authorized participants in interacting with Barclays, this happens all the time as the assets under management grow and shrink in the range of 100s of millions of dollars. Since inception more than $5 billion dollars of creation dollars for shares have flowed to Barclays. That’s not to say that all of that was profit for Barclays–they are certainly hedging their position, although maybe not at a 100% level.

— Vance

Hi Vance,

But in the case of an ETN as opposed to an ETF do any shares actually exist? Are you not trading the issued notes directly? To my understanding an ETN is not a fund and it does not hold the assets the note’s value is tied to. Isn’t what you call “the assets under management” simply the value of the 70M issued notes? This value will vary by hundreds of millions because of price changes in the VXX.

Split adjusted, Barclay’s has as of March 18, 2015 (I could not find any issue after that) issued 70M notes. The NAV yesterday (April 28th) was 16.22USD which gives a value of 1.135B USD which corresponds very closely to the 1.13B listed by Yahoo finance.

Barclays has issued new notes on 27 occasions since inception and raised 10.6B in capital which gives a profit of about 9.5B if unhedged. I have put all the issue dates, size of the issues and the VXX value at the issue dates in a spreadsheet if you are interested.

Hi Vance, if S&P reverses from here and drop back to 1800 in a month, wouldn’t VXX follows suit, meaning spike up? will it be a quick spike? I see that index like dow are moving 3 digits almost every other day…

Thanks Vance I checked on the spreads this morning and penny to the red cent! I appreciate your help and great article.

Vance,

Quick question you mentioned in the article bid ask spreads were slim, today it is like almost $2.45 dollars between bid and ask . I am wondering if this is normal or is it just because I am looking at it after a volatile day.

Source was Yahoo currently bid is 41.10 x300 ask is 43.55x 500 and the current price is 39.41. Just wondering if this is natural.

Hii, Those are after-market ask/bid prices. Check during regular market hours and you’ll see the penny spreads.

— Vance

Why wouldn’t a person just short this on the spikes and hold? Doesn’t it decay no matter what over time?

Shorting VXX is popular. However shorting the right spike can be tricky–volatility often has a triple spike before a correction is over. If youi’re too soon you better have deep pockets ’cause the margin calls will be a coming. Also, a short can at best give a 100% profit, see https://www.sixfigureinvesting.com/2014/03/short-selling-securities-selling-short/ If you hold your position for a long time a daily reset fund like XIV or SVXY will perform better.

— Vance

I will ask a stupid question, sorry about that, but why would anybody buy VXX over VIX ? I feel that VIX is much more appropriate for the kind of security people are looking for, as it follows properly SNP500 ? Thanks for the article !

Hi Michael, It turns out that’s not possible to directly buy the VIX. People talk like they do, but in reality they are buying a volatility future or exchange traded product–neither of which track the VIX very well. For more see: https://www.sixfigureinvesting.com/2010/01/how-to-go-long-on-the-vix-index-2

— Vance

Thank you very much ! I just bought some TVIX earlier today, do you expect any tendency from it ?

Your website is great by the way, thank you for dedicating this time to inform people, it’s really appriciated.

Regarding TVIX, just remember once volatility peaks and starts to decline TVIX’s value will drop very rapidly.

Vance, what am I missing here? The call prices don’t seem to indicate contango as the chart does. Why wouldn’t everyone just sell call spreads into perpetuity?

The risk is volatility spikes. If you get greedy you can lose a lot of money in a hurry.

— Vance

I actually found my answer. The calls trade richer so you’re going to risk more on the spread…still I’m not sure I get this underlying. It basically looks like a sure thing.

What I meant is where I could get my hands on the theoretical VXX time series, of course — not the futures data.

Hi Nick, I offer a spreadsheet that provides the theoretical VXX values (including fees) back to March 2004 for $30. As you suggested I generated it from the CBOE’s VIX Futures data–not a trivial task. If you’re interested send an email to [email protected].

— Vance

Nice article Vance! I’m just wondering where you got the VXX data for the 2004 to Jan 2009 period. I’m assuming you generated these theoretical values based on what the first and second forward futures contract prices were? Do you know where I could get my hands on that data? I would sure appreciate being able to save the time and headache of constructing the time series myself!

Hi Vance,

Based on the ETN nature of VXX I think Barclay might not be fully hedged and that might make Barclays an LTCM ver 2 in an adverse event. In my understanding, the ETN does not require physical holding of the corresponding futures or whatever replication portfolio. When Barclays issue one share of VXX at today’s price, simply it is collecting the 14.48$ as of 09/11/2013 and promises the buyer whenever you want to redeem/sell the share it is available. Under such scenario, Barclays essentially is shorting VXX or more broadly speaking shorting volatility. It is willing to do so because VXX is decaying like no return and generally it is very profitable to short volatility. If Barclay is not hedged at all it is collecting both the fees and the short profits (4.8$ Billion as you mentioned) in VXX.

However, this seemingly sweet deal could also blow Barclays up. If anadverse market event happens and VXX triples or quadruples in just a few days, Barclays might lose its profit for a whole year since during that turbulent period it might not be able to hedge its positions and its hedging action could only aggravate the crisis. With a Net asset of 1.15$billion and growing Barcalys could easily lose several billion dollars if most of the VXX holders are redeeming their shares.

That is just my wild guess and I hope nothing that catastrophic would happen. Not for the bankers, but for the ordinary working people. Any financial crisis could only make our life more miserable.

I agree that Barclays is probably not fully hedged, but I doubt their risk management controls would allow them to go completely unhedged. Historically the open interest on VIX futures does not drop all that much during market panics, even though the longs had huge profits–we do have 2007/2008 data on VIX futures. I think it relates to the tendency for people to want to jump on the band wagon–the momentum traders. That will tend to offset the people that are taking profits and exiting.

At this point I believe the VIX futures market could soak up a lot of demand without significantly distorting prices. Any significant price distortion creates arbitrage opportunities between VIX futures and SPX options. The SPX options market is incredibly deep with tens of billions of notional value in single strikes of single expirations dates. The VIX futures market is still way to small to move that market around.

— Vance

Hi Vance,

thanks for educating ‘the world’ about VXX and the like.

I have one question:

At what time of the day does the index that VXX tracks roll its future position (or does that even matter)? Is the roll executed ‘on the close’ (and when is that for VIX futures?) If it is on the close how do Barclays and other people who follow that index execute their hedge? I doubt they all do their roll at one time of the day.

How does that work?

thank you.

Hi Marco, The index that VXX tracks uses the closing (settlement) values of the VIX Futures for its computation. The close is at 4:15 ET. Yes it is a catch-22 situation. I don’t know the specifics of what goes on, but my understanding is that most of the day’s volume does occur at close. It appears that the exchange is accommodating the needs of the hedger by often extending trading quite a bit beyond 4:15. In September the CBOE plans to start VIX Futures trading for the next business day around 45 minutes after the normal close. This would allow hedgers to adjust their positions without taking overnight risk.

— Vance

thanks for your comments Vance

…is it time for a 10 to 1 split?

Probably won’t be until February– and will be a 4 to 1 split. https://www.sixfigureinvesting.com/2013/08/next-vxx-reverse-split/

— Vance

I have been writing call spreads on this piece of crap since march…They keep expiring worthless, I keep collecting premium. What a gold mine!

I just came across this because it was exactly what I was thinking. This seems to be the ideal spread situation. I can’t be that easy. Even though If you look at the ATM put and call the prob of expiring out of the money indicates the tendency of contango but the prices don’t! Am I missing something here? I know I have to be, it’s never this easy.

Hi JhM, It’s never easy in the long run. Being short volatility works great until a correction rips your ears off. Volatility can spike very quickly. I’m not sure what price disparity you are seeing. Put / Call parity will keep things roughly aligned even when the risk is asymmetric.

— Vance

Thanks for the quick response. I think I figured out the problem. Calls are really rich. I’m trying a skewed iron condor to the downside. I would normally make it a broken wing butterfly but the capital requirements go up 4x if you don’t cover the put side. Have you ever thought about a trade like this?

The premium available on the put side seems really thin–doesn’t seem worth the risk. Why not just call credit spreads?

Well I don’t really see any real risk to the down side. I skewed it taking into account that 5% a month loss to contango selling the 27 call and the 26 put 30 days out. That should work. This is a unique underlying. Are there any others that you know of that behave similarly and also have liquid options?

I suspect you’ll see your puts go ITM. VIX Futures have been riding a bit high in my opinion. Other vol ETP’s with options/decent liquidity: UVXY, SVXY.

This makes me wonder why CS got cold feet with TVIX. Really, issuing long VIX index ETNs is a bit of a gold mine.

Hi Andrew, I’ve been wondering the same thing. I suspect they panicked because the short term capital requirements were kicking up into the hundreds of millions and they were getting hit with expensive swaps, etc. If they were trying to hedge near 100% it could be ugly. On the other hand as you say, it’s a long term gold mine–if they’re willing to take some short term risk.

— Vance

this article is really great!!

thanks a lot Vance