Many people seem to believe that the CBOE’s VIX Futures market is attempting to predict upcoming CBOE VIX® values. I think they are mistaken. Most futures prices have very little to do with predicting the future.

Futures contracts were invented to allow producers/consumer of commodities to limit their business risk by locking in future prices. In exchange for eliminating price risk, they give up the potential for increased profits if markets later moved in their favor. Traders wasted no time using futures for speculation, not because they somehow foretell the future, but rather because the low margin requirements for futures allows them to heavily leverage their bets.

Prices for futures contracts are constrained by arbitrage. For example, if an arbitrager sees the premium for Dec 2016 E-mini S&P 500 futures rise above a certain point they will short E-mini contracts and buy the appropriate amount of stocks in the S&P 500 (or just short SPY). From this point on they don’t care what direction the market moves—they are perfectly hedged—a risk-free position. The transaction is triggered when there is sufficient difference between the current S&P prices (the “spot” price) and the December contract bid price to compensate for their cost of capital to buy the stocks, account for dividends, and deliver the target profit. Alternatively, if they think the futures price is too low, they reverse the transaction, buying the future and shorting the S&P 500. Companies will differ in how much premium they require between the spot price and the futures price but the net effect is that E-mini prices trade between these boundaries—they aren’t a divination of the S&P 500’s value in December 2016.

For physical commodities like corn or natural gas, the cost of storage is included in the futures pricing and in some cases seasonality. For example, prices for corn might be depressed during harvest time because some producers want to move the product directly to market so they don’t have to store it.

Arbitrage for VIX futures is a much trickier thing. You can’t buy volatility on the spot market and store it in your garage for a few months. The best you can do is buy or sell the appropriate set of S&P 500 (SPX) options—the ones that expire 30 days after the settlement date, and eventually subject yourself to the settlement process. Settlement is via the tweaky Special Opening Quotation (SOQ) process, which can’t even tell you ahead of time the full set of options that will be used for the settlement and in the last year has differed from the VIX opening price by as much as +4.27% / -3.8% on the morning that VIX Futures settle.

Monthly SPX options are only available for the next 4 or 5 months, so the options associated with further out VIX futures expirations (up to 9 months out) are sometimes not even available. Clearly, market makers in VIX Futures must have other ways to hedge their positions (e.g., VIX futures spreads, VIX options, calendar spreads of SPX options).

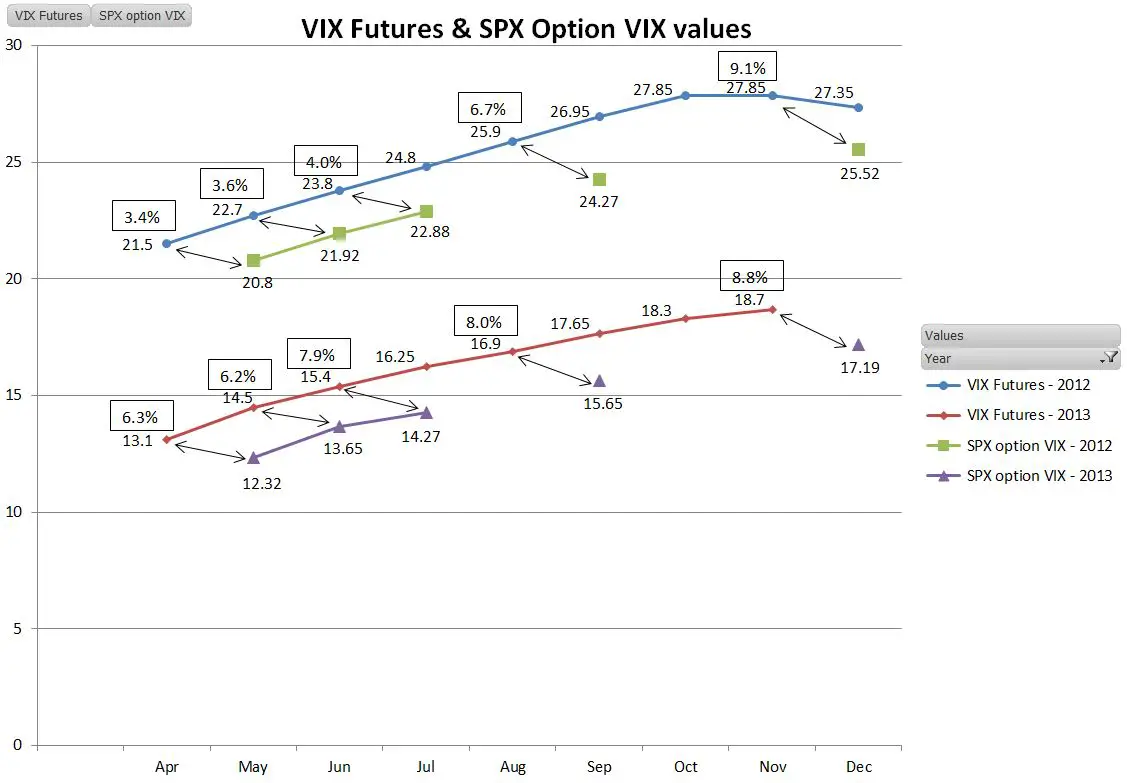

A quick look at historical data suggests that VIX futures tend to trade at a 3% to 9% premium to the VIX level of their associated SPX options. A chart with April 10, 2012, and April 11, 2013 data is shown below:

Since the notional value of the SPX options market is currently much bigger than the VIX futures value it is reasonable to assume that the VIX futures tail does not wag the SPX options dog. So the question becomes, what sets SPX options prices, and indirectly their implied volatility? Are the market participants seers or are there other factors at work?

First of all, by any measure SPX option implied volatility is terrible at predicting future volatility in any way other than general reversion to mean. If current volatilities are very low they predict an increase in volatility, if really high they predict it will drop. Short term they predict that tomorrow will be like today—brilliant…

Insurance is a better model for predicting SPX option prices. Investors use option strategies for price protection (e.g., fully hedge any market moves below a certain price), and as assets that reliably go up during serious market corrections or panics. Even if your puts aren’t in-the-money, they still go up a lot when volatility spikes.

An insurance company doesn’t try to predict when you will have losses on your house or car. It looks at the statistics and then charges a constant monthly rate they believe in aggregate will cover the claims they receive and over time deliver a reasonable profit. I think the VIX Futures market looks a lot like an insurance provider.

Two final notes:

- VIX Futures do have one seasonality pattern —the Christmas effect. Typically December VIX futures are slightly cheaper than the surrounding contracts because volatility around that time tends to be low—a lot of people are on vacation, and the market is closed for several holidays

- The VIX Futures term structure chart during quiet markets has gotten more linear in the last couple of years. This shift has dramatically increased the contango in the mid-term futures—much to the chagrin of the XVIX, VXZ, and XVZ ETNs. On the other (inverse) hand ZIV is a happy camper. Eli, from VIX Central speculates the curve straightened because there used to be a low-risk trade of shorting a VIX future month right before it started sliding down the steeper portions of the curve while being long the month after it as a hedge. This trade might have just gotten crowded or perhaps the increased volume in the later month futures driven by the volatility ETPs made the market more competitive.

I know this is a very delayed comment to this thread, but I hope you still get alerted. A quick question for you, if you would be so kind… In the above analysis you indicate a typical premium in values reflected in the VX futures, when compared to the associated SPX option IV (3%-9%). My question: did you attempt to model that premium so that you could use SPX options to accurately predict the VX futures price(s)? For example, are they perhaps related to the level of the VIX itself? the volatility of volatility?

I’ve experimented over the last 6 months (off and on) with using VIX at various maturities to accurately model futures contract prices. I’ve had some success, but have yet to really get a good model that correctly compensates for the variance that you describe above. If that was something that could be modeled with any level of accuracy, it would be pretty darn slick.

Why? What’s the objective? Developing a realistic set of synthetic VX futures that start back in the early 90’s when the VIX can be reasonably well approximated (across the curve). With synthetic futures, it’s then easy enough to create synthetic indexes that are the basis of VXX, VXZ, etc. – which would be pretty slick.

If you’ve got some good ideas on this front, I’d be happy to share the synthetic futures contracts that I then derive (I’ve got all the old options data – after going through some rounds with the guys in Chicago – the data is by no means “pristine” back in the earlier days).

(Technical note: I spent some time this afternoon looking at http://cfe.cboe.com/education/vixprimer/Features.aspx to determine fair market value via variances – I must be having a senior moment, as I can’t seem to make that work even for a simple scenario).

Thanks, Lee

Hi Lee,

Interesting project. To answer one of your questions, I only looked at a couple snapshots of VIX term structure data to get my 3 to 9% assertion. I’m assuming institutional arbitrage limits the deviation between the two at some level. I have noticed significant deviations between the term structure of VIX and the VIX futures–specifically during mid to late 2009 when the 1 month/3 month term structure diverged significantly between the two.

Have you developed the ability to generate the VIX values for various durations (e.g, 5 months) from the SPX option data? The CBOE VIX term structure data only goes back to 2010.

Best Regards,

Vance

Vance,

Thanks for another insightful post. I’m going to respectfully play devil’s advocate on this one and argue that VIX futures prices are predictions for future VIX levels.

In commodities futures markets, the price of the futures contract is often thought of as the spot price increased at the risk free rate, plus any convenience yield and minus any storage costs. Obviously the VIX has no storage cost or convenience yield. Also, the calculated VIX should not increase at the risk free rate, based on my understanding of that calculation; therefore, none of these three traditional factors should be determining the futures prices. From these factors alone, one would predict a flat VIX term structure.

The only remaining traditional theory for the term structure of futures markets is expected future VIX levels. Indeed, historical VIX term structures tends to ‘point to’ the historical mean, or at least a range around the historical mean: when the VIX is high, the term structure points lower, and when the VIX is low, it points higher. This may reflect people’s expectations for the VIX to mean revert, at least when it’s very low or very high.

This phenomenon also, I think, rules out the idea that contango in the VIX term structure reflects some form of risk premium. If it were, it is unlikely the VIX term structure would ever be backwardated, which it sometimes is. My question for you is, how would the insurance story explain backwardation, or even flat term structures, without also including expectations for future VIX levels?

Let me know what you think.

Hi Tim,

My analysis, although I emphasized the insurance aspect doesn’t exclude the predictive aspects of VIX futures. When the market is panicky, and the VIX is jumping then I think the shorter term VIX futures contracts do reflect a revision to mean prediction–often resulting in backwardation. It feels similar to seasonality factors to me, because it has a strong historical basis. In normal markets I think there is an arbitrage mechanism between VIX Futures and the associated SPX option expiration month (e.g, May Futures, June SPX options), it’s not particularly tight, but the data is pretty compelling. The calendar / horizontal skew of SPX options has been increasing since 2010, and if my analysis is correct this is driving the increased contango in the mid-term VIX Futures. The B&S model does not predict calendar skew. I’m inclined to attribute it to the same cause of vertical skew–that the markets have figured out that the B&S model does not correctly weight the probability of large negative moves in the market–and prices in an insurance style premium to cover that risk. To interpret that insurance premium as predicting a specific VIX value in a specific month seems very contrived to me, and I suspect has a near zero correlation to historical results.

Best Regards,

Vance

Hi Tim,

This paper might be of interest to you

Simon, David P. and Campasano, Jim , The VIX Futures Basis: Evidence and

Trading Strategies (June 27, 2012). Available at SSRN:

http://ssrn.com/abstract=2094510 or

http://dx.doi.org/10.2139/ssrn.2094510

Cheers,

Chin Soon