Update 20-Oct-2023

Credit Suisse announced yesterday that it will be closing a set of Exchange Traded Notes that include volatility ETNs TVIX, VIIX, and ZIV. These funds had been closed to share issuance since July-2020, signaling that Credit Suisse (CS) was exiting this business. However, rather than closing down the funds at that point by accelerating their maturity date (2030), Credit Suisse choose to let them languish in over the counter trading, sometimes call the pink sheets.

The reason for this decision was clear, the long term prognosis for most of these funds was for a decline in value (driven by term structures in contango, and volatility drag. By not immediately closing out these funds, which would require paying out cash for existing shares, CS could let their liability erode away over time. With TVIX at least, this was successful, its current trading price today is $0.19 per share. This worked out well for CS, but caused investors pain, specifically with one of the funds, $DGAZ that was put in this mode. With creations halted, one of the key mechanisms for keeping an ETP tracking its underlying index is disabled. Without share creations there’s no way for market participants to reliably profit when an ETP is trading significantly above its index price. In July 2020 speculators drove $DGAZ’s price from it’s index value of ~$120 up to a peak of $25000 in a matter of days. Anyone short $DGAZ shares was in a world of hurt. Many were blown out of their positions, at outrageous prices by their broker’s margin calls. Credit Suisse ended the DGAZ fiasco by terminating DGAZ, which closed out remaining shares at the index price, but the damage was done. Fortunately, CS’s relatively rapid response to this discouraged similar attempts with the remaining ETNs, but overall it showed a callus disregard for the well being of the people using their products. For more on the $DGAZ debacle see DGAZ Horror,

Update 12-July-2020

Effective July 12, 2020 TVIX was delisted on national exchanges (press release). The issuer, Credit Suisse (CS) halted share creations effective July 3rd but is not terminating the fund. They reserve the right to do so but don’t have to until 2030. TVIX is currently trading on OTC exchanges, e.g., OTCMarkets.com and is currently trading pretty close to its IV price, the theoretic value of the VIX futures TVIX would be holding today. An OTC quote on TVIX is available here: https://finance.yahoo.com/quote/TVIXF. As of 6-July-2020 Schwab and Ameritrade are still providing IV value quotes ($TVIX.IV) and (TVIX.IV) respectively.

With share creations halted TVIX’s OTC price may climb above its IV price, depending on OTC demand and the availability of TVIX shares to borrow and short to create short positions. There is definitely a floor price, close to the IV price because Credit Suisse is still redeeming (buying back) TVIX shares at the IV price. If a significant discount developed traders could make risk free profits by buying cheap TVIX shares and redeeming them with CS at the IV price.

If a premium price develops be aware it can go away in an instant if Credit Suisse decides to terminate the fund. In that case all the shareholders at that point will have their shares cashed out at a final IV price.

If you want to sell your TVIX shares contact your broker. They may be willing to close out your shares at the end-of-day IV price without going through the OTC market. For TVIX, Credit Suisse is willing to work with your broker to close out even one share lots–although the fees might be substantial.

—————————————————————

VelocityShares’ TVIX Exchange Trade Note is a 2X leveraged fund that tracks short term volatility. This post will discuss TVIX‘s inner workings, including how it trades, how its value is established, what it tracks, and how VelocityShares makes money on it.

How does TVIX trade?

- For the most part, TVIX trades like a stock. It can be bought, sold, or sold short anytime the market is open, including pre-market and after-market time periods. With an average daily volume of 30 million shares, its liquidity is excellent and its bid/ask spread is a penny.

- Like a stock, TVIX’s shares can be split or reverse split. In fact, TVIX has reverse split 6 times since its inception in November 2010. You can see TVIX’s history of reverse splits and my predicted date for the next reverse split here.

- TVIX has a 1.5X leveraged Exchange Traded Fund cousin—ProShares’ UVXY. It used to be 2X leveraged also but was deleveraged after the February 5th, 2018 volatility Volmageddon.

- Unlike the 1.5X leveraged UVXY there are no options available on TVIX.

- TVIX can be traded in most IRAs / Roth IRAs, although your broker will likely require you to electronically sign a waiver that documents the various risks with this security. Shorting of any security is not allowed in an IRA.

How is TVIX’s value established?

- Unlike stocks, owning TVIX does not give you a share of a corporation. There are no sales, no quarterly reports, no profit/loss, no PE ratio, and no prospect of ever getting dividends. Forget about doing fundamental style analysis on TVIX. While you’re at it forget about technical style analysis too, the price of TVIX is not driven by supply and demand—it’s a small tail on the medium-sized VIX futures dog, which itself is dominated by SPX options (notional value > $100 billion).

- According to its prospectus, the value of TVIX is closely tied to twice the daily return of the S&P VIX Short-Term Futurestm .

- The index is maintained by S&P Dow Jones Indices. The theoretical value of TVIX if it were perfectly tracking 2X the daily returns of the short term index is published every 15 seconds as the “intraday indicative” (IV) value. Yahoo Finance publishes this quote using the ^TVIX ticker.

- Wholesalers called “Authorized Participants” (APs) will at times intervene in the market if the trading value of TVIX diverges too much from the IV value. If TVIX is trading enough below the IV value they start buying large blocks of TVIX—which tends to drive the price up, and if it’s trading above they will short TVIX. The APs have an agreement with Credit Suisse that allows them to do these restorative maneuvers at a profit, so they are highly motivated to keep TVIX’s tracking in good shape.

What does TVIX track?

- Ideally, TVIX would exactly track the CBOE’s VIX® index—the market’s de facto volatility indicator. However, since there are no investments available that directly track the VIX VelocityShares chose to track the next best choice: VIX futures.

- VIX Futures are not as volatile as the VIX itself; solutions (e.g., like Barclays’ VXX) that hold unleveraged positions in VIX futures typically only move about 55% as much as the VIX. This shortfall leaves volatility junkies clamoring for more—hence the 2X leveraged TVIX and the 1.5X leveraged UVXY.

- TVIX attempts to track twice the daily percentage moves of the S&P VIX Short-Term Futurestm index (minus investor fees). This index manages a hypothetical portfolio of the two nearest to expiration VIX futures contracts. Every day the index specifies a new mix of VIX futures in that portfolio. For more information on how the index itself works see this post.

- TVIX’s tracking to its target index is not as good as UVXY’s. I’ll get into the details of why later in the post, but on average you pay a premium of around 1% to 3% for TVIX shares relative to the index it tracks, compared to a premium of 0.25% for UVXY. For a security as volatile as TVIX this is not an especially big deal, but worth knowing.

- If you want to understand how 2X leveraged funds work in detail you should read this post, but in brief, you should know that the 2X leverage only applies to daily percentage returns, not longer-term returns. With a leveraged fund, longer-term results depend on the volatility of the market and general trends. In TVIX’s case these factors usually (but not always) conspire to dramatically drag down its price when held for more than a few days.

- The leverage process isn’t the only drag on TVIX’s price. The VIX futures used as the underlying carry their own set of problems. The worst being horrific value decay over time. Most days both sets of VIX futures that TVIX tracks drift lower relative to the VIX—dragging down TVIX’s underlying non-leveraged index at the average rate of 7.5% per month (60% per year). This drag is called roll or contango loss.

- The combination of losses due to the 2X structure and contango add up to typical TVIX losses of 15% per month (85% per year). This is not a buy and hold investment.

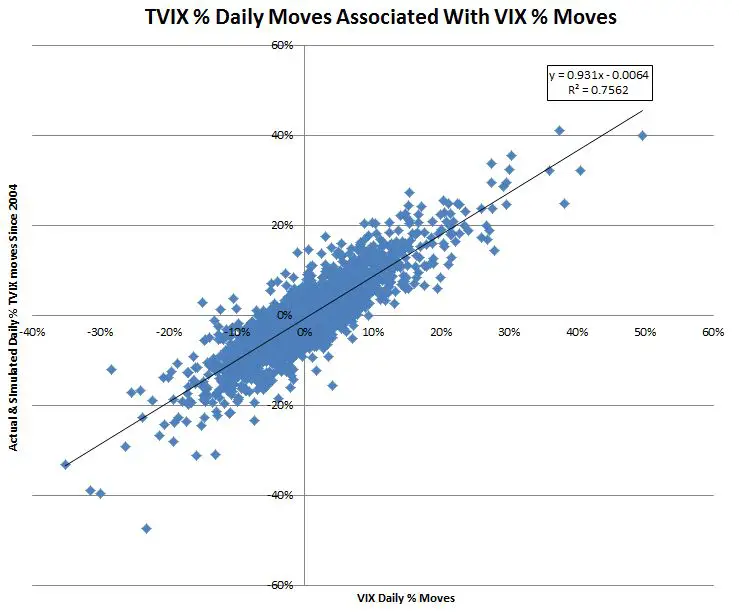

- On the other hand, TVIX does a decent job of matching the short term percentage moves of the VIX. The chart below shows historical correlations with the linear best-fit approximation showing TVIX’s moves to be about 93% of the VIX’s. The data from before TVIX’s inception on October 3, 2011, comes from my simulation of TVIX based on the underlying VIX futures.

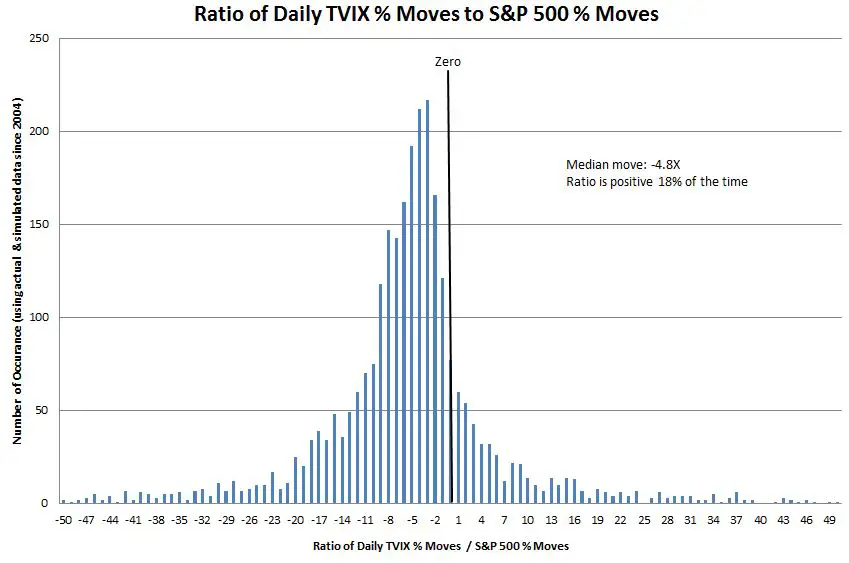

- Most people buy TVIX as a contrarian investment, expecting it to go up when the equities market goes down. It does a respectable job of this with the median TVIX’s percentage move being -4.8 times the S&P 500’s percentage move. However 18% of the time TVIX has moved in the same direction as the S&P 500. So please don’t say that TVIX is broken when it doesn’t happen to move the way you expect.

- The distribution of TVIX % moves relative to the S&P 500 is shown below:

- With erratic S&P 500 tracking and heavy price erosion over time, owning TVIX is usually a poor investment. In fact, even the provider’s marketers who you’d expect to figure out a positive spin, state that “The long-term expected value of your ETNs is zero.” Unless your timing is especially good you will lose money.

How do Credit Suisse and VelocityShares make money on TVIX?

- Credit Suisse, TVIX’s issuer, collects a daily investor fee on TVIX’s assets—on an annualized basis it’s 1.65% per year. With current assets of around $900 million, this fee generates approximately $15 million per year. That should be enough to cover TVIX costs and be profitable, however, I suspect their business model includes revenue from more than just the investor fee.

- VelocityShares (now owned by Janis Capital Group) – gets a portion of the investor fee for its marketing and branding efforts.

- Unlike an ETF, TVIX’s Exchange Traded Note structure does not require Credit Suisse to specify what they are doing with the cash it receives for creating shares. The note is carried as senior debt on their balance sheet but they don’t pay out any interest on this debt. Instead, they promise to redeem shares that the APs return to them based on the value of its index—an index that’s headed for zero.

- To fully hedge their liabilities Credit Suisse could hold the appropriate number of VIX futures contracts, but they almost certainly don’t because there are cheaper ways (e.g., swaps) to minimize their risks. Given TVIX’s inexorable journey towards zero, it would be tempting to assume some risk and not fully hedge their TVIX position, but I doubt Credit Suisse has a corporate culture that would support that. Instead, I suspect they put fund assets not needed for hedging to work earning interest on relatively safe investments like collateralized repurchase agreements. Earning even an extra percent or two annually on $900 million is real money.

February through March 2012 —When TVIX was not working

- In February 2012 TVIX’s assets were growing rapidly, climbing several hundred million in a few days to reach $691 million. Normally this would be viewed as a very good thing by an ETN’s issuer, but Credit Suisse was not happy. With a daily resetting fund like TVIX positions need to be rebalanced daily, and with a 2X leveraged fund the positions adjustments needed are equal to the day’s percentage move times the asset value of the fund. So if TVIX was to move +30% in a day, not unprecedented, and the assets were at $690 million, then an additional $207 million in hedging securities would need to be purchased that day at close of the VIX Futures marke. We don’t know the reason, but likely because of the costs of doing that hedging or the risks of a swap’s counterparty defaulting Credit Suisse decided to stop creating new TVIX shares on February 22, 2012. This prevented the assets of the fund from growing any larger.

- You might think that limiting the number of shares in an ETN would be a good thing for the shareholders—if shares are scarce they might become more valuable. But for exchange-traded products this is a very bad thing. The share creation mechanism is essential to the process that keeps the fund closely tracking its underlying index. Specifically, if TVIX’s value gets too high relative to its index the authorized participants will normally short TVIX and hedge that position with VIX futures-related securities to lock in a risk-free profit. They will continue to short sell, driving down TVIX’s price until the gap between TVIX and the index is too small for this arbitrage transaction to be profitable.

- Short selling requires that there be shares available to be borrowed, and with Credit Suisse no longer willing to create new shares the supply of borrowable shares dried up completely. As a result, TVIX’s share value became untethered from its index and by the end of March was trading at a 90% premium to the index. In market cap terms there was around $277 million of bogus value in TVIX.

- In late March 2012 Credit Suisse resumed share creation and the TVIX premium evaporated instantaneously—leaving a lot of stunned and poorer shareholders. Credit Suisse’s solution to their problem was to lay more of the risk on the authorized participants, requiring them to provide the necessary securities before they would create shares. The extra cost of doing this is reflected in the premium (often around 1%) in TVIX’s price over its index.

Important Dates

- TVIX Inception 29-November-2010

- Credit Suisse puts TVIX creations on hold 22-Feb-2012 post

- Credit Suisse resumes TVIX creations 22-March-2012

- Reverse splits: See this post

- TVIX delisted from national exchanges 12-July-2020

TVIX—destroyer of wealth

- According to ETF.com’s ETF Fund Flows tool, TVIX’s net inflows have been around $2.8 billion since its inception in 2010. It’s currently worth $900 million, so VelocityShares has facilitated the destruction of over one and a half billion dollars of customer money—so far. I’m confident this overall destruction will continue.

TVIX’s race to zero attracts a lot of short sellers. That strategy works most of the time, but if your plan is to ride out any volatility along the way be prepared to handle a 4X or more spike in TVIX”s value. Most people are unequipped both financially and emotionally to handle this sort of reversal. If you are considering selling TVIX short please read Is Selling TVIX Short the Perfect Trade.

TVIX has a proven record as a cash incinerator, but its occasional upward spikes continue to attract speculators hoping to profit from the anguish of the general market. A few traders with impeccable timing or good luck will make good money going long on TVIX. Most will lose money.

If trump halts the stock market for 7 days, what would you expect the % change of TVIX to be the day trading reopened?

No idea. I suspect it would really depend on the events of thse 7 days.

Thanks for the great lesson. I was wondering, for markets like TVIX and anything else where the value is dependent upon other stocks, how do traders actually affect that market? I imagine that the way I view things like TVIX is not like how I’d typically trade using chart patterns and prediction short squeezes but just by overall market direction and more macroscopic factors?

I can’t seem to find a concrete answer about this anywhere, so I hope you find a opportunity to see this four years later.

Hi Joshua,

At a micro level supply & demand does impact the value of TVIX but if that price deviates too far from the indicative value established by the underlying VIX futures then market makers will intervene to reduce that premium or discount. As I say in the article I believe the technical analysis of the ETPs themselves doesn’t make sense to me. Supply & demand for VIX futures and SPX options ultimately ends up setting prices.

Hello Vance, thanks for the great analysis, well done. I only wish I had read it before I started jumping into this space! Looking at what TVIX has done over the last 30 days, I have continued to buy at lower and lower prices and am holding for the moment. Not working out the best for me right now… any thoughts on TVIX popping with the new fed chair or is it time to get out and play the day trade game on this only before we keep racing to zero (or the next reverse split)?

Hi Steve, Unfortunately being successful owning TVIX requires excellent timing. If you hold onto to TVIX too long even a big VIX spike won’t get you back to your initial investment. My opinion is that the Fed chair issue is not going to impact the markets much. Overall holding TVIX short term might pay off, but more likely you will effectively lose your entire investment. If you’re not ok with losing the whole thing then consider getting out and saving what you can.

Thank for the quick response Vance. Always learning something, sometimes more painfully than others :).

It seems that Yahoo Finance hasn’t been updating ^TVIX-IV since June. Any idea where we can look at the latest? I’d imagine APs are still acting as market makers to keep TVIX in-line with some IV value, right?

https://finance.yahoo.com/quote/%5Etvix-iv

Hi John, Most broker software packages include IV quotes if you know where to look. Schwab is $.iv (.e.,g $TVIX.IV) Fidelity is TVIX/IV you might have to call to find out what your broker uses. Yes, the APs are still at it. Right now 1:30pm ET 25Oct17 IV is 10.44 midprice is 10.52 so tracking error is 0.77%

Vance

Vance,

Thank you very much! I’m with Scottrade, will see if I can find their quotes.

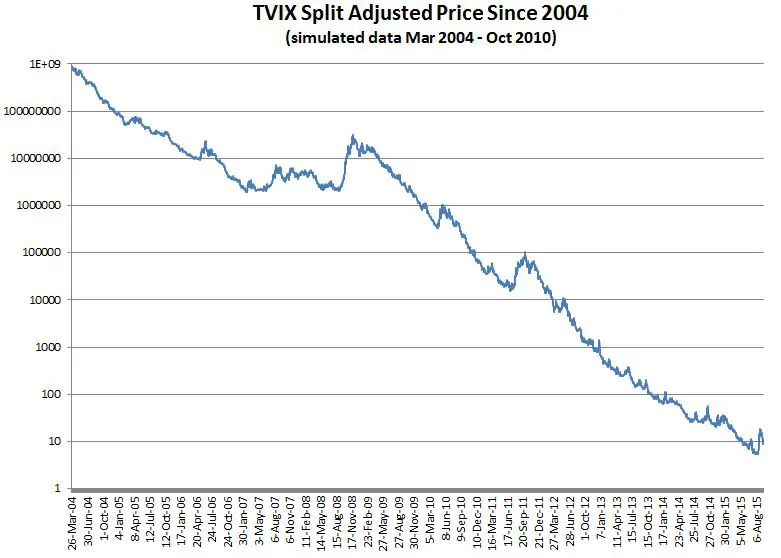

Hello, Vance, thank you for the great analysis over TVIX. If I am seeing correctly, the price level in 2010 was around 28 million, which rapidly declined to 4 million, then back up to 27 million. From then it was going down to this date. I am not sure if I understand these wild price swings correctly. Under what circumstances did these happen?

Thank you.

First of all it’s important to realize that TVIX never traded at those levels. The prices on the chart are reverse split adjusted. The most you could expect UVXY to spike would be around a factor of 8 or 9 with a 2008 style bear market. In that time frame TVIX was probably trading around $2/ share.

The wild price swings up were due to periods of volatility both in 2010 and 2011 where the VIX spiked up hard and stayed there for a while. After the fear wears off the VIX futures go into a configuration called contrango, where the longer dated futures get more and more expensive. This configuration drags down TVIX’s price in the range of 10% per month–hence the long term decline.

Best Regards,

Vance

Hello Vance

I have been researching these sort of VIX ETF’s and was intrigued with your post. After reading a lot of articles I understand that these intruments are not buy and hold types. However, with regards to timing and the SP 500 bubble we are witnessing these days, say hypothetically if the index comes crashing down, would there be a chance of TVIX or UVXY climbing to $5000 or $10,000 levels for a few days before it gets readjusted and the gap is closed to the underlying index.

I would assume when the panic sell ends and bear market is confirmed, VIX would settle down and consequently TVIX an UVXY would fall back to $10 levels we see today.

Your insight is greatly appreciated.

Thanks

Hi SilverShehz,

If we have a 2008 style bear market the 2X longs could go up around 15X, so UVXY could go up to around $150 per share. These 2X ETPs track their indexes quite well so there won’t be any huge gaps to profit from.

Vance

Vance – Congratulations on an excellent website. Your analysis is very insightful and detailed, yet written in plain language accessible to aspiring traders at all levels. Keep up the great work.

Now, about the 2012 TVIX share creation issue, I have been thinking about how an average retail investor could have anticipated it. In any case, is it possible that some of the VIX ETF’s out there might not face such an issue and it is restricted to ETN’s alone? Thanks.

Both ETFs and ETNs can have share creation problems. The most common reason for it is commodity restrictions on position sizes (e.g, so you don’t corner the market on some commodity). With volatility exchange traded products I would say that the ETNs are more likely to have the issue because their business model likely requires non-exchange traded products like variance swaps to be available at reasonable prices. If these swaps get expensive then the ETNs might lose money hedging the product or be exposed to excessive risk. The ETFs just need liquid VIX futures–and that seems to be the case even during pretty stressful market situations. I doubt there will be a repeat of the TVIX fiasco, Credit Suisse has had multiple opportunities to kill TVIX by letting it fade to zero, but they keep reverse splitting it–so it must be worth the risk for them.

I wonder if TVIX is going to go up tomorrow. Brexit vote for leave!? I put in 1000 shares at 2.2 let’s see.

It was up….u r lucky man!

Thanks for the post. Which would have been the maximum spike? it seems something like 10x, in ’08-’09

What would have been the spike in ’87?

I read in Vix and more that the VXO index would have gone to 172.

I’m shorting it with a very small position, trying to figure wich would e the maximum prudent position

Very interesting post. Shorting TVIX or UVXY is scary because of the upward spikes, but what do you think about buying puts? Looking at that chart, it seems that if you buy puts after a big spike you should be able to make good money without so much emotional strain.

Options arent traded on TVIX, but they are on UVXY