Long term charts of 2X UVIX, 1.5X UVXY, or VXX suggest they are perfect candidates for shorting, but there are risks you should be aware of and alternatives to consider.

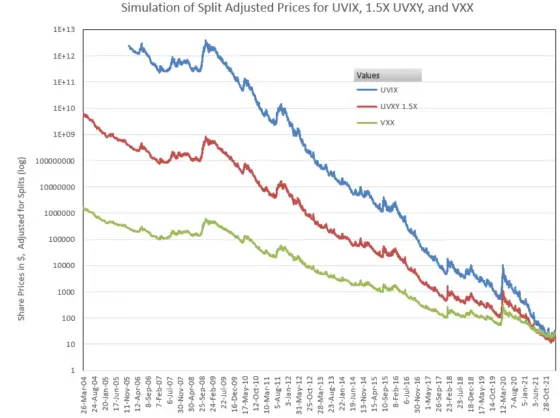

The charts for long volatility Exchange Traded Products (ETP) like Volatility Shares’ UVIX, Barclays’s VXX, and ProShares’ 1.5X levered UVXY are astonishing.

I’m not aware of any other widely available securities that have declined like these.

Two questions come to mind:

- Why would anyone invest in these perennial losers?

- Why doesn’t everyone on the planet short these funds?

It turns out that there are reasonable reasons to buy these funds, and some people make money doing it. And a lot of people short these funds; it’s a crowded trade—to the point where it’s sometimes not possible to borrow the shares to short them.

It’s not easy money either way.

Risks of a Short Position

- Unlike a short position, in most equities fear is not your friend when you are short a volatility fund. When the market gets scared, the equity declines are scary, deep, and fast—and volatility spikes up dramatically.

- One characteristic of a short position is that its leverage moves against you if you’re wrong. When you first open a short position, a 10% gain in the stock you shorted will cost you 10% of your position’s value, but the next 10% gain in the security will increase your loss by 12.2%. This increase in leverage increases rapidly if the security moves strongly against you. See this post for more information on this phenomenon.

- Typically, 75%+ of the time, the prices of long volatility funds like VXX, UVXY, of UVIX are battered by contango, but when the market tanks they turn into beasts. First of all, the VIX futures that these funds are based on spike up, second, the VIX future’s term structure goes into a configuration called backwardation—which boosts the ETP’s returns, and leveraged funds often experience a compounding effect that boosts their returns past their benchmark leverage levels.

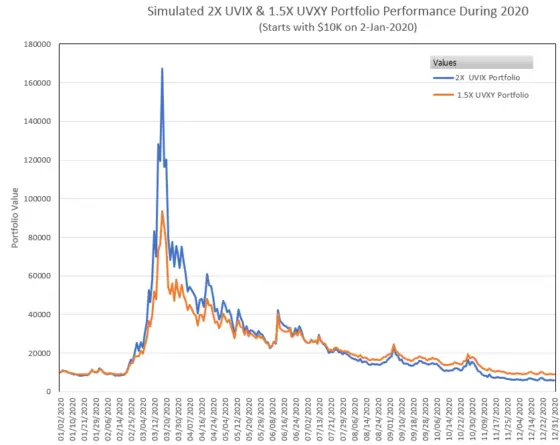

- Long volatility funds have not existed all that long, the first one was introduced in 2009, so we don’t have actual data for the earlier bear markets, but we do have historical data for the 2011 correction, where UVXY’s value went up 550% in a few months (it was 2X leveraged at that point in time). In my simulation of UVXY’s 1.5X leveraged prices that goes back to 2004, I show that the prices of UVXY would have gone up 5.5X in the 2008/2009 crash. Recently, during the Feb/Mar 2020 Covid crash, 1.5X UVXY went up over 10X, and simulated 2X UVIX would have gone up 20x.

Now you can see why some people are interested in going long with these funds.

- In addition to the risks of typical market corrections and bear markets, a short volatility position is also vulnerable to a Black Swan-type event. A major geopolitical event, natural disaster, or terrorist attack could cause a very large, essentially instantaneous jump, in the volatility funds. The record one-day VIX jump so far was a 116% jump in February 2018, but in this post, I postulate that even bigger one-day jumps in the VIX are not out of the question. The VIX futures that underlie the volatility ETPs don’t track the VIX moves directly, typically the mix of futures used moves around 45% of the VIX’s percentage move for the 1X funds, but with the 2X leveraged funds that still gives a 90% daily jump in their prices. On February 5th, 2018 the VIX futures jumped almost the same amount as the VIX, 96% vs 116%—resulting in the termination of Credit Suisse -1X XIV, the deleveraging of SVXY down to a -0.5X fund, and deleveraging of UVXY down to a 1.5X fund. If an event like this happens when the market is closed, there will be no chance for protective measures like stop-loss orders to execute. Even if the event happened during market hours, conditions would be chaotic, and the market would likely shut down quickly.

If I haven’t managed to scare you off by now, the next section discusses the specifics of initiating a short trade.

The Trade

- These securities are always in the “hard to borrow” category, so it’s very likely at least a phone call to your broker will be required to create a short position. It’s also very likely you’ll have to pay an ongoing fee to borrow the shares. Plan on the annualized fee being at 3% for the non-leveraged VXX.

- You’ll need to have margin capability set up in a taxable account. Short selling is not allowed in retirement accounts such as IRAs or 401Ks.

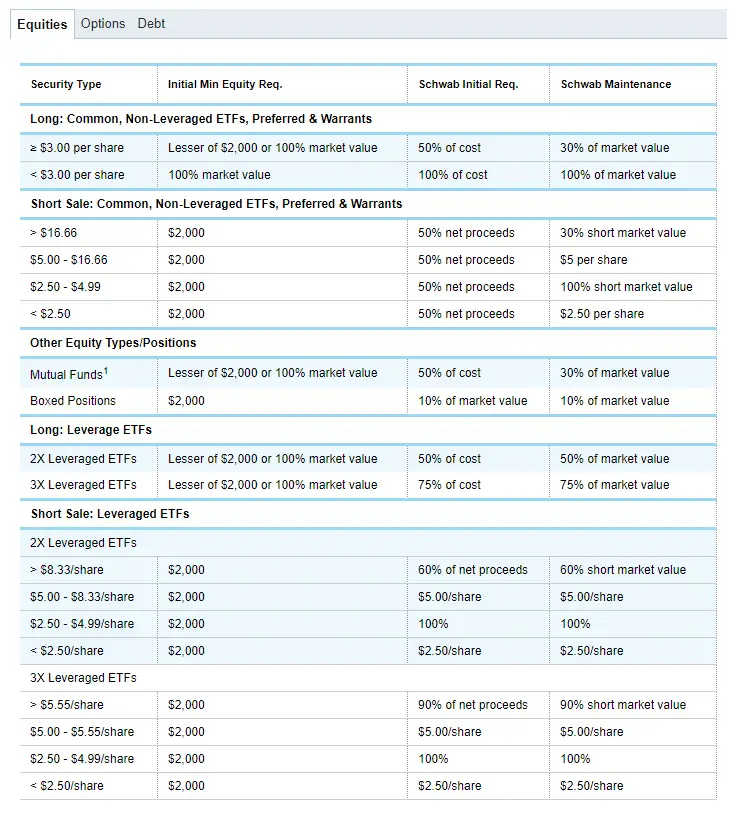

- You’ll need extra cash / marginable securities in your account as margin. There are two different amounts required (which can vary by broker and by security), one to initiate the trade and another to maintain your position. The initial percentage will always be greater than or equal to the maintenance position. Leveraged funds like UVXY and UVIX may require extra margin. The chart below shows Charles Schwab’s requirements for shorting ETFs as of 22-Feb-2019.

- If your trade moves against you to the point that you don’t meet the maintenance requirements, you’ll get a margin call from your broker. Not a fun thing. You have two choices at that point, either add more money / marginable securities to your account, or reduce your short position by buying back some of the security. Don’t expect your broker to be patient.

Managing a Short Position

- If you hold a short position, it’s critical that you have an exit plan. A few people might have a small enough position and enough margin to weather even the darkest bear markets, but most people won’t have the capital or the temperament to hang in there. Emotionally it is very difficult to close out a short volatility position with a large loss. Clearly, your timing has been bad and there’s the near certainty that eventually contango will wear these funds back to levels that would be profitable for you. On the other hand, not having an exit plan raises the very real possibility that your broker will be the one closing out your position, not you, likely at the worst possible time.

- One protective strategy would be to buy out-of-the-money calls at strike prices much higher than the current trading value of the securities. That way you can limit or mitigate your maximum loss, even during a Black Swan. Essentially you’re buying an insurance policy with a high deductible. It wouldn’t be cheap because the options would likely be expensive and usually expire worthless, but the peace of mind might very well be worth the cost.

- One harsh reality of a short position is that while you are exposed to potentially very large losses, the best case profit you can realize from your initial position is limited to 100%. For example, if you sell short $1000 worth of VXX your maximum profit can’t be more than $1000 because VXX can’t drop below zero. And even with the ravages of contango, VXX’s split-adjusted price will never get all the way to zero. As a shorted security drops in value, the leverage of your position drops also, eventually approaching zero.

- If your short has been successful, at some point you’ll need to short additional shares to get your leverage and additional profit potential back up. I quantify this leverage with a simple formula: Leverage = P/Po where P is the current price and Po is the price you initially shorted at. Let’s say you are comfortable with a leverage factor between 1 and 0.7. If it drops to .7 then you would short enough shares to bring your leverage back to 1. So if you were initially short 100 shares at $10, you have a maximum profit potential of $1000 at that point… If the price has dropped to $7, then your maximum additional profit has dropped to $700 and your leverage has dropped to 0.7. To get your leverage and additional profit potential back to 1.0 and $1000 you need to short an additional $300 worth of shares (~43 shares).

Alternatives to a Short Position

There are some alternative strategies that address some of the risks and restrictions of taking a short position. Of course, they introduce their own limitations, risks, and restrictions.

- Volatility Shares’ -1X SVIX and ProShares’s -0.5X SVXY are inverse volatility ETPs that avoid the variable leverage and unconstrained loss aspects of a short position and are allowed in retirement accounts. In exchange for solving those problems, you pick up path dependency and volatility drag. See these posts: How Does SVIX Work?, How Does SVXY Work?, and Ten Questions About Short Selling for more information.

- Options are available for SVXY, SVIX, UVXY, UVIX, and VXX. Instead of going short on these ETPs, you can buy or sell puts and calls. Buying puts eliminates the potential for an unconstrained loss, but the premiums are steep. No easy money here either. One additional caveat is, because of their frequent reverse splits longer-term options on the long funds will likely become “adjusted” options. The number of shares they control changes and they track a modified version of the security price. This option adjustment happens in conjunction with the reverse splits. Theoretically, no value is lost, but by all accounts, these options become less liquid and the bid/ask prices widen. These options are American style, so with long positions, you’ll always be able to exercise them, but caution is warranted. For more on this see UVXY Reverse Splits.

Seller Beware

I’ve had direct contact with people that have lost hundreds of thousands of dollars on both sides of these trades. Honestly, I think considerably more is lost on the long side, but the blowouts on the short side tend to be quick and vicious. Most rookies get greedy, and risk being blown out by even a mild correction. If you can manage to hold (and rebalance) your short position long enough it’s a rational trade—but that’s a big if.

Instead of shorting shares, would shorting an ATM call and longing an ATM put work? The risks I see is that these are defined expiry trades, and you might bear some vega risk since UVXY calls are generally priced higher than puts due to vol skew. However, it seems like delta hedging these with some shares over the expiration of the trade could hedge off the risk for the most part. Thoughts?

Thanks for this site and articles like these.

There seem to be two good ways to protect oneself. First and simplest is position sizing. I calculate my position size based on

(a) what I’m using for margin collateral — I assume broad US market equities can drop 60% from the most recent ATH.

(b) the state of VIX futures

(c) margin requirements — at Fidelity it’s 200% for these products.

(d) some room of error — bake in another 10% for error.

Therefore right now, if using shares of SPY as collateral, I assume SPY can drop to 192 (from a high of 480), which is about 46% of its current level. VIX 1 month futures’ current level at the time of this post is about 20. So VXX could go up about 4x (or a bit more with beta slippage). For a 100k account, I might short (0.46 / 4 / 2 * 0.9) = 5% of the account, and use the proceeds to buy more equities.

This strategy works particularly well in a bear market because there’s more room for VIX to fall (profit!), there’s less room for it to rise (less risk), there’s less room for equities to keep falling (less risk), while the proceeds are used to buy equities on the cheap. In a strong bull market such as 2017 or 2019 it would have been higher risk (therefore a smaller position size) and less reward.

The other option besides position size is to buy calls on what you’re shorting, which allows a larger position size but has a lot more room for error in execution and can be expensive to keep rolling when volatility rises but not high enough to let you close out your short by exercising the call.

VXX Leap Puts is a very high vega trade. And it is to my understanding when the VX futures are in huge backwardation when the market crashes say Mar 2020 – Front month VX futures was like 60-70.

VXX Leap Puts were so high premium priced, in volatility that even if you bought it for direction OTM, LEAP like 1 year+, you may lose more on the vega than gaining on delta.

I noticed on certain Vol spikes that are not huge market corrections, these are great opportunities to buy VXX LEAP Puts OTM or more aggressively shorter term 6 months to 12 months, assuming you don’t get caught with VX1 / VIX continuing to rise and spike.

What are some ways to mitigate this?

1) Wait for Volatility to calm down in the markets, like backwardation is moving towards contango?

2) Instead of pure VXX Leap Puts, VXX LEAP Put Spread so that you sell some high volatility?

3) Sell Credit Call Spreads to finance?

4) Sell VXX Short Term Puts to finance the LEAP VXX Puts to take advantage of Vx1 term structure moving back into contango?

I am playing around with selling VXX weekly put spreads 2% OTM to hedge my neutral condor strategy.

I just started adding this to my overall neutralish option strategy, so we’ll see…it is a bit nerve wracking to see VXX losing value, heading toward my strike price even as the market is flat or even retraces a tiny bit, but if I can see it’s on track for it’s normal 2% per week decay, I can keep my sanity.

Since I’m doing a weekly strategy, I only have to guess the likely decay rate for the next week.

Hi gb, Not clear to me how much of a hedge your put spreads will provide. Their payout probably doesn’t help that much if your condor goes wrong. The put spread is typically more of an income strategy because the best case is pretty limited. Having skin the game does make those VXX plunges scary. It can drop more than 2% pretty easily.

Is there advance notice of a reverse split on VXX? If there is, how would I be able to follow that notification system?

Jim

Hi Jim, They can be hard to find, but there are press releases that give a couple weeks notice. I use google alerts with a string like “VXX split” to find these. The OCC always issues memos relating to the impact of splits on options. https://www.theocc.com/webapps/infomemos They also offer a RSS feed that can be triggered by contract adjustments, so that should work if you’re willing to sift through all the non-VXX related stuff that goes on.

Vance

Thanks Vance, I set a google alert. We will see how that works. My VXX trades are rarely longer than 30 days. Because of the confusion of the VXX splits I would rather just pass on the trade if I know the split is coming. At the current level, I feel a split must be coming soon.

Jim

Barclays announced a 1 for 4 reverse split on VXX for Aug 23.

http://www.businesswire.com/news/home/20170809006219/en/Barclays-Bank-PLC-Announces-Reverse-Split-iPath%C2%AE

Jim

Thanks, Jim! Quite a bit sooner than I predicted (December). The contango has been brutal.

Vance

I have read your articles and ideation on this topic with much interest. As far as I understand, it seems like these instruments look like a sure way to make money, but as you argued that is rarely the case, as people often lose thousands of dollars. The reasons for which are:

1) Position sizing, the market spikes and thus goes significantly against the short trader. While there is no data for the 08 crash you mentioned that there would have been a 6x (600%) spike on VXX and 15x (1500%).

2) If there short goes against you, it leverage increases as prices go higher whereas if the short works – the potential profit percentage drops and is limited to 100%, whereas the theoretical loss is unlimited.

I would like to challenge a couple of these ideas, mayhaps because of my limited understanding and ultracrepidarianism. This thinking is based on just trading the shares, not options.

a) Theoretical Profit is limited to 100% and the percentage gains decrease for the trade over time.

Then why not create a system that targets relatively small profit targets, e.g. 4% – 20% range, before the law of diminishing returns comes into effect? I.e. short the trade with a short small predetermined profit target and close it. As you stated the contango effect will batter the instrument down over time and thus, over a long enough time period the trade will close at profit. Additionally the smaller the target trade, the sooner it will close.

b) The leverage effect if the market spikes.

Based on the chart the biggest from a previous low on VXX was 207% between July and November of 2011. And I think you mentioned that sims showed it would have gone up 600% during the 08 crash. OK, so then why not consider the following:

*if the maximum possible jump is expected to be 600%, then base the trade size on that.

* e.g. if my total investment account is $15,000 then allocate $3000 as a margin of safety, divide the rest ($12K) that by the maximum expected spike 12,000 / 6 = $2000. Thus only short $2000 of the whole account.

* e.g. buy 200 VXX @ $10.00 = $2000. If the market spikes 600%, to $60 per share = $12,000

Does using this methodology not address the leverage spike issue?

Additionally:

*Add an additional $1K to the account and recalculating trade size every 12 months.

*If the market does spike, just keep the trade open and wait it out, volatility can only last x amount of years. I am cognizant that there has been extended volatility in the distant past, e.g. 1929-, but I assume the government has gotten better at reducing such extended volatility over long periods as our understanding of economics has improved.

The thing is shorting with 10% of totally investing and paying round 8% for shorting fee, it is may be not worth to do it.

But I agree with your rebalance strategy.

I have been using this methodology since Oct 2016, so far I have closed 19 trades all in profit. Its been working as expect and I am super-happy about it.

“The thing is shorting with 10% of totally investing and paying round 8% for shorting fee, it is may be not worth to do it.

But I agree with your rebalance strategy.”

About the investment of only 10% of the account, yes agreed that is an issue. So, what I have been doing is to only invest a small amount of the account and will hold out for a bike spike, and then only buy on that big spike.

I no longer trade VXX that much, preferring XIV instead, as it can only fall 100%, but VXX can spike 600%, because the 600% worst case jump was huge, it reduced my investment size significantly. With XIV, I can no increase my investment size a ton.

The reason I am waiting for a big spike down, while also trading in an out is, if I buy at $100, I can get 1 share per $100, but if I get in on a bike spike down to $20, I can fives times more shares.

The caveat these spikes are far and few apart, so I am using both strategies, with some careful math.

I have read your articles and ideation on this topic with much interest. As far as I understand, it seems like these instruments look like a sure way to make money, but as you argued that is rarely the case, as people often lose thousands of dollars. The reasons for which are:

1) Position sizing, the market spikes and thus goes significantly against the short trader. While there is no data for the 08 crash you mentioned that there would have been a 6x (600%) spike on VXX and 15x (1500%).

2) If there short goes against you, it leverage increases as prices go higher whereas if the short works – the potential profit percentage drops and is limited to 100%, whereas the theoretical loss is unlimited.

I would like to challenge a couple of these ideas, mayhaps because of my limited understanding and ultracrepidarianism. This thinking is based on just trading the shares, not options.

a) Theoretical Profit is limited to 100% and the percentage gains decrease for the trade over time.

Then why not create a system that targets relatively small profit targets, e.g. 4% – 20% range, before the law of diminishing returns comes into effect? I.e. short the trade with a short small predetermined profit target and close it. As you stated the contango effect will batter the instrument down over time and thus, over a long enough time period the trade will close at profit. Additionally the smaller the target trade, the sooner it will close.

b) The leverage effect if the market spikes.

Based on the chart the biggest from a previous low on VXX was 207% between July and November of 2011. And I think you mentioned that sims showed it would have gone up 600% during the 08 crash. OK, so then why not consider the following:

*if the maximum possible jump is expected to be 600%, then base the trade size on that.

* e.g. if my total investment account is $15,000 then allocate $3000 as a margin of safety, divide the rest ($12K) that by the maximum expected spike 12,000 / 6 = $2000. Thus only short $2000 of the whole account.

* e.g. buy 200 VXX @ $10.00 = $2000. If the market spikes 600%, to $60 per share = $12,000

Does using this methodology not address the leverage spike issue?

Additionally:

*Add an additional $1K to the account and recalculating trade size every 12 months.

*If the market does spike, just keep the trade open and wait it out, volatility can only last x amount of years. I am cognizant that there has been extended volatility in the distant past, e.g. 1929-, but I assume the government has gotten better at reducing such extended volatility over long periods as our understanding of economics has improved.

I see a lot of ideas involving shorting VXX. Isn’t it better to buy XIV?

Thanks!

Hi Don, It really depends on how the market is acting. If volatility is volatile, with a lot of VIX movement up and down, then shorting VXX would be better (with periodic rebalancing to keep the leverage ratios in line). If volatility is relatively tame or trending, then XIV is better.

Hi Vance,

I recall an old blog from 2012 where you mentioned a strategy that uses ZIV, medium-term inverse volatility fund combined with the VIX/VXV ratio, to switch between fully invested and cash. Is that strategy still valid?

Thanks!

Hi Roiven, That strategy stopped working in 2014. Don’t know why. Updated simulation results below.

https://www.sixfigureinvesting.com/wp-content/uploads/2017/04/ZIV-simple-ratio-3Mar17.jpg

Hi Vance,

Thank you for the great post.

Any thoughts on MRPAX (Measured Risk Strategy Fund) as a long term way to short the vol ETPs?

Republicans spent eight years lying about the debt ceiling and now they control the government and have to raise it. Will they lie again and will their supporters see the blatant hypocrisy?

Trump is eating through all the cash President Obama stored up for the debt ceiling fight. In a few days, the money could be gone. While Treasury is already taking action, there’s no sign of action in congress and the debt ceiling will be hit in a few days.

If you think republicans are utterly incompetent you’ll buy UVXY now and wait for republicans to default on the debt.

hahahhah that s a smart trade…. wait for the republican to default, good way to time the market hahahahah

Obama kept cash hordes! Good to know. How’s that uvxy working for you?

Hi there,

I am constantly shorting VXX and making profits. I do never let the short position to be greater than my equity and getting in only on price ups. The thing that concerns me is the enormous price appreciation of the VXX. As I have observed these price increase does not occur in the single day but it rises gradually (in the most cases) to be able to wipe out the equity. What do you think would be the indicating factor suggesting that it is time to get out of the short and wait for another opportunity to be back in? Currently I am using volatility stop on daily chart, when it provides with the buy signal, I do exit the trade, when it suggest selling, I do re-enter. What do you think?

Hi Vykintas, I don’t have any great answers here. Other than upcoming events with high impact / uncertainty it can be very difficult to anticipate volatility spikes.

Perhaps research the strategy of buying some LEAP PUTS on SPY when the VIX gets really cheap as a hedge or maintain some ratio of SPY puts to VXX short? LEAPS because of the implied volatility decay and try to roll the option everytime you have 3 months to expiry.

I’m not really sure the right ratio or how to manage and it would depend on your position size and risk tolerance and strike price and other factors. But at least if there was an enormous event that rocked the SPY downward and the VXX upward you could do okay. The one negative variable would be the tendency for rising vix and rising market before tops like in 2006-2007. You’d get hit from both eroding premium and rising vix there and it would be even worse if a crash followed and you hadn’t bought the SPY put or had bought it from much lower prices..

Hi Optionbets, About using options to hedge a short VXX position: My concern is that in a black swan event, when VXX shoots to the sky, SPY may not move that much, and those puts may be not a good hedge. Have you thought about buying deep out-of-money calls on VXX or UVXY instead?

But if the VIX rises the extrinsic value of the S&P will still rise. VXX and UVXY suffer badly when they are in contango which is most of the time, so unless you can time it or only trade it when VIX enters contango and protect against things getting worse and black swan not appearing from complacent markets I suppose that is one option.

I prefer to buy options when implied volatility is cheap. The implied volatility OF instruments that track the implied volatility is usually going to rise expecting some kind of mean reversion which makes things difficult…

I think buying VXX puts is okay if you can grab a spike and expect contango to resume…

When VIX is cheap I want to play more options and sell my XIV shares or VXX puts to fund those trades.

Just me personally not a recommendation to buy or sel and other standard disclaimer stuff.

This makes sense, but it is hard to estimate the delta of such hedge. The hedge is simpler with VXX calls.

Say, I am short 1000 shares of VXX. I can buy the same amount of very cheap VXX calls with the strike of 30.

I will still need enough equity in the account to survive if VXX goes up to 30. After that, the delta of the call option will be almost 1, and I am fully hedged.

Both VXX and its calls will loose their value as a result of contango, but as long as the number of options matches the number of shares, I will be safe even if VIX (or VXX) goes totally through the roof.

What do you think?

Is it not feasible to hold those positions long term, meaning a couple of months to mayhaps a year (who knows?). Eventually I also think that it is a near certainty that in the long term, the price will again drop lower to that level. After all the trend is for volatility to spike over short (relatively) periods of time versus a long term.

Would love to know what you think

Vance. You mention XIV being terminated in a bad enough correction. Can you clarify how that would work?

The XIV prospectus defines a termination event if within a single day the fund loses 80% or more of it’s value from the previous close. This could occur if the 1st and 2nd month VIX futures went up about that amount in a day. Since the 1st month is typically more volatile than the 2nd month futures the % of XIV allocated to each of the month’s futures would make a difference. The amount in the fund left after the end of the day would be refunded to the shareholder. That amount would not be negative, but it could be more or less than 20% of the previous day’s closing value.

Dear Vance,

One year ago, I bought VXX, VXZ and TWM because I was certain that the market is going down (Total 60k$). Since than, I lost 80%.

My question is – assuming that I have ‘long breath’, would you recomment to hold and wait?

Hi Ron, Sorry to hear that you are in a loss situation. First of all I cannot make recommendations because I am not a registered investment advisor. I will however make some observations that might help you make your decision. Being down 80% it would take a very major correction or a bear market for these long volatility funds to recover back to your break even point. That volatility event could happen tomorrow, but as you’ve discovered market direction is very hard to predict. You will have to weigh the emotional risk of selling and then having the possibility of the market correction then occurring soon after vs the likelyhood that you will eventually lose almost all of your current investment if you just hold on. $12K is still a significant amount, so admitting that your timing was bad and moving on to something else is not a bad move. For some admitting bad timing and selling the position will be an incredible emotional relief, others might torture themselves if they do that and the market does crash. You can look within yourself to see what is best for you and your family.

Thank you Vance.

Ron, I trade volatility frequently so if you can use a hand using these instruments for their best purpose and potential let me know.

Hi Vance: I am wondering how fast can the jump of VIX be in case of a black swan event happens? It jumps in seconds? in several minutes? or jump step by step in one day? If VIX increase by 50% in 1 sec or by market open, it’s difficult to hedge this risk

Hi Sussy, Worst case situation is probably an overnight event that panics the markets, but something not so dire that the markets don’t open. The biggest one day spike, greater than 50%, happened 27-Feb-2007. On that day the VIX opened at 12.12, climbed up to 19.01 and closed at 18.31. Closing out/opening positions in market conditions like this would be nightmarish. The spreads will be huge if circuit breakers haven’t triggered. VIX ETP products are driven by percentage changes, not absolute levels–so a relatively benign event, slightly worse than the 27-Feb-2007 could terminate short volatility funds like XIV & SVXY. For me the bottom line is that you should size your positions such that you can live with a black swan even–assuming that you won’t be able to do anything with your position the day of the event.

I just started a small position on UVXY. I plan on adding to this position as I believe the markets are going to be very volatile this year. I did some research into investing in a fund correlated to the VIX, but I noticed in every blog I read, that I shouldn’t hold this fund more than a day or 2. Am I investing in the wrong product if I have a 2 to 3 month investment horizon because I believe February will be a volatile month? Should I not add to my popinion if I have strong conviction that volatility will spike? I need some help, not really understanding this whole VIX strategy. Thanks anyone

HI Anthony, The trouble with UVXY is that if your timing isn’t perfect you will losing significant amounts of money. If the market doesn’t have a volatility spike when you expect it you will likely lose 8% of your investment PER WEEK. If you aren’t set on making huge gains on your investment you might look at XVZ or BSWN. Both of these will do well in a big market turndown (but not the big multiples like UVXY), but their erosion rates are much lower during quiet times.

How do You guesstimate roll yield/ decay at 8% a week..ive held TVIX longer and did not lose 32% a month..site an example..

The vix futures market has been sideways even though in contango TVIX position is not losing 8% a week

Anthony, I trade volatility frequently so if you can use a hand using these instruments for their best purpose and potential let me know.

Hello, thank you for the valuable information. Is there any tax implications at the year end trading UVXY? I read few articles about it, but not very clear what is the tax impact end of the year. if you can give me example like if i make $100 end of the year as a short term gain how much tax do i pay. Thank you.

My understanding is that 60% of the $100 gain would be treated as long term gain (usually taxed at a lower tax rate), and that $40 would be taxed as short term capital gains.

Thank you for the reply, Vance. I’ve scottrade brokerage account and my profit on UVXY trade is shown under short term capital gains. will it be shown correctly in my tax statement ? how can i make sure my accountant file the tax correctly. Cause as per trading rule for any brokerage ac, anything hold for less than a year is short term gain/loss.

Hi Eric,

In the UVXY webpage http://www.proshares.com/funds/uvxy.html it specifies (in the fine print at the bottom) that this fund issues a K-1 form. My understanding is that UVXY will be considered under the 1256 contracts tax rules which don’t follow the same rules as equity trades. Of course I might be wrong, but ProShares owes you a K-1 form which your accountant can use to figure your taxes.

yes Vance, out of the money. Some have to be rewritten if they’re too close.

Hi Vance, I’ve been shorting SVXY and VXX and writing puts for the last 16 months. I’m down on my SVXY and up less on VXX but my puts have given me a 15% return overall for 2016. It’s the perfect trade except for the black swan event which will come sometime next year. Powder dry

HI Energy11, So you’re writing puts on both SVXY & VXX? Are the VXX puts significantly out of the money? Seems like otherwise they would have gone into the money a lot this year.

Hey Vance, at IB right now I see UVXY has borrowing costs of ~8% but TVIX has borrowing costs of ~3%. Do you know if this is normal to have such a large difference in borrowing costs for two almost identical ETPs?

Hi Luke, I don’t know the history on borrowing costs. I suspect the difference is just due to supply and demand. Because TVIX historically spent so much time trading below a dollar I think UVXY has become more popular for shorting. As far as differences I don’t see any substantive ones.

shorting at all-time historical lows of volatility would be too dangerous, no? vix 11.60 and hasnt really been lower than 10.8 as far as I know…

Certainly not an ideal time. Historically volatility picks up in January. However, now might be a good time to pick up protective long term OTM calls (e.g, S60) if you know you’re going to go short in the near future. Historic low for VIX is around 9.

OTM calls with $60 strike? I looked at last 3 years and VIX has been 10.3 at the lowest and 53.3 at its absolute height. They don’t even offer $60 strike… any other suggestion?

Sorry, since a direct short of VIX isn’t possible I was assuming you were talking about VXX. 16-June-17 VXX S50 calls are at $1.18. This would limit losses on a VXX short (assuming $25 price) to 100%

danke. makes perfect sense now.

Over the last six or seven months, I’ve bought a lot of VXX and UVXY underlying shares because the market seems to be getting really complacent. Now my positions are down about 60%. I know at some point we’re going to have a spike, but I am getting nervous since my basis price for VXX is about $70. What do you think about selling calls against this vs just waiting until the next time the market panics? Most of my accounts are sitting in cash outside of these VIX ETF positions.

Hi Don, Without a market correction VXX & UVXY will have average monthly decay rates of around 7% and 20% respectively. https://www.sixfigureinvesting.com/2016/06/monthly-yearly-decay-rates-contago-losses-vxx-uvxy-vxx-vixy/ Without giving up most of your upside selling calls won’t reduce that decay rate by much. In my opinion holding these long vol funds for the inevitable vol spike is generally a losing strategy unless your timing is really good. The decay just kills you. You might consider the hedged vol funds XVZ and BSWN. They won’t have the spectacular returns that a VXX or UVXY would provide, but they’re a lot more likely to preserve your capitial until the spike actually happens.

Vance

What about buying some puts on VXX assuming VVIX is low?

Thanks!

Thanks Vance,

I looked up the charts for BSWN and XVZ, and the volumes are extremely low, zero on some days unless I’m doing someting wrong when I generate the chart. Are the volumes really that low for these?

Thanks,

Don

These funds have very low trading volumes. They are liquid because their underlying is liquid. These ETPs by definition don’t do anything until the market crashes, so they don’t attract much attention. Posts related to these funds:

https://www.sixfigureinvesting.com/2016/08/how-do-velocityshares-bswn-lsvx-xivh-work/

https://www.sixfigureinvesting.com/2015/08/determining-liquidity-of-low-volume-etf-etn/

https://www.sixfigureinvesting.com/2015/08/trading-low-volume-exchange-traded-products/

Hi Vance,

Am I correct that VXX and XIV are inversely related, so if one goes up 1% in a day, the other one drops 1%? If that is the case, is it possible to setup a “straddle effect” by buying the same dollar amount of the underlying VXX and XIV when we anticipate a medium to large change in volatility but aren’t sure which way? Because of compounding interest, the leg that increases in value will move in larger and larger dollar amounts as the price rises than the losing one will lose. For instance, a $10,000 investment in each stock with 5% (exaggerated) daily increases in XIV and decreases in VXX, the XIV value will increase $10,500, $11,025, $11,576, but $10,000 in VXX will decrease to $9,500, $9,025, 8,574. The net value of the $20,000 portfolio would then be about $20,150. This is true regardless which way the VXX and XIV move. Am I missing something here?

Thanks,

Don

Hi Don, VXX and XIV are only inversely related on a daily basis. For periods longer than a day it gets much more complicated. If volatility is high with lots of up and down movement XIV will tend to underperform, if the market is trending up or down then XIV will tend to overperform relative to VXX. For more on this behavior see https://www.sixfigureinvesting.com/2012/10/a-hat-trick-for-inverse-leveraged-volatility-funds/

Why not just short UVXY, but back after a 50% profit, then sell short again? Repeat process throughout the year? Based on a Jan 2016 price of 150 and a current price of 10 this would have worked out beautifully selling and buying after every 50% gain. What am I missing, because I know this is a too good to be true scenario.

Hi Slade, 2016 did not have any volatility spikes to speak of. In the 2011 correction UVXY would have gone up 9X –consider what that would do to your strategy. The big challenge is not getting wiped out when (not if) volatility spikes up.

Assuming a small percentage of your portfolio was/is dedicated to the strategy it wouldn’t wipe you out but be painful for a few months. The trade would have still been close to break even if not profitable by the end of the year. I would be more afraid of an extended bear market vs a quick spike in volatility given suck a quick reversion to the mean. So do you recommend buying XIV on big dips vs shorting UVXY? I’ve looked at buying puts on UVXY but the pricing and delta are obviously not in your favor. Last question, do brokers treat margin calls on these volatility trades because of their reversion tendencies?

Thanks for the quick response, do you offer any volatility trading advice or newsletters I can subscribe to or know of any reputable newsletters with trades on vol? I’m just recently learning the vol trades available and I love your blog, some of what you say is over my head but you provide a ton of great information.

Hi Vance, Can you remind me if there is a chartable ticker and what it is for the index maintained by Dow Jones that UVXY is supposed to track on a daily basis? Something like VXSTVIX? I can’t find it anywhere. Thank you in advance

Hi Phil, UVXY tracks 2X the daily moves of SPVXSP (see https://www.sixfigureinvesting.com/2014/12/volatility-related-indexes-and-tickers/ for links to places where SPVXSP is broadcast). As far as I know you’d have to do the math yourself to get the appropriate 2X version of the index that UVXY tracks.

Thanks for that Vance! Do you know why the weights on the VXX are not straightforward? For example, I would assume that the November futures weight increases by 5% because the roll period is 20 days. But at yesterday’s close the weight is 43% when it should be 45%.

Hi Phil, The mix is managed as a portfolio dollar value, not by the number of futures contracts. For details see https://www.sixfigureinvesting.com/2015/01/how-does-vxx-daily-roll-work/

Ok! Thank you Vance! So with your example the new allocation will be 72 or 72.14 contracts?

Options add a slew of new variables to the mix, but you can control your max loss with them vs shorting the stock. Never have to ask my broker to borrow and I can trade them in an IRA.

The real problem is that if all hell breaks loose (and it might not even take that much to happen), the ETNs might detach from their underlyings and explode. More detail on pp. 22-23 here:

http://static1.squarespace.com/static/5581f17ee4b01f59c2b1513a/t/561dc6f1e4b0b5f8adc9ca2f/1444792049785/Artemis_Q32015_Volatility-and-Prisoners-Dilemma.pdf

Hi Less, Cole’s stuff is entertaining but I don’t buy his doom & gloom. It’s well known that the 2X long and -1X inverse have to rebalance in the same direction (e.g., buy more when volatility goes up). This market, VIX futures is very liquid and is backstopped by the even more liquid SPX options. There are lots of institutions that would love to arb out a premium price in VIX futures relative to the appropriate strip of SPX options. The other dynamic is that there is lots of selling of VIX futures during volatility spikes. Holders are cashing in, trying to beat the inevitable volatility crash that comes later.

— Vance

Hi Vance, found this article (from other your other one); my thoughts exactly to short VXX when vix 30-50 on the (eventual) decline. Also keeping in mind a 15x worst case scenario cash position. However if factoring a 15x VXX spike, the hands down better trade would probably be a SPY long position or long anything assuming the company your buying still exists in that “dooms day” scenario!

Who is “Less”? If you honestly think arbing is going to be the top priority during the next legitimate crash, I have to say I lose some respect for you. This is coming from someone who has been short VXX for the better part of 8 years, BTW.

My point is that if sh!t truly hits the fan, everyone backs away. The price of VXX can go as high as it damn pleases. Nothing to stop it. Shorting VXX is basically selling insurance against a total market meltdown. I’m not sure everyone understands that.

Yes, everyone backs away and things remain thin even at natural objective levels. Fewer-and-fewer of us remember those times, and that’s aside from the recency bias. Thanks for your extremely relevant input about reality.