Update

Trade Options Weekly no longer appears to be around, but there are people still providing the same basic strategy (e.g, 5Percent{PerWeek.com). Be aware these are high risk strategies

Original Post

If you do any amount of browsing on stocks and options you’ve seen ads for services that tout weekly percentage gains of several percent. I’ve never really been tempted to investigate these—I reflexively put them in the generic too-good-to-be-true category, but when Trade Options Weekly offered me a free trial I couldn’t resist.

The first time I saw the weekly trades I gasped. While most of my option trades have risk/reward ratios between 1:1 and 5:1 the risk reward of these trades is typically 50:1 to 100:1. So, for a best case profit of $1000 I would need to put $50K to $100K at risk. A sharp market move against your position could wipe out all your capital—a 100% loss, in 3 days. The minimum required capital to put at risk is not trivial—in order to make a meaningful profit after commissions and subscription costs are subtracted around $15K needs to be invested.

A typical trade using this strategy would look like this:

Trade time: 1-August-2012 12.57pm

SPY Weekly Options expiring 3-August-12

Credit Spread

Sell: Put-133 for $.06

Buy: Put-132 for $.04

At a Credit of: $.02

Limit order good for the day

With $15K in capital, you would buy 150 of these spreads. Assuming commission costs of $18 (eoption.com), and factoring in one fourth of your $149.95 Trade Options Weekly monthly subscription cost ($37.5) your best case profit would be $244.5 and your worst case loss would be $14.755K.

Many of the Trade Options Weekly historical trades have only a $.01 credit, so the maximum profit on those would be $144.50. Commission costs would be much higher with many brokers (e.g., Fidelity: $127, optionsXpress: $239).

The only happy ending for these trades is expiration out of the money. With these razor thin margins there’s no room for closing out your position early at a profit. Any sort of hedging strategy would almost certainly eat up all your possible profit.

How risky is this trade?

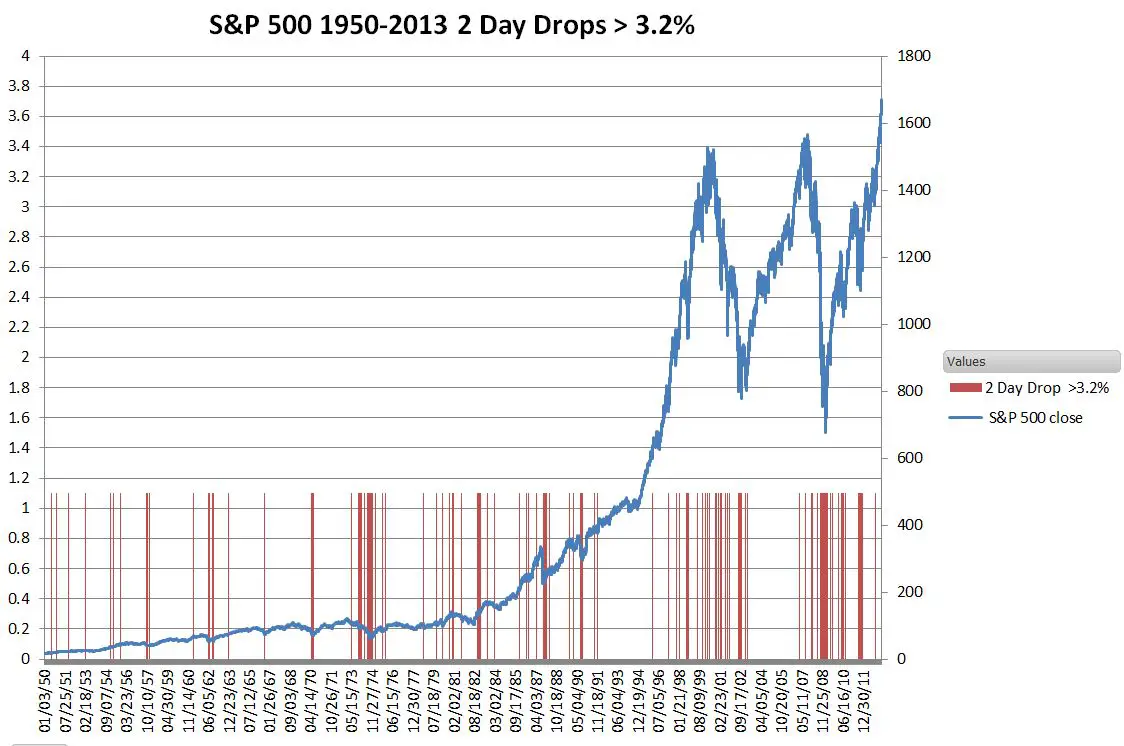

I don’t have intra-day data that far back, but SPY’s low on August 1st,2012 was 137.40, the day the position was created. So the short put (strike at 133) was at least 3.2% out the money when the trade was initiated.

The red bars in the chart below show the days where the S&P500 has closed down more than 3.2% in a two day period.

In the last 63 years there have been 247 instances of two day drops greater than 3.2%–an average of 3.9 times per year. The risk looks about the same for each trading day of the week, so if the average trade is only the last two days of the week that will reduce the risk by 3/5ths–for an average of 1.5 times per year. Some years (e.g., 1992 through 1995 and 2004 through 2006) didn’t have any drops this size most had at least a couple.

This isn’t particularly comforting…

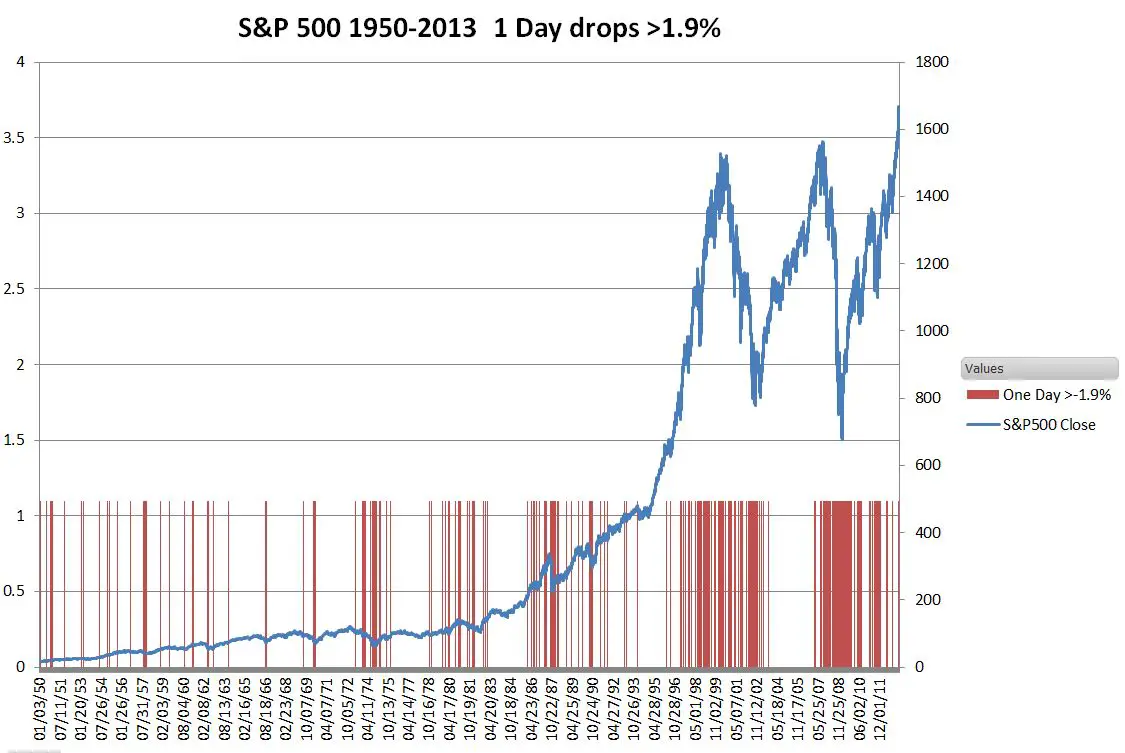

This particular trade did fine, but it had a bit of a scare. On the August 2nd, with one day until expiration the S&P dropped as low as 135.58, the short put only 1.9% away from being in the money. Drops of 1.9% in one day are more common—387 in the last 63 years.

However most of those drops were concentrated in bear markets. Note how the frequency of these drops has increased over the decades. We’re not imagining that the overall volatility of the market is increasing.

Most of the time, these trades will do fine, but if the market really does go south the position will be in trouble well before the short options go in-the-money. In this example, if SPY drops to 133.5 with one day to go your position will be in the red $2400 (assuming 150 spreads and 15 as the implied volatility). In most of these situations the mettle of your advisor will be critical. Will they get you out in time?

If the market drop is fast and severe (e.g., overnight crash, terrorist attack, flash crash) there will be nothing to do—your positions will be blown out with no way to recover, your entire investment will be gone. Of course almost everyone would be hurt badly in that situation, but it’s easier to recover when you’re not starting from zero.

Maximum loss of a credit spread is limited, how come you say the worst case loss would be $14.755K?

This is idiotic.

Excellent. Thank you for the data, Vance.

I think I am totally lost here and I don’t know if I am reading this correctly…

” your best case profit would be $244.5 and your worst case loss would be $14.755K.”

What you’re saying is that you are risking $15,000 to make a whopping $244.50 with the possibility of losing $14,755? Who, in their right mind, would make such a trade?!

Hi Niel, No, you are reading things correctly. I did gasp when I first understood what they were promoting. The $244.50 is a 1.6% gain in a week, with 15K at risk. Of course the shops promoting these strategies can show how their strategies have done well over recent history, don’t detail the worst case scenarios, and they extol the skills of the managers providing the trades.

That’s wild! Thanks for replying back so quickly!

you must take into account the probability of making the $244.50. Would you risk the $15,000.00 if you had a 99.999% chance of making the $244.50. I would take that trade at those odds. The trick to a credit spread is in how you adjust the position when the market works against it. In my opinion less than 1 in 100 people have the will power to make the necessary adjustments. They will freeze like a deer in the headlights and hang on to hope that the price action will push the trade back into their favor. The strategy will survive for the long run in how you adjust the trade when the market starts to really kill you. Very few people will adjust a credit spread to a loss or take the loss and close it out. I am not even sure I have the will power to do this and I have played around with options for years.

what about buying OTM options that are cheap that can gain 20-30% in $1 move in the underlying , where the strike is picked at the middle range of the underlying. for example, a delta of 0.1 on abc call that is around 0.1$, can double in price in a $1 move. off set the theta decay with a short position of equivalent value or a few percentage points more.

Typically it’s tough to counterbalance the theta costs without losing the upside for you–or picking up a lot of tail risk if things blow up. Commissions would be a factor too, because you’d have to buy a lot of options to make it worth you’re while. Never hurts to paper trade something for a while to get a feel for it. Consider what happens if IVs blow up, that cause do some counter-intuitive things.

— Vance

I think this is not a good strategy, the risk/reward ratio is bad.

but it gives me an idea, how if the positions reversed to debit spread?

buy 133put and sell 132put.

You may loss more often, but one win should cover those losses

HI Hendra, Your approach certainly would have much less risk. It could be discouraging to take a lot of 1 or 2% losses before having a winner.

— Vance

in the end, no matter what the strategy, you get the risk free rate

You are much better off with a Debit Spread for a 100 bucks, especially if you sell OTM call spread to finance your purchase, and you know the markets do not go up, especially at the top that they are in, parabollically …So your Credit Call Spreads are a safer short trade …