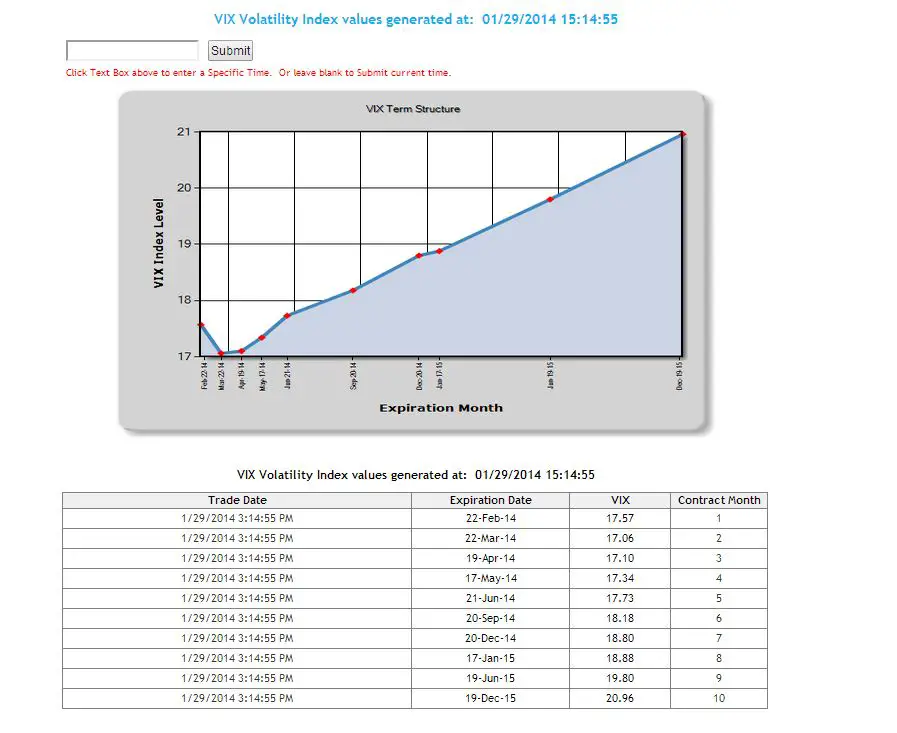

The VIX style calculation for the March 22nd SPX options closed today at 17.06. The data is from the CBOE’s VIX Term Structure website.

|

The CBOE will use the March SPX options to compute the settlement value for the February VIX Futures when they expire on February 19th.

February VIX futures, on the other hand closed at 16.25, a 5% discount to the March SPX options. The blue dot on the chart marks the VIX style calculation for the March SPX options.

|

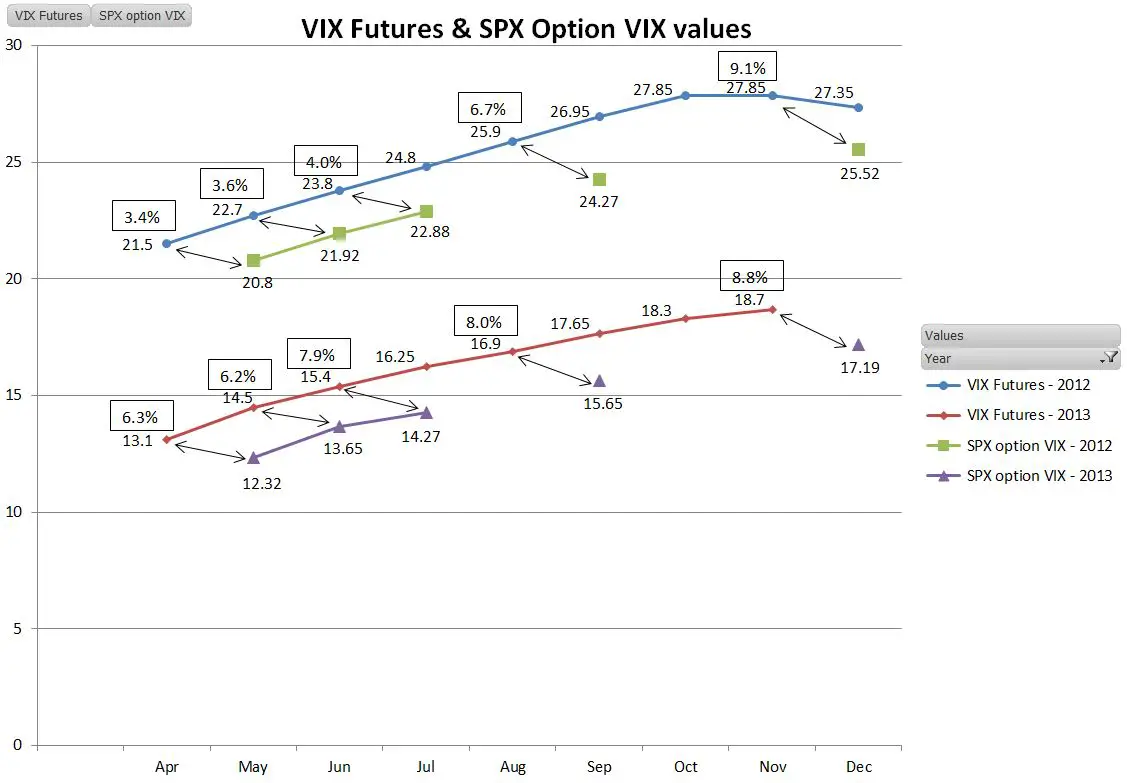

Normally VIX Futures trade at a 3% to 9% premium to the VIX style IVs of the SPX options that will be used to settle them.

|

This implies to me that profitable arbitrage of VIX futures using SPX options requires a difference between the two of around +-5% or more. Anybody have any insights on this?

For more background see: VIX Futures—Crystal Ball or Insurance Policy?

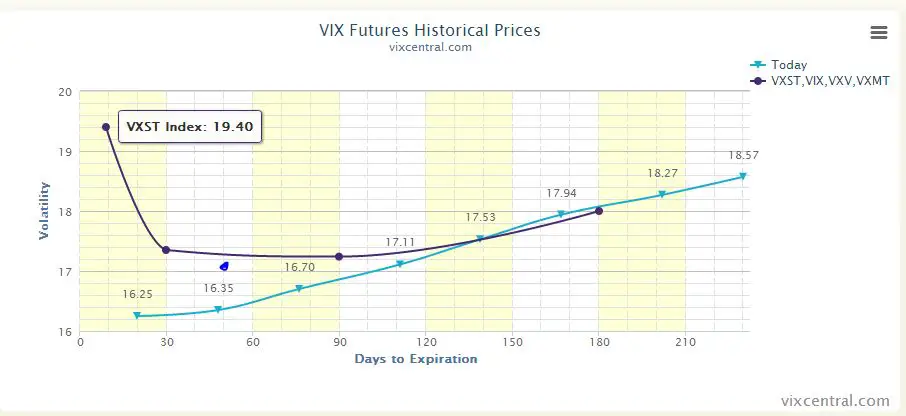

I just checked this earlier today using the vixcentral site for VIX futures term structure and CBOE site for calculated VIX term structure and the futures were trading at a discount to the VIX calculated values for the settlement calculation months. Honestly I’m too much of a novice to even know what to make out of that.

This is a very confusing area. The VIX values in the CBOE’s site you mentioned are not fixed duration (e.g, 30 days) so they can’t be compared directly to the futures of the same month. Also the futures use the SPX options that are a month out (e.,g the May futures settle to the June SPX option values when they have precisely 30 days before expirations.

— Vance

Well the fact that vix is now higher than front month futures seems to imply that some big profits are going to be there for long vxx buyers. Take a look at growth of vxx shares outstanding and it’s easy to see savvy buyers stepping in. Long term average spx vol near 20%. So a little taper, a little EM hysteria, an ordinary market correction and bang we should see a big vxx rise. Whereas pretty hard to see vol going much lower. At these vix levels vxx seems a great hedge by my calcs 0.5% vxx will level out drawdowns of 2009 magnitude.