The CME, a well-respected, USA-regulated futures exchange, has been trading BitCoin futures since December 2017. These futures make it possible to trade on Bitcoin’s value without being exposed to the uncertainties of the mostly unregulated Bitcoin exchanges.

To understand Bitcoin futures you need to recognize, among some other things, that these futures are not in the business of predicting Bitcoin’s price.

Bitcoin Futures are Not Trying to Predict the Future!

It’s reasonable to assume that a product named a future is attempting to predict the future. For Bitcoin futures, this is definitely not what they deliver. The core utility of the futures markets is not predicting the future prices of their product but rather the secure delivery of a product at a known price, quality, and date. If there’s product seasonality (e.g., specific harvest times) or foreseeable shortages/abundances then future prices may reflect that but neither of these factors applies to Bitcoin.

I’m not saying that Bitcoin futures won’t be used by speculators making bets on Bitcoin—they certainly will be— but when you see Bitcoin futures trading higher or lower than the current Bitcoin exchange values (spot value) it’s not a prediction—it’s a reflection of the inner workings of the futures market.

How Are Bitcoin futures prices established?

If you look at the quotes for Bitcoin futures you’ll see at least three things, the expiration code (shorthand for a specific expiration date ) the bid (buy price), and the ask (sell price). If you’re ever confused as to which one to use in your situation it’s easy to sort out—start with the price that’s worse for you.

Important agents interacting with those prices are operating in one of three roles: individual speculator, market maker, or arbitrageur. A key role is market maker—a firm that has agreed to simultaneously act as both a buyer and seller for a specific security. When companies sign up for this role they agree to keep the bid/ask prices relatively close to each other—for example, even if they aren’t keen on selling Bitcoins at the moment they can’t just set the ask price to an outrageous level. The agreed-upon maximum bid/ask ranges might be tied to market conditions (e.g., wider when deemed a “fast market”) and might allow time-outs but in general, the market maker agrees to act as a buffer between supply and demand.

The Market Makers

The existence of market makers (e.g., Virtu Financial) refutes a common assertion about futures—that there‘s always a loser for every winner; that it’s a zero-sum game. It’s true that derivatives like stock options and futures are created in matched pairs—a long and a short contract. If two speculators own those two contracts the profits on one side are offset by losses on the other but market makers are not speculators. In general, they’re not betting on the direction of the market. They act as intermediaries, selling to buyers at the higher ask price and buying from sellers at the lower bid price— collecting the difference.

Market makers are challenged in fast markets—when either buyers or sellers are dominating and prices are moving rapidly. When this happens market makers are obligated to continue quoting bid and ask prices that maintain some semblance of an orderly market. If they start accumulating uncomfortably large net long or short inventories they may start hedging their positions to protect themselves. For example, if they are short Bitcoin futures they can buy Bitcoin futures with different expirations or directly buy Bitcoins to hedge their positions. The hedged portion of the market maker’s portfolio is not sensitive to Bitcoin price movements—their profit/losses on the short side are offset by their long positions.

The market maker’s ability to hedge out their exposure demonstrates that futures aren’t inherently a zero-sum gain. They can accommodate the market and still be profitable—regardless of the market’s direction.

The Arbitrageur

The arbitrageur is hyper-focused on the price difference between the Bitcoin future prices and the actual Bitcoin exchange price (spot price). If those prices differ enough they can lock in risk-free profits. You can imagine how much capital is available if risk-free profits are in the offing…

The arbitrageur very carefully calculates the costs of buying or shorting Bitcoin futures while selling short or buying actual Bitcoins.

These calculations include:

- Time value of money required for margin deposits

- Fees

- Transaction costs (bid/ask spread)

- Contract expiration settlement price risk (Bitcoin futures are cash-settled)

- Borrow costs for shorting Bitcoin if going short

- The amount of profit that their bosses expect from them.

In general, commodity futures arbitrageurs have to account for things like storage costs (e.g. warehouses, silos), insurance (in case the storage facility is robbed or burns down), and seasonal price variations. In the case of Bitcoin, there are no apparent seasonal variations, but the digital equivalent of storage does exist and very likely insurance costs.

Knowing their estimated costs and profit requirements the arbitrageur determines a minimum difference they need between the futures’ prices and the spot price before they will enter the market. They then monitor the price difference between Bitcoin futures and the Bitcoin exchanges and if large enough they act to profit on that gap. For example, if a specific Bitcoin future (e.g., February contract) is trading sufficiently higher than the current Bitcoin exchange price they will short that Bitcoin future and hedge their position by buying Bitcoins on the exchange. At that point, if they have achieved trade prices within their targets, they have locked in a guaranteed profit. They will hold those positions until contract expiration (or until they can cover their short futures and sell Bitcoins at a profit).

They’ll do the complementary transaction if the price of a specific future is enough lower than spot price. They’ll buy futures and short Bitcoins to lock in profits in that case.

Arbitrageurs provide a critical role in futures markets because they’re the adults in the room that keep futures prices attuned to Bitcoin exchange prices. If there are multiple futures providers, they’ll also act to keep the futures from the various exchanges aligned with each other.

If Bitcoin futures prices get too high relative to spot, arbitragers are natural sellers, and if the futures prices get too low they are natural buyers. Their buying and selling actions naturally counteract price distortions between markets. If they’re somehow prevented from acting (e.g., if shorting Bitcoin was forbidden) then the futures market would likely become decoupled from the underlying spot price—not a good thing.

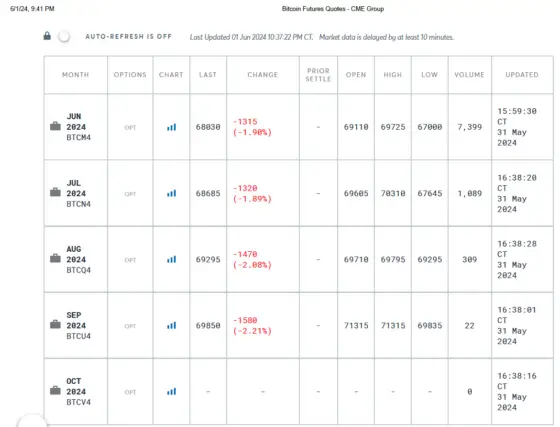

The Term Structure

A key attribute of a futures market is how its contract’s prices vary by expiration date. The succession of futures prices over time is called the “term structure”. If supply is stable (no seasonality or shortages) then typically futures prices will increase with expirations further in the future. This term structure configuration is called “contango” and it accounts for the fact that carry costs (e.g., time value of money) and profit expectations increase with time. Unless there are big changes in interest rates or the way that Bitcoin exchanges work I expect the level of contango in the Bitcoin futures term structure to be small. Bitcoins don’t cost much to hodl (once you have your hardware wallet) and there’s no apparent seasonality. The table below from the CME shows a typical Bitcoin term structure.

CME: Sizes & Settlement

There is only one USA regulated Bitcoin futures exchange in operation, the CME. Initially, the Cboe had Bitcoin futures also but they dropped out early in the game. The standard CME’s contract unit is five Bitcoins, which makes the face/notional value of the contracts quite high, $300K if BTC is at $60K. Larger investors won’t care but this will be an issue for smaller investors, so the CME offers a micro contract also, which has a notional value of one-tenth of a bitcoin. For the CME futures, the settlement price is a complex calculation using an hour of volume-weighted data from multiple exchanges (currently Bitstamp, itBit, Kraken, and GDAX). With the CME’s approach, it will be harder to manipulate the settlement price but it doesn’t give arbitrageurs a physical mechanism to trade their positions.

There’s nothing to prevent people from closing out their contracts before the final settlement but typically there is some premium remaining until the very end.

Unlike many commodity futures, Bitcoin futures are cash settled rather than physically settled. Cash settlement is a relatively new development in futures trading, first introduced in 1981 for Eurodollar futures, that addresses the problem of how to settle futures contracts on things that are difficult/impossible to deliver physically—things like interest rates, large stock indexes (e.g., S&P 500), and volatility indexes (Cboe’s VIX). Physical settlement of futures involves actual shipment/change of ownership of the underlying product to the contract holder but in practice, it’s rarely used (~2% of the time). Instead, most organizations that are using futures to hedge prices of future production/usage will make separate arrangements with suppliers/customers for physical delivery and just use the futures to protect against contrary price changes. In practice, the final settlement price of the contract can be used to provide the desired price protection regardless of whether the futures contract specifies physical delivery or cash settlement.

While “physical” delivery of Bitcoins as part of a futures contract would certainly be possible, it raises regulatory and security issues in today’s environment where the cybercurrency exchanges are mostly unregulated, somewhat unreliable, and theft due to security hacks is distressingly common. By selecting cash settlement the CME completely avoids the transfer of custody issues and shifts those problems to somebody else—namely the market makers and arbitrageur.

Leverage

One traditional attraction of trading futures is the ability to use relatively small amounts of money to potentially achieve outsized returns. In many futures markets the margin, the amount of money that your broker requires up-front before executing the trade can be quite small compared to the ultimate value of the contract. For example, as of 20-Oct-2021, each E-mini S&P 500 contract was worth $225K ($50*S&P 500 index value)—this “list price” of the contract is called its notional value. The CME only requires you to maintain a minimum margin of $7.65K (3.4% of notional) to control this contract (brokers often require additional margin). Margin requirements this low are only possible because the volatility of the S&P 500 is well understood and your margin account balance is adjusted at the end of every trading day to account for the winnings or losses of the day. If your account balance falls below the margin minimum of $7.65K you’ll need to quickly add money to your account or your position will be summarily closed out by your broker. On the plus side, if you’ve predicted the S&P’s direction correctly your profits will be the same as if you completely owned the underlying stocks in the index. A +1% daily move in the S&P500 would yield $1340 in profit even though you only have $7650 invested— a 29% return—this multiplier effect is called leverage.

Currently, Bitcoin futures have high margin requirements. The CME requires 40% of the notional amount for maintenance margin. Your broker will likely require more than that. The culprit behind these high requirements is Bitcoin’s high volatility—until that calms down the exchanges will protect themselves by requiring a bunch of up-front money. If you don’t come up with the money for a margin call, they want there to still be enough value in your account such that they can close out your position without leaving a negative balance.

Because of the high margin requirements, Bitcoin futures just offer modest leverage compared to just buying Bitcoins outright. However, Bitcoin futures do offer the trader time-tested exchanges that are not nearly as susceptible to hacks, thefts, and unscheduled downtime.

Conclusion

In the movie “Trading Places,” there’s a wild scene where fortunes are made and lost in the orange juice futures pit in a matter of minutes. This scene epitomizes what most of us envision futures trading to look like. The movie depicts a situation where the supply of oranges from the next harvest is unknown—and that is the source of the craziness.

Bitcoins don’t have seasonal variabilities—supply is a known quantity. This supply stability makes Bitcoin futures a lot less dramatic but in the case of Bitcoins this is a real plus—there’s already plenty of drama in the exchanges—the futures market will be the safer space. A different sort of trading places…

Click here to leave a comment