UPDATE

Credit Suisse has terminated XIV due to a greater than 80% drop in its indicative value on 5-Feb-2018. The final payout was $5.99 per share. The last day of trading was the 15th of February. For more on what caused XIV’s crash see this post, for more info on the XIV termination process see this post.

—————————————————————————————————————————————

VelocityShares’ XIV and its sister fund ZIV are designed to go up when the volatility of the S&P 500 goes down. XIV has a shorter time horizon (1 to 2 months) whereas ZIV has a 5-month timeframe.

To have a good understanding of how XIV works (full name: VelocityShares Daily Inverse VIX Short-Term ETN) you need to know how it trades, how its value is established, what it tracks, and how VelocityShares (and the issuer— Credit Suisse) make money running it.

How does XIV trade?

- XIV trades like a stock. It can be bought, sold, or sold short anytime the market is open, including pre-market and after-market time periods. With an average daily volume of 29 million shares, its liquidity is excellent and the bid/ask spreads are a penny.

- Unfortunately, XIV does not have options available for it. However, its Exchange Traded Fund (ETF) equivalent, ProShare’s SVXY does, with five weeks’ worth of Weeklys with strikes in 50 cent increments.

- Like a stock, XIV’s shares can be split or reverse split—but unlike VXX (with 5 splits since inception) XIV has only split once, a 10:1 split that took its price from $160 down to $16. Unlike Barclays VXX, XIV is not on a hell-ride to zero.

- XIV can be traded in most IRAs / Roth IRAs, although your broker will likely require you to electronically sign a waiver that documents the various risks with this security. Shorting of any security is not allowed in an IRA.

How is XIV’s value established?

- Unlike stocks, owning XIV does not give you a share of a corporation. There are no sales, no quarterly reports, no profit/loss, no PE ratio, and no prospect of ever getting dividends. Forget about doing fundamental style analysis on XIV. While you’re at it forget about technical style analysis too, the price of XIV is not driven by its supply and demand—it is a small tail on the medium-sized VIX futures dog, which itself is dominated by SPX options (notional value > $100 billion).

- The value of XIV is set by the market, but it’s tied to the inverse of an index (S&P VIX Short-Term Futurestm) that manages a hypothetical portfolio of the two nearest to expiration VIX futures contracts. Every day the index specifies a new mix of VIX futures in that portfolio. This post has more information on how the index itself works.

- The index is maintained by the S&P Dow Jones Indices and the theoretical value of XIV if it were perfectly tracking the inverse of the index is published every 15 seconds as the “intraday indicative” (IV) value. Yahoo Finance publishes this quote using the ^XIV ticker.

- Wholesalers called “Authorized Participants” (APs) will at times intervene in the market if the trading value of XIV diverges too much from its IV value. If XIV is trading enough below the index they start buying large blocks of XIV—which tends to drive the price up, and if it’s trading above they will short XIV. The APs have an agreement with Credit Suisse that allows them to do these restorative maneuvers at a profit, so they are highly motivated to keep XIV’s tracking in good shape.

What does XIV track?

- XIV makes lemonade out of lemons. The lemon in this case is an index S&P VIX Short-Term Futurestm that attempts to track the CBOE’s VIX® index—the market’s de facto volatility indicator. Unfortunately, it’s not possible to directly invest in the VIX, so the next best solution is to invest in VIX futures. This “next best” solution turns out to be truly horrible—with average losses of 5% per month. For more on the cause of these losses see “The Cost of Contango”.

- This situation sounds like a short sellers dream, but VIX futures occasionally go on a tear, turning the short sellers’ world into something Dante would appreciate.

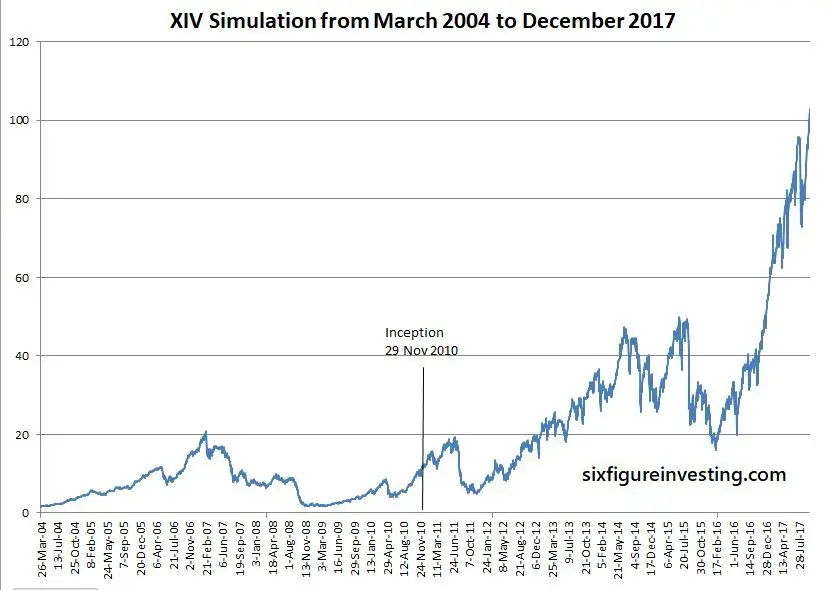

- Most of the time (75% to 80%) XIV is a real money maker, and the rest of the time it is giving up much of its value in a few weeks—drawdowns of 80% are not unheard of. The chart below shows XIV from 2004 using simulated values.

- Understand that XIV does not implement a true short of its tracking index. Instead, it attempts to track the -1X inverse of the index on a daily basis and then rebalances investments at the end of each day. For a detailed example of what this rebalancing looks like see “How do Leveraged and Inverse ETFs Work?”

- There are some very good reasons for this rebalancing, for example, a true short can only produce at most a 100% gain and the leverage of a true short is rarely -1X (for more on this see “Ten Questions About Short Selling”. XIV, on the other hand, is up almost 200% since its inception and it faithfully delivers a daily move very close to -1X of its index.

- Detractors of the daily reset approach correctly note that XIV and funds like it can suffer from volatility drag. If the index moves around a lot and then ends up in the same place XIV will lose value, whereas a true short would not, but as I mentioned earlier, true shorts have other problems. However, daily reset funds don’t always underperform. If the underlying index is trending down, they can deliver better than -1X cumulative performance. For more see “A Hat Trick for Inverse / Leveraged Volatility Funds”

How do VelocityShares and Credit Suisse make money on XIV?

- Credit Suisse collects a daily investor fee on XIV’s assets—on an annualized basis it’s 1.35%. With current assets at $1.3 billion this fee brings in around $17 million per year. That should be enough to cover Credit Suisse’ XIV costs and be profitable. My understanding is that a portion of this fee is passed onto to VelocityShares for their technical and marketing activities.

- I’m sure one aspect of XIV is a headache for Credit Suisse. Its daily reset construction requires its investments to be rebalanced at the end of each day, and the required investments are proportional to the percentage move of the day and the assets held in the fund. XIV currently holds $900 million in assets, and if XIV moves down 10% in a day (the record negative daily move is -24%, positive move +18 %) then Credit Suisse has to commit an additional $90 million (10% of $900 million) of capital that evening. If XIV goes down 10% the next day, then another $81 million infusion is required.

- Unlike an Exchange Traded Fund (ETF), XIV’s Exchange Traded Note structure does not require Credit Suisse to report what they are doing with the cash it receives for creating shares. The note is carried as senior debt on Credit Suisse’s balance sheet but they don’t pay out any interest on this debt. Instead, they promise to redeem shares that the APs return to them based on the value of XIV’s index.

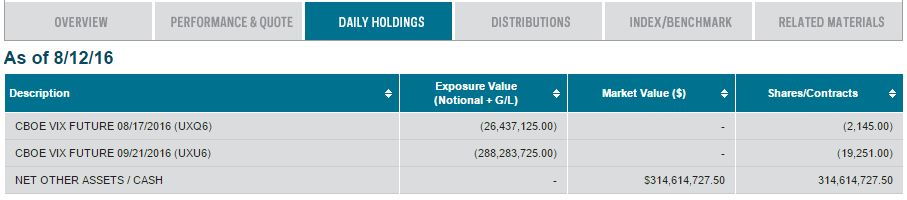

- Credit Suisse could hedge their liabilities by shorting VIX futures in the appropriate amounts, but they almost certainly don’t because there are cheaper ways (e.g., swaps) to accomplish that hedge. ETFs like ProShare’s SVXY can use swaps also, but they usually just use the futures. The picture below is a snapshot of their holdings on August 12th, 2016. The parenthesis denote a short position in the futures.

XIV won’t be on any worst ETF lists like Barclays’ VXX, but its propensity to dramatic drawdowns will keep it out of most people’s portfolios. Not many of us can sit tight with big losses in the hope that this time will not be different.

The eye-popping inverse volatility gains in 2016 and 2017 have pushed XIV’s assets beyond VXX’s but it will be interesting to see how the next few years go. I suspect we’ll see some bloodletting when people rediscover short volatility can be very volatile in its own right.

For more information

Thank you very much for this article! Very informative, and it’s super fun to learn about the

bizarre cast of characters that are VIX and friends.

You give the impression in your first paragraph that XIV has halted trading.

The Spike that killed XIV

According to the XIV prospectus the daily indicative value is calculated from the S&P VIX Short-Term Futures index ER with ticker SPVXSP. The spike in the index resulted in an increase in the index of about 95% and hence a drop in the XIV indicative value of 95%.

What is interesting is that no such spike can be seen from yahoo finance for S&P VIX Short-Term Futures (without the ER) but with the same ticker.

-50% and -95% is a pretty large difference.

Yahoo usually uses the wrong closing time 4PM ET. The VIX futures and associated ETPs all use the settlement time of the VIX futures as the close, it’s 4:15PM ET or later. In this case 15 minutes was a very big deal.

haha, it doesn’t anymore

“XIV can be traded in most IRAs / Roth IRAs, although your broker will likely require you to electronically sign a waiver that documents the various risks with this security.” meanwhile XIV is down 96 points right now

Vane,

Do you have any idea why XIV stock price ($137.61) is diverging from the Indicative Value ($133.66). The difference is almost 3%. Data from VeloictyShares website from 1/25/18 close.

Thanks

Hi Mark, Just tweeted something out on this: https://twitter.com/6_Figure_Invest/status/956918383030579200 no telling if this will persist or not.

Thanks

Hello Vance, Hope you are doing well. I see that VXX spiking with SPY rising and the situation may continue if market continues melt up. And if Market falls a bit, then Probabyly VXX will spike too (natural behavior) .. Under these conditions, is it good to short SPXU (3x bear of SPY) than shorting VXX/UVXY. Thank you for your inputs as always.

I guess the reason was that the turd was entering the cage.. just ahead of the fan. I hope you did not suffer too badly here.

Had a very small stake in the volatility universe split 50/50 between XIV and ZIV. At least, ZIV is still alive.

Hi Vance,

If there were a sudden spike in VIX or a daily sequential upward moves in VIX that are large enough to bring XIV (or another ETF like VMIN) fairly close to zero during a market session, what happens next? Does the fund shut down? Or will the issuer do a reverse split to keep the ETP tradable? Thanks.

Hi rttrader, In the situation you describe the funds would close out their positions during the day. The final value of the fund would be the resulting cash value of the fund divided by the number of shares outstanding. That value is guaranteed to be no less than zero.

Good guess. As of today, Feb 16, XIV is no more.

Been running some numbers. XIV seems to a much better bet. I basically assumed buying either one @ a 50% discount from the current price and then calculated the profit when it rebound.

https://uploads.disquscdn.com/images/4f910c11e9263262a8cfdbf4a6ed215589cca040994c790d49ce1c702af73e04.png

Vance, with XIV at all-time high of $78 and VIX at all-time low around 10, what’s your suggestion for people with mostly cash and don’t know when to buy XIV? Should one stay sideline and wait for the drawbacks? Should one just buy high and sell higher? During the 4 months between December 2016 and end of March 2017, VIX stayed around 12 and moved sideways. XIV went straight up $45 to $70 in the same period and broke out the $50 resistance back in August 2015. Can history repeat itself? Thank you!

Hi Jack, History could repeat itself, but volatility always manages to surprise us. I don’t recommend specific strategies. You can check out my blog roll to see some of the paid services out there.

Vance

Hi Vance/all,

Interesting to read about how XIV works, with XIV-IV. I notice sometimes the difference between XIV-IV and XIV lasts for a while. Is there a way to exploit this? For example buy XIV when it’s below XIV-IV, and short XIV when it’s above XIV-IV? Since after a short time it should rise/drop respectively to match XIV-IV? Thanks, – Tony

Vance, I have read your articles more than once to keep my faith in XIV. I really enjoy reading them. Thank you!

One question I could never get an answer for: Nasdaq site shows the short interest is about 190% now for XIV and even higher before. What does that mean? Does it matter to daily trading? Cheers!

Hi Jack, My best guess at the short interest is that traders are using a short VXX, short XIV style pairs trade to capture the compounding loss that XIV sometimes has. For more see https://www.sixfigureinvesting.com/2011/11/pairs-trading-short-vxx-and-short-xiv/ Since Exchange Traded Products are designed for incremental share creations they aren’t susceptible to “short squeeze” situations that a stock in a company might experience. for more on that see https://www.sixfigureinvesting.com/2010/09/short-squeeze-on-etf/

The bottom line is that the high short interest does not impact daily trading negatively, and probably helps by increasing the amount of trading that’s going on.

Thank you for the explanation, Vance. BTW, short interests are 200% for SVXY, 100% for VXX, 70% for TVIX, and only 33% for UVXY. How interesting!

Hey Vance, nice article. It appears in the prospectus that an investor needs to have 25k shares of XIV for early redemption. Is this true? Can I just own a couple shares to try it out?

What about SVXY? Is it the same?

Thanks

Hi Bluff, The references to 25K shares are just if you want to directly interact with the issuer (Credit Suisse). You can buy / sell one or more shares of XIV just like a stock on the exchanges. SVXY is the same way.

Vance

Thanks! So the way I understand the fee structure is that CS charges the 1.35% ÷ by 365 days?

*or is it divide by actual trading days, not all days?

They use calendar days, so it’s 365.

Hello Vance,

New member here and what a great site on little-known alts. Great article and very true how XIV is not as popular as the others mentioned. For those of us young enough and has the gumption to stomach the occasional scary draw-downs, I would imagine one can make a tidy gain of ~20%-25% per annum over a long-term period, say 15-25 years?

However, one potential risk would be the unlikely, but possible bankruptcy of Credit Suisse, since the product is only as good as the parent that sponsors it? Am I correct in thinking this?

Sincerely,

Sam

Hi Sam,

Choppy markets and bear markets are tough on the inverse vol funds. Long term I think you’re probably right that the long term gain will be good, but not a sure thing. I don’t worry too much about the big banks failing. I think there would be some time to get out if they look shaky, but there’s an easy alternative: SVXY (or VMIN). These are both ETFs that hold the underlying assets, so they have less credit risk. SVXY does generate K-1 forms so the taxes are a little more complicated, but that’s not a big deal with them generally.

Dear Vance,

thanks for the great site. I’m still wondering if it is better to hold XIV or short VXX (both long term and short term). If I don’t account for the disadvantages of a short position and purely look at the profit side of the trade it seems short VXX is more likely to be profitable (definitely in long term).

I remember I read one of your comments here that holding XIV should be better short and long term but now I can’t find that. Any comment on this?

Thanks.

Hi Martin, It’s not a straightforward call. If you haven’t seen https://www.sixfigureinvesting.com/2016/10/is-shorting-uvxy-tvix-vxx-the-perfect-trade/ and https://www.sixfigureinvesting.com/2014/03/short-selling-securities-selling-short/ I’d recommend you read them. In my opinion a short position carries more risk and requires more attention (e.g, to keep the leverage ratio reasonable). XIV limits your loss to your initial investment, doesn’t require rebalancing, and can do better than a short in a trending market, but it will be eroded if volatility itself is volatile.

Hi Vance, You have some solid info posted on VIX and I’m enjoying reading through it. Are you able to explain what this means for XIV http://finance.yahoo.com/news/credit-suisse-places-conditions-acceptance-204500232.html

Hi Smoked, Thanks for bringing this news to my attention. What it means is that the issuer of XIV, Credit Suisse is protecting themselves by making sure their hedging costs are consistent with the price that they create new shares at. Issuers of ETNs like XIV buy or sell shares to institutional entities called authorized participants (APs). These APs are market makers or deal directly with market makers. If Credit Suisse sells XIV shares to an AP, then they will hedge their exposure, often with over the counter instruments called swaps. If these swaps got too expensive then Credit Suisse would start losing money on the transaction–not something they will tolerate for long. This change to the prospectus allows Credit Suisse to require the APs to sell to them the swaps required for hedging at a price that allows them to be profitable. If these swaps starting getting expensive then the APs / market makers will start charging a premium for XIV in the retail market–you’d see a divergence between the bid/ask prices and the indicative value price. TVIX is in this situation now–has been for a long time.

— Vance

So does that mean that market factors aside XIVs price should increase because of this?

I’m not seeing any impact right now. What sort of market factors do you have in mind?

Should have been more clear. I was saying that based on my understanding of your comment aside from the daily market factors that cause XIV to go up or down. If these APs are charging a premium for XIV on the retail market wouldn’t it make the shares themselves more valuable?

Well, I’m seeing XIV is trading at a discount to the IV value some of the time. It could be that this will continue since the APs are faced with the other side of the swaps (bid vs ask) vs what they are dealing with on TVIX. Need to think about this some more…

Thanks for the insight. Are you able to explain the impact it’s having on TVIX?

Looking at ETF.com it looks like TVIX’s median premium over IV value is 1.7%, XIV’s premium is around 0.25%.

Saw some changes in prospectus. How those changes affect the ETF going forward?

How can the VIX and the XIV both be down over 1% on the same day?

XIV is tied to VIX Futures, which sometimes have a mind of their own relative to the VIX. It’s not that unusual for the VIX to be down and the VIX futures to be up–which results in XIV dropping.

Great article. I have a VIX/XIV strategy where I add more XIV at predetermined VIX levels (spikes in the VIX) and then sell at a VIX floor level if you will. What do you think of this strategy? I am noticing some faults, namely that VIX returns to it’s baseline faster than XIV can increase to a profitable level, so I have to hold XIV and hope the market stays flat for a few days.

Alternatively I am thinking of an even simpler method where I only look at XIV. I buy a bundle of XIV every time it drops $5 with a plan to sell when it goes up $5. For example, I would buy at $30 and then sell at $35 or buy more at $25. Buy more at $20 or sell the second lot at $30. $5 is an arbitrary increment but this strategy takes the VIX out of the equation.

Thoughts?

Hi Ryan,

It’s been a tough 12 months to be short volatility. The volatility of volatility has been high enough to drag down returns of the inverse funds despite persistent contango.

Regarding your new strategy, I think the key issue is your ability to withstand the horrific drawdowns that short vol can give you. If we go into a major correction or bear market it would be a long time before your position would be profitable. Eventually it would be, but you need to have both the capital and the psychology to live with large losses on your position.

— Vance

I’ve used almost the same strategy successfully in the last few years with gains of approximately 25-40% / year. Yes you indeed need to possess the psyche to withstand the horrific declines. I sat pat, down as much as 90K one time around. At times like this, you start to think about what you could have bought with that money…”used Ferrari, studio condo out of the city…” I’m in 7000 shares at 22.4 now, looking for an out of around 40.

Vance, great information. Every time I come back to this page I learn something new. One thing I noticed that I wanted to ask, you wrote, “the price of XIV is not driven by its supply and demand”. Do you have a source for this because the VelocityShares prospectus on page 34 states:

“supply and demand for the ETNs in the secondary market, including but not limited to, inventory positions with any market maker or other person or entity who is trading the ETNs (supply and demand for the ETNs will be affected by the total issuance of ETNs, and we are under no obligation to

issue additional ETNs to increase the supply),”

The prospectus is for all the ENTs so the statement above may not apply to XIV?

Hi Anthony,

I should qualify this statement. At the macro level XIV’s price is driven by VIX futures prices–a large and liquid market. The flows in and out of XIV are trivial compared to the action in VIX futures–hence my statement that XIV’s price is not driven by its supply and demand.

However at a micro level the price of XIV does fluctuate based on market forces. For example heavy demand would tend to increase the price of XIV up, but when that price increases to a point that its premium over the underlying VIX Futures is significant the authorized participants, the institutions that actually transact with the ETP’s issuer, will instigate an arbitrage transaction (sell XIV short, buy the offsetting VIX futures in this case) that guarantees them a profit. This short selling will tend to drive the price of XIV back down. They are happy to do this all day long if the premium persists.

In XIV’s case the median difference between XIV’s price and the value of the underlying VIX futures is 0.12% (http://www.etf.com/XIV) so the premium required to do this arbitrage in XIV’s case is quite small.

— Vance

Vance, if the current ow volatility is the norm for the next few years will XIV prosper or will it trade more or less sideways (assuming VIX hs minimum variance from today’s levels)?

Very helpful comments all around. In the case of xiv and svxy, what is the relationship between total assets and market cap of the fund? Is the total assets (on which their fees are based) more or less the same as market cap? In the case of xiv, one source indicated that total assets is a simple calculation based on total notes outstanding times current price; i believe this would also be the calculation for market cap.

Hi James, for Exchange Traded Products the total assets and market cap are the same thing. Shares outstanding times share prices gives market cap / assets under management. Fees are just percentage of your position (e.g. 1% annual cost).

— Vance